Price prediction is arguably finance’s favorite sport – and in crypto, that fascination is amplified by the asset class’s growing mindshare as the industry steps into maturity and declines in volatility. While no one can predict the future with certainty, informed forecasts are grounded in a blend of quantitative analysis and qualitative judgment.

In the first weeks of the year, we’re launching our Price Predictions series, where we take a forward-looking view on the top five crypto assets. Last week we covered Bitcoin and Ethereum. This week we delve into Solana, XRP, and Aave. For Solana we look at five interacting forces that determine valuation in 2026:

- Protocol-level value capture.

- Evolving monetary policy.

- Infrastructure resilience and decentralization credibility.

- Liquidity hub role via dollar payments and settlement.

- Competitive positioning.

As we outline below, Solana enters 2026 as one of the best-performing blockchains with rapidly growing US dollar payments and meaningful institutional experimentation. The debate is no longer whether Solana can scale usage; this has been resolved. The unresolved question is whether economic activity on Solana can be converted into durable value capture for SOL investors.

SOL’s price will ultimately reflect not raw network performance, but the quality, durability, and value capture of that performance.

What’s driving our 2026 outlook?

1. Protocol-level value capture

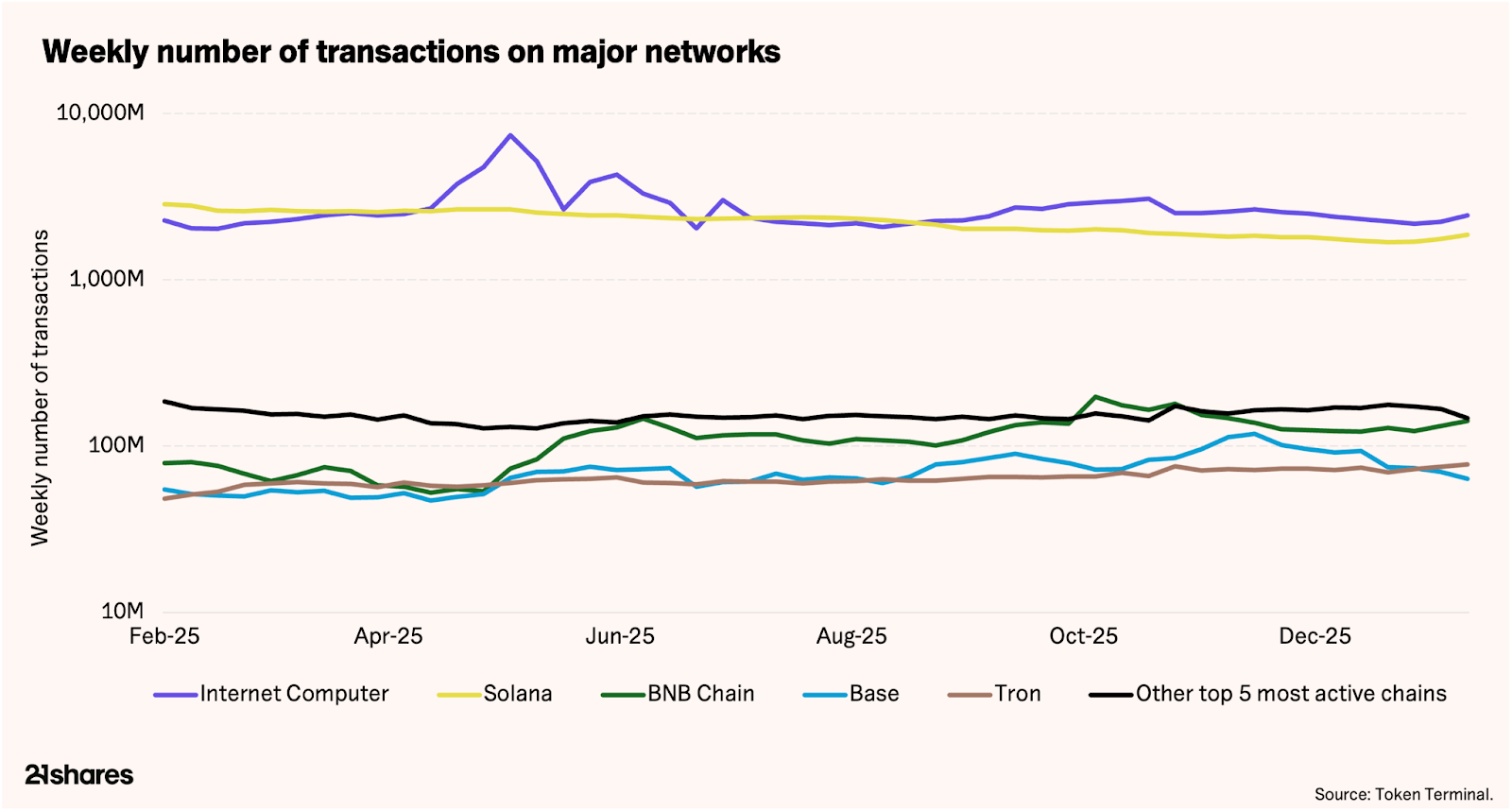

Solana leads all Layer-1 networks in raw on-chain activity. The network processes approximately 2.2 billion transactions per week, second only to Internet Computer (ICP) at 2.6 billion, and far ahead of other major chains such as BNB Chain (~108 million) and Tron (~62 million). User activity follows a similar pattern: Solana averages 16.7 million weekly active addresses, exceeding Near Protocol (15.6 million) and BNB Chain (just under 15 million). Despite this scale, the majority of economic value generated by this activity accrues to applications built on Solana rather than directly to SOL token holders.

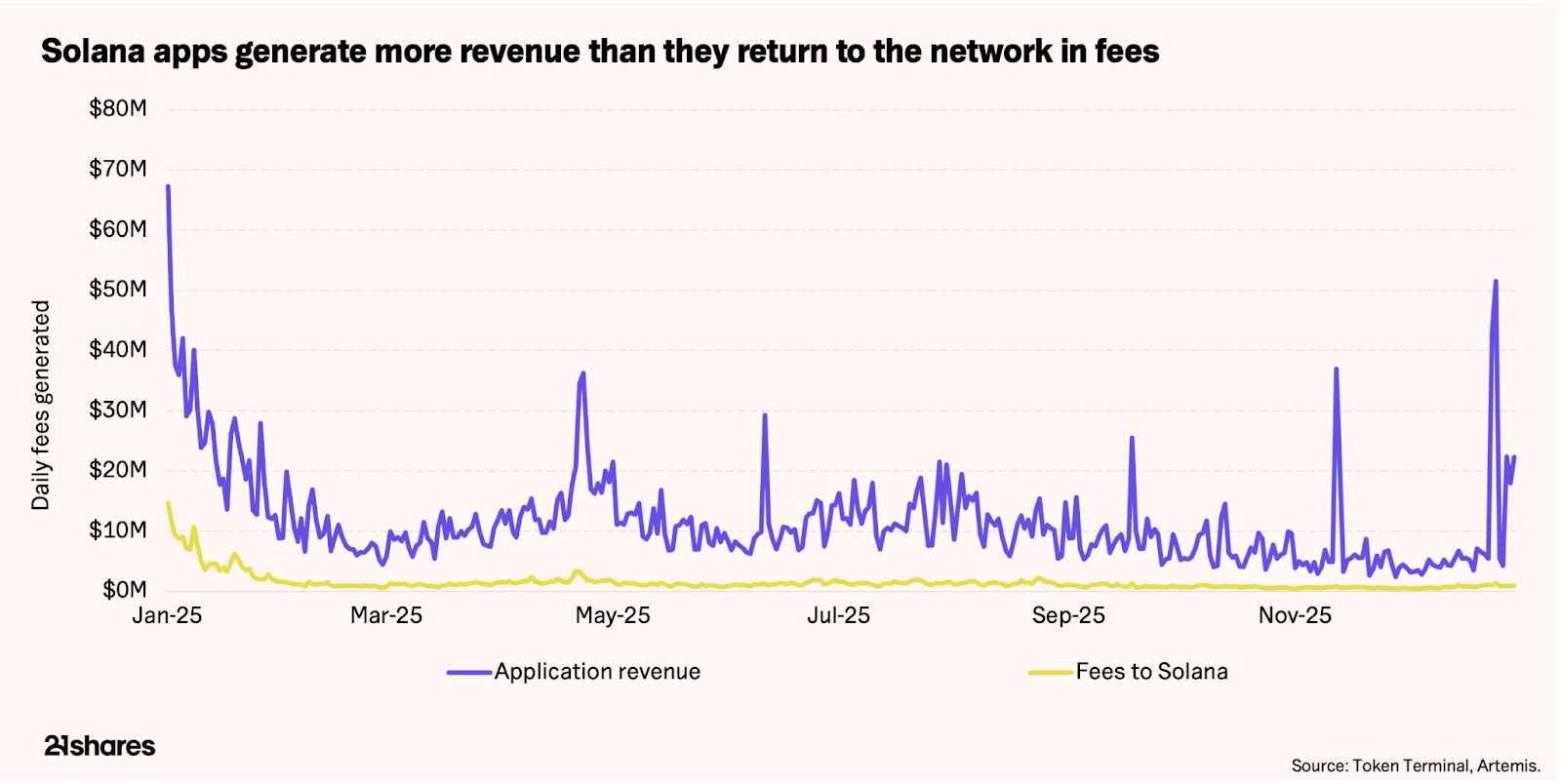

In fact, the last nine months have reinforced a clear monetization imbalance. Application-generated fees now consistently dwarf Solana fees, while protocol-level value capture remains structurally constrained. Of roughly $10 million in daily ecosystem fees, just up to $100,000 flows to the protocol (under 10%), with most economic value accruing to applications.

Solana’s model is high-volume, low-capture. Without a meaningful rise in priority fee capture, usage growth strengthens the network but leaves limited structural upside for SOL.

2. Evolving monetary policy

SOL remains somewhat inflationary, with issuance still around 4% annualized, declining gradually toward its terminal rate. Approximately 70% of the circulating supply is staked, which reduces liquid float but does not eliminate dilution.

Unlike the Ethereum network, Solana no longer has a burn mechanism tied to network usage. This makes SOL’s valuation more sensitive to:

- Sustained staking demand.

- Growth in protocol revenue to offset issuance.

- The persistence of SOL as a monetary asset rather than purely a utility token.

If staking yields compress or demand weakens, inflation becomes a visible valuation headwind. Thus, the proposed change in SIMD-0411, which would reduce inflation to 30% annually, is a genuine valuation catalyst. This proposal is like a plan for a central bank to cut down on printing money much faster than originally promised. If adopted, it will benefit investors with less dilution and benefit from value capture via fees and staking.

3. Infrastructure resilience and decentralization credibility

Solana’s network became significantly more resilient with the official public launch of Firedancer in December 2025, but this progress was built over time. A beta version of Firedancer was already released in late 2024, allowing parts of the new software to be tested live on the network well before full deployment. This early release paved the way for Frankendancer, a hybrid system that combines Firedancer technology with Solana’s existing software and enabled a smoother, lower-risk transition. As a result, Solana is no longer dependent on a single core software system. Today, around 71%1 of Solana runs on Jito, 17% on Frankendancer, and 12% on Agave, reducing single-client risk and improving long-term network reliability.

That said, decentralization remains a mixed picture:

- Active validators have dropped by over 68%, down to 800, from more than 2,500.

- Economic stake concentration remains non-trivial among large operators.

For institutional allocators, reliability and decentralization are not abstract ideals. They directly affect position sizing, risk limits, and cost of capital. Sustained uptime plus demonstrable software diversification are required to reduce the structural risk premium that may still be applied to SOL.

4. Liquidity hub role via US dollar payments and settlement

Solana’s $15 billion in total US dollars is one of its strongest differentiators from most app-platforms. Digital dollars or stablecoins represent the leading indicator to onchain demand, tied to international payments, trading, and treasury activity. However, valuation depends on liquidity quality, as settlement and treasury flows are structurally more valuable than speculative churn.

If stablecoin balances continue to grow but do not translate into higher protocol revenue, Solana risks becoming a high-liquidity, low-capture payment system, limiting fundamental valuation growth. Expanding financial services, including lending and tokenized instruments, would materially strengthen monetization by turning liquidity into recurring, higher-volume activity.

5. Competitive positioning

Over the past six months, Solana’s institutional traction has moved beyond proof of concepts to production-ready tokenization, particularly in public equities and short-dated credit.

- Notably, Galaxy Digital tokenized its publicly listed equity on Solana via Superstate’s Opening Bell, followed by a $50 million tokenized US commercial paper issuance arranged by JPMorgan for Galaxy on Solana and settled in USDC.

- Additional public issuers, including Exodus and Forward Industries, have announced similar equity tokenization plans, indicating an emerging, repeatable issuance pattern rather than isolated experiments.

This positions Solana somewhat differently from Ethereum, though the distinction is not absolute. Ethereum remains the primary environment for tokenized assets integrated with DeFi and trading, where assets are repeatedly reused as collateral across lending, derivatives, and other composable applications. Solana, by contrast, has gained traction in high-throughput use cases such as trading, payments, and settlement, where speed, reliability, and predictable low costs matter more than composability. Much of this activity is driven by institutions and infrastructure providers, supporting recurring usage and reinforcing Solana’s role as practical financial infrastructure - while still requiring sustained volumes, rather than pilots or announcements, to prove durability.

From a valuation standpoint, high-volume payment systems capture thin margins. In 2025, Visa2 processed nearly $16 trillion in payments for about $40 billion in revenue (~0.27% take rate). Solana shows a similar pattern onchain: roughly $1.5 trillion in transaction volume generated an estimated $600 million in protocol fees (~0.04%). As a result, institutional adoption may strengthen Solana’s infrastructure relevance, but without higher fees, sustained staking demand, or broader economic use of SOL, it does not automatically drive token-level value capture.

The 2026 question is therefore not whether institutions are using Solana, but whether this usage becomes economically binding for SOL itself.

Our projected scenario range for 2026

Price predictions are not single-point forecasts, but scenario-based assessments grounded in both quantitative data and qualitative assumptions. By modeling varying adoption, macroeconomic, and market-structure outcomes, we estimate potential valuation ranges at peak levels under each scenario over the course of the year.

- Base case - $150 (21%): Activity and stablecoin balances continue to grow at a moderate pace. Protocol capture improves marginally but remains structurally low. Inflation persists but is absorbed by staking demand. Firedancer improves reliability, but decentralization concerns linger. Institutional usage expands gradually without becoming a dominant driver.

- Bull case - $197 (59%): Revenue via fees rises meaningfully. Stablecoin settlement accelerates with higher-quality flows from corporates and institutions. Multi-client adoption and validator dispersion compress Solana’s risk premium. Institutional settlement and issuance scale beyond pilots, allowing SOL to be positioned as a premium infrastructure for financial services rather than a high-beta asset.

- Bear case - $95 (-23%): Protocol capture fails to improve due to growing competition, staking demand weakens, and inflation becomes more visible. Stablecoin growth stalls or rotates to competing rails. Centralization and governance concerns resurface. Institutional pilots fail to scale, and SOL trades increasingly as a high-activity asset with limited value accrual.

What are the key risks?

- Structural value capture gap: Even with continued activity growth, Solana’s protocol captures a small fraction of ecosystem value. If this does not improve, SOL’s valuation multiple remains capped regardless of usage metrics.

- Inflation without offset: Ongoing issuance without burn makes SOL reliant on staking demand and, to some extent, speculative inflows. A decline in staking participation would expose dilution more directly.

- Decentralization and governance risk: Validator concentration and economic centralization may limit institutional position sizing and prolong the application of a risk discount to SOL.

- Stablecoin liquidity without monetization: A large stablecoin base is supportive, but if settlement volume does not translate into fee growth, Solana risks becoming a low-margin settlement rail. This risk is partly offset if financial services expand, such as lending, payments and trading, and generate incremental fees beyond basic payment and tokenization flows.

- Macro and derivatives sensitivity: SOL remains highly sensitive to risk-off regimes, funding rate swings, and derivatives positioning, amplifying drawdowns during macro stress.

Solana’s 2026 challenge: closing the gap between activity and value accrual

The network has already proven it can scale users, transactions, and liquidity. The next phase requires converting that scale into protocol-level economics while compressing decentralization and reliability risk premia.

If Solana succeeds, SOL can re-rate as a core settlement and execution asset. If not, it risks remaining a technically impressive network with structurally capped upside for the token itself.

Footnotes:

- Blockworks. Solana: Validator clients. Blockworks Analytics. Retrieved from https://blockworks.com/analytics/solana/solana-supply-staking-and-validators/solana-validator-clients.

- Visa Inc. (2025). Visa annual report 2025. Retrieved from https://annualreport.visa.com/home/default.aspx.