Hyperliquid: The Global Liquidity Index Amid Geopolitical Conflict

Analysis by Karim AbdelMawla and Matt Mena, with additional contributions from Eliezer Ndinga.

When US and Israeli forces struck Iran on Saturday, February 28, traditional markets were dark. With the Chicago Mercantile Exchange (CME) closed, legacy infrastructure could not react. Hyperliquid, a blockchain-based derivatives exchange, remained open. Its 24/7 trading engine allowed the WTI crude perpetual to price the shock in real-time, spiking to $111.53 while traditional markets remained close.

This highlights Hyperliquid’s role as the de facto trading venue and index amid heightened geopolitical conflicts, providing real-time price discovery during weekend gaps. By the time traditional markets reopened and WTI pushed above $110, the gap between Hyperliquid and the CME had already closed. Hyperliquid did not just react faster; it effectively priced the shock nearly 48 hours ahead of the traditional system.

That alone is a compelling narrative. What makes it an investment story is what happened next.

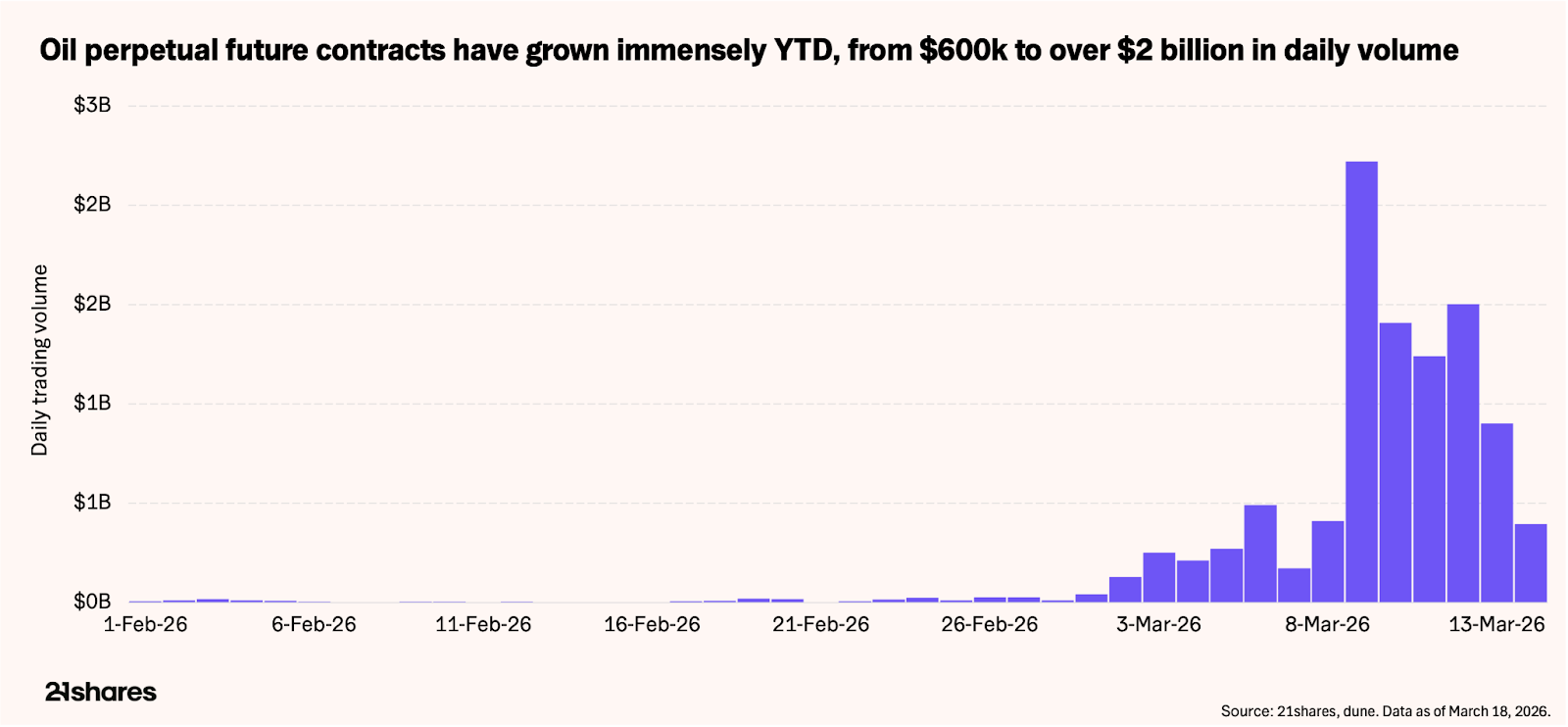

As Iranian attacks on shipping in the Strait of Hormuz increased, Hyperliquid's oil contract recorded $1.99 billion in 24-hour volume, flipping ether to become the platform's second-most traded market after bitcoin. Bitcoin daily volume trades at triple the size of oil on Hyperliquid, making it the preferred commodity for traders – beating oil, silver, and gold.

HYPERLIQUID'S EVOLVING BUSINESS MODEL

In this report, you will discover how to sensibly value Hyperliquid and learn about the key metrics and risks investors should monitor to gauge the platform.

Historically, most of Hyperliquid’s revenue came from digital assets trading, a business model correlated with broader crypto market conditions. However, the recent surging commodity volume is fundamentally expanding the platform’s core business model.

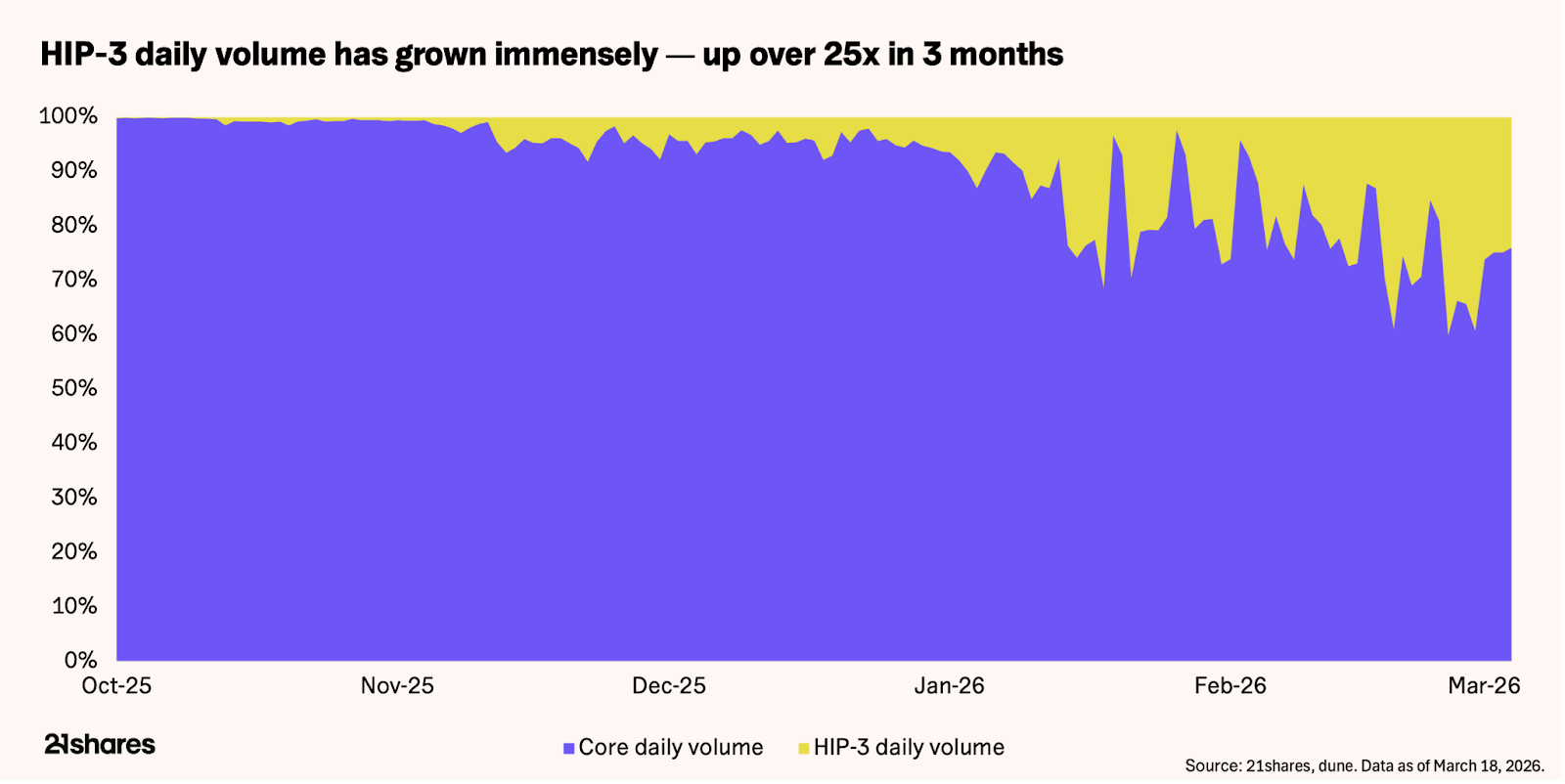

HIP-3, the protocol’s permissionless framework for launching new perpetual futures markets, now accounts for roughly 27% to 30% of total volume, up 500% to 800% from late 2025. Open interest (OI) across these markets reached $1.3 billion in mid-March, more than doubling in a single month. Commodities account for approximately $618 million of that total, with oil alone representing roughly 31%.

The shift is rapid. Crypto pairs, the segment the platform was built for, have seen their volume share drop from roughly 90% to roughly 70%. Currently, six of the top 10 assets by volume are traditional markets like commodities. The platform that once started as a crypto derivatives exchange is now increasingly behaving like a macro exchange.

The bull case for the HYPE token rests on this diversification. With the upcoming HIP-4 launch of prediction markets and options, Hyperliquid is increasingly becoming the “everything exchange.”

FOLLOWING THE MONEY

Hyperliquid’s metrics position the protocol among the most profitable in the digital assets space, comparable to leading traditional derivatives exchanges:

- Cumulative all-time trading volume: $4.12 trillion.

- Cumulative protocol gross revenue: $1.15 billion.

- Annualized gross revenue: $630 million – $700 million.

HYPE’s value accrual is driven by the Assistance Fund, which directs 97% to 99% of fees into automated token buybacks – surpassing $815 million1 to date. This share repurchase program scales with volume and requires no board approval, ensuring every trade on the platform directly benefits the token’s supply dynamics.

At current run rates, the implied buyback yield is roughly 13%2 of the circulating market cap. For comparison, CME Group approved a $3 billion3 share buyback program in late 2024; however, only $532 million has been utilized. Annualized, this is roughly $1.06 billion on a roughly $105 billion market cap, yielding about 1%. Hyperliquid's return on capital is roughly 13 times higher, albeit at greater risk.

HYPE also serves as a medium of exchange for transaction fees and is required as collateral for new HIP-3 deployments. Currently, 500,000 HYPE – worth roughly $19.5 million – must be locked to launch each new perpetual market. As the platform expands into more asset classes, more HYPE is pulled out of circulation from multiple directions at once. At current volumes, the protocol is net deflationary: monthly buybacks of roughly 2.3 million HYPE outpace the approximately 1.75 million tokens entering circulation via unlocks and staking.

PUTTING A NUMBER ON IT

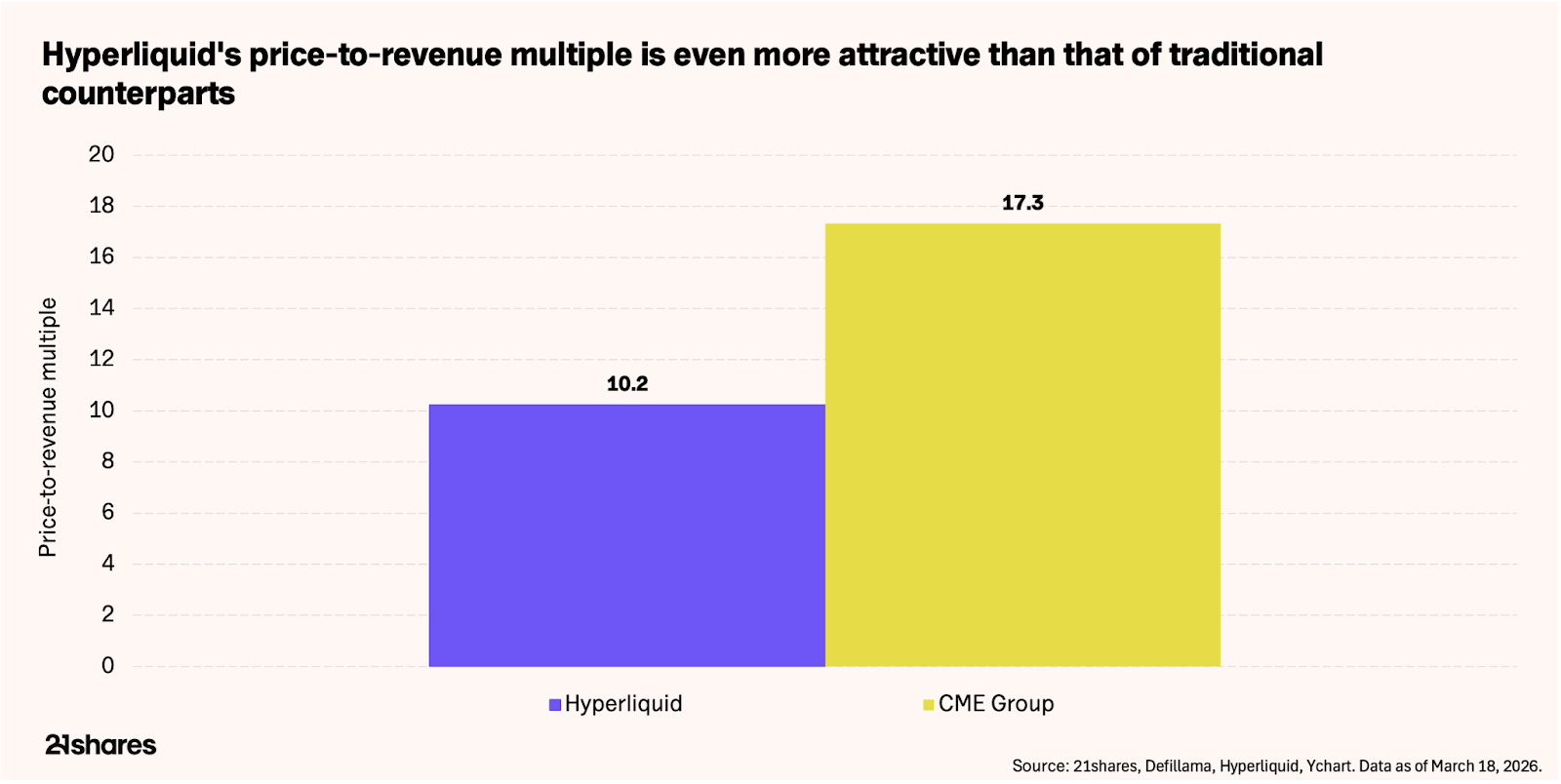

HYPE currently trades at a circulating market cap of approximately $9.8 billion. Against a trailing 12-month revenue of $958.3 million, it carries a price-to-revenue (P/R) multiple of roughly 10.2x. CME – the world’s largest derivatives exchange – trades at about 17.32x4 its $6.55 billion 2025 revenue.

The market is already valuing HYPE in a range similar to that of a traditional exchange. The real question then becomes whether the nature of Hyperliquid’s revenue justifies that comparison. To illustrate the efficiency of blockchain rails compared to traditional systems, Hyperliquid’s 2025 revenue was $873 million6 with only 11 employees – a revenue-per-employee ratio of $79.36 million. In contrast, CME Group’s $6.5 billion in revenue was generated by 3,875 employees7, resulting in a ratio of $1.7 million per employee. This gap underscores the efficiency of blockchain technology and the strength of Hyperliquid’s revenue model.

On a fully diluted basis – accounting for all 1 billion HYPE tokens, many of which have not yet vested – the valuation stretches to about $37 billion, or 38 to 39 times revenue. That figure only makes sense if revenue grows substantially before all tokens enter circulation. However, given Hyperliquid’s year-over year user growth of more than 100%8, along with expansion into other asset classes such as commodities and new markets like prediction markets, this growth premium may be appropriate.

Rather than pinning a specific price target on the token’s valuation, it is more useful to consider the following scenarios:

- Bull case: If geopolitical tensions persist, commodity trading remains elevated, and HIP-3 open interest grows toward $3 billion to $5 billion, annualised revenue could move into the $1.2 billion to $1.5 billion range. At that point, applying a CME-like multiple of roughly 16 to 17 times revenue would imply a market cap of approximately $19 billion to $24 billion, or around $80 to $100 per HYPE.

- Base case: Alternatively, if the situation in Iran cools and commodity activity normalizes, HIP-3 would likely settle closer to 15% to 20% of total volume, leaving the core crypto business to carry the platform. Currently, that business generates about $50 million to $60 million per month9, or roughly $500 million to $600 million annually. At a 13 to 14 times price-to-revenue ratio, this points to a market cap of around $6.5 to $8.5 billion, putting the HYPE token in the $27 to $36 range.

- Bear case: Should Brent normalize near $60, commodity volume would likely retreat. In this scenario, buybacks could fail to offset token unlocks as annualized revenue slides toward the $350 million to $450 million range. Applying a more conservative 10 times multiple, to reflect slower growth and higher dilution, points to a market cap of roughly $3.5 billion to $4.5 billion, or about $15-19 per HYPE. That would imply a 50% to 60% drawdown from current levels. However, this still doesn’t account for the upcoming launches that will diversify the platform’s revenue beyond futures trading, as we have pointed out earlier.

That said, the market confirms our bullish thesis: Bitcoin is down 15% year to date, while HYPE is up more than 50%. This decoupling stems from HYPE’s shift toward diversifying revenue streams. HYPE is not risk-free; it has simply swapped crypto beta for geopolitical volatility. Whether this persists depends on geopolitics and the team’s execution.

THE RISKS WORTH NAMING

HYPE has several primary risks that investors must weigh against the protocol’s growth:

- Centralization and attack vectors: The 2025 JELLYJELLY10 and POPCAT11 token attacks nearly drained the $230 million liquidity vault, forcing manual intervention by validators to delist the asset. While effective, this move highlighted that the platform can act in a centralized manner when its treasury is at risk.

- Regulatory: Hyperliquid remains geoblocked for US users, and onchain commodities occupy a regulatory gray area. To resolve this, HYPE would likely need to acquire a license – similar to Polymarket’s acquisition of a CFTC-regulated entity – to operate legally in the US.

- Geopolitical shifts: Revenue from HIP-3 thrives on global tension. A cooling of macro volatility or a ceasefire could rapidly deflate the “geopolitical volatility (VIX)” premium currently driving the platform’s usage, and consequently, the token’s value.

- Emissions vs. buybacks: While the protocol is currently net deflationary, its ability to absorb ongoing token unlocks is entirely dependent on sustained high trading volumes.

THE BOTTOM LINE

The oil market didn't trade on a blockchain for decentralization purposes; it traded because all other markets were closed. This distinction – utility over ideology – is what separates Hyperliquid's current moment from the decentralized finance narratives that preceded it.

At 13 to 14 times annualized revenue, the market is treating HYPE like a legitimate exchange business rather than a speculative altcoin. The margin of safety depends on whether non-crypto volume persists, whether buybacks continue to outpace dilution, and the success of upcoming features.

The data, at least, earns HYPE a careful look. Whether it earns a position in your portfolio depends on your reading of the world beyond the chart.

______

Footnotes:

- ASXN. (n.d.). ASXN Hyperliquid Dashboard. https://hyperscreener.asxn.xyz/revenue.

- ASXN. (n.d.). ASXN Hyperliquid Dashboard. https://hyperscreener.asxn.xyz/revenue.

- CME Group. (2024, December 5). CME Group Announces $2.1B Annual Variable Dividend and $3B Share Repurchase Program. https://investor.cmegroup.com/news-releases/news-release-details/cme-group-announces-21b-annual-variable-dividend-and-3b-share.

- YCharts. (n.d.). CME Group (CME) Price to Sales Ratio. https://ycharts.com/companies/CME/ps_ratio.

- PR Newswire. (2026, February 4). CME Group Inc. Reports Fourth Consecutive Year of Record Annual Revenue, Adjusted Operating Income, Adjusted Net Income and Adjusted Earnings Per Share for 2025. https://www.prnewswire.com/news-releases/cme-group-inc-reports-fourth-consecutive-year-of-record-annual-revenue-adjusted-operating-income-adjusted-net-income-and-adjusted-earnings-per-share-for-2025-302678360.html.

- DefiLlama. (n.d.). Hyperliquid Protocol Revenue and Fees. https://defillama.com/protocol/hyperliquid?revenue=true&fees=false&tvl=false&groupBy=cumulative.

- CME Group. (2026, February 4). CME Group Inc. Reports Fourth Consecutive Year of Record Annual Revenue, Adjusted Operating Income, Adjusted Net Income and Adjusted Earnings Per Share for 2025. https://www.cmegroup.com/media-room/press-releases/2026/2/04/cme_group_inc_reportsfourthconsecutiveyearofrecordannualrevenuea.html.

- Artemis. (n.d.). Hyperliquid Perp Volume, Open Interest, Fees & Revenue Analytics. https://app.artemisanalytics.com/asset/hyperliquid?from=assets.

- Artemis. (n.d.). Hyperliquid Perp Volume, Open Interest, Fees & Revenue Analytics. https://app.artemisanalytics.com/asset/hyperliquid?from=assets.

- PANews. (2025, March 27). Hyperliquid was attacked and its network was disconnected; Polymarket was attacked by governance and its governance was inactive. https://www.panewslab.com/en/articles/n7qbr7q226xv.

- Halborn. (2025, November 14). Explained: The Hyperliquid Hack (November 2025). https://www.halborn.com/blog/post/explained-the-hyperliquid-hack-november-2025.

This report has been prepared and issued by 21Shares AG for publication globally. All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however, we do not guarantee the accuracy or completeness of this report. Crypto asset trading involves a high degree of risk. The crypto asset market is new to many and unproven and may have the potential not to grow as expected.Currently, there is relatively small use of crypto assets in the retail and commercial marketplace in comparison to relatively large use by speculators, thus contributing to price volatility that could adversely affect an investment in crypto assets. In order to participate in the trading of crypto assets, you should be capable of evaluating the merits and risks of the investment and be able to bear the economic risk of losing your entire investment.Nothing herein does or should be considered as an offer to buy or sell or solicitation to buy or invest in crypto assets or derivatives. This report is provided for information and research purposes only and should not be construed or presented as an offer or solicitation for any investment. The information provided does not constitute a prospectus or any offering and does not contain or constitute an offer to sell or solicit an offer to invest in any jurisdiction. The crypto assets or derivatives and/or any services contained or referred to herein may not be suitable for you and it is recommended that you consult an independent advisor. Nothing herein constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to your individual circumstances or otherwise constitutes a personal recommendation. Neither 21Shares AG nor any of its affiliates accept liability for loss arising from the use of the material presented or discussed herein.Readers are cautioned that any forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors.This report may contain or refer to material that is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject 21Shares AG or any of its affiliates to any registration, affiliation, approval or licensing requirement within such jurisdiction.