Solana 2026: price reset, fundamentals didn’t

Additional contributions by Adrian Fritz and Eliézer Ndinga

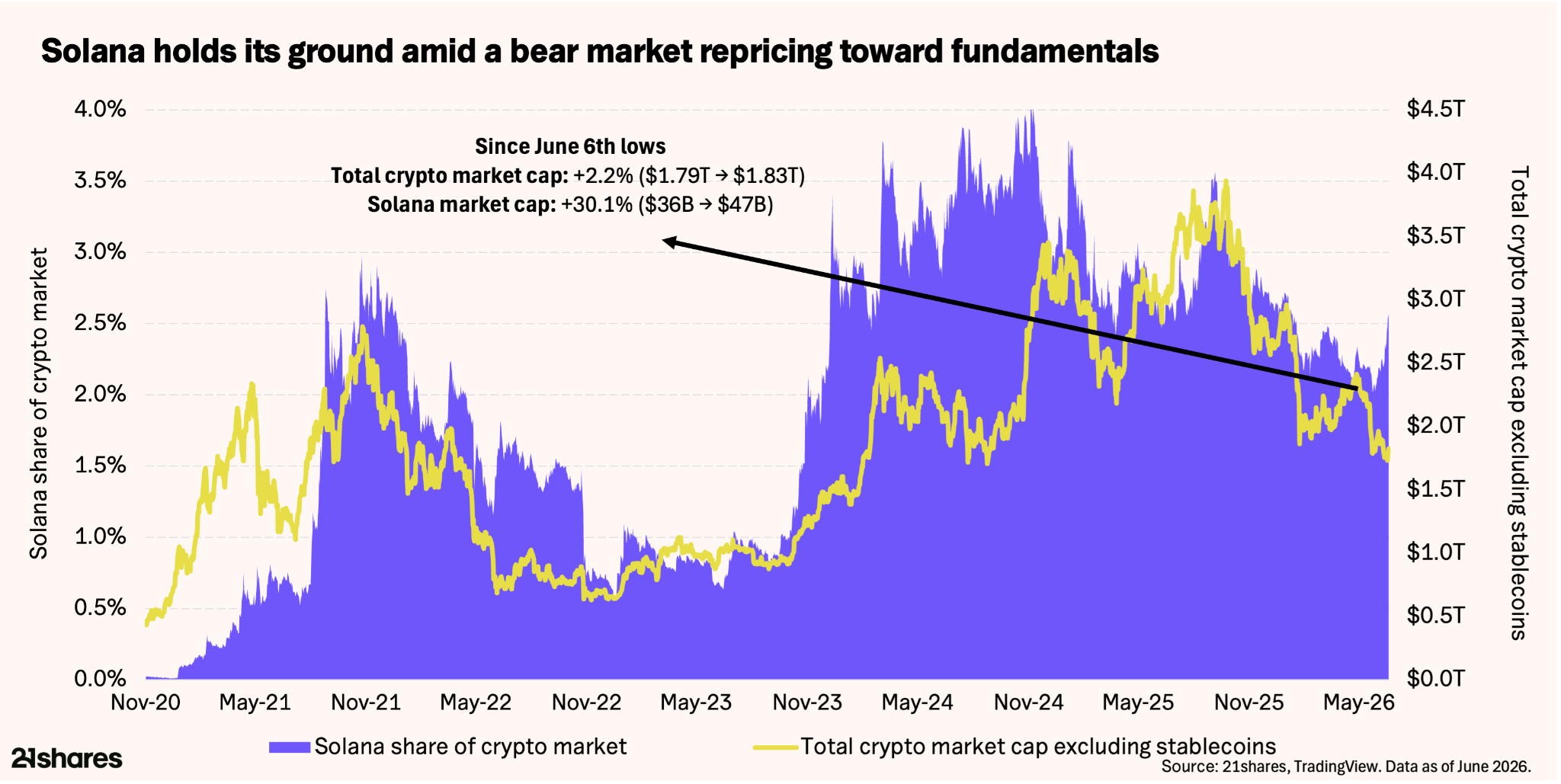

The broader crypto market has shed over $2 trillion in market capitalization since October. Solana's price has fallen roughly two-thirds from its peak. But while the price has reset, the network has not.

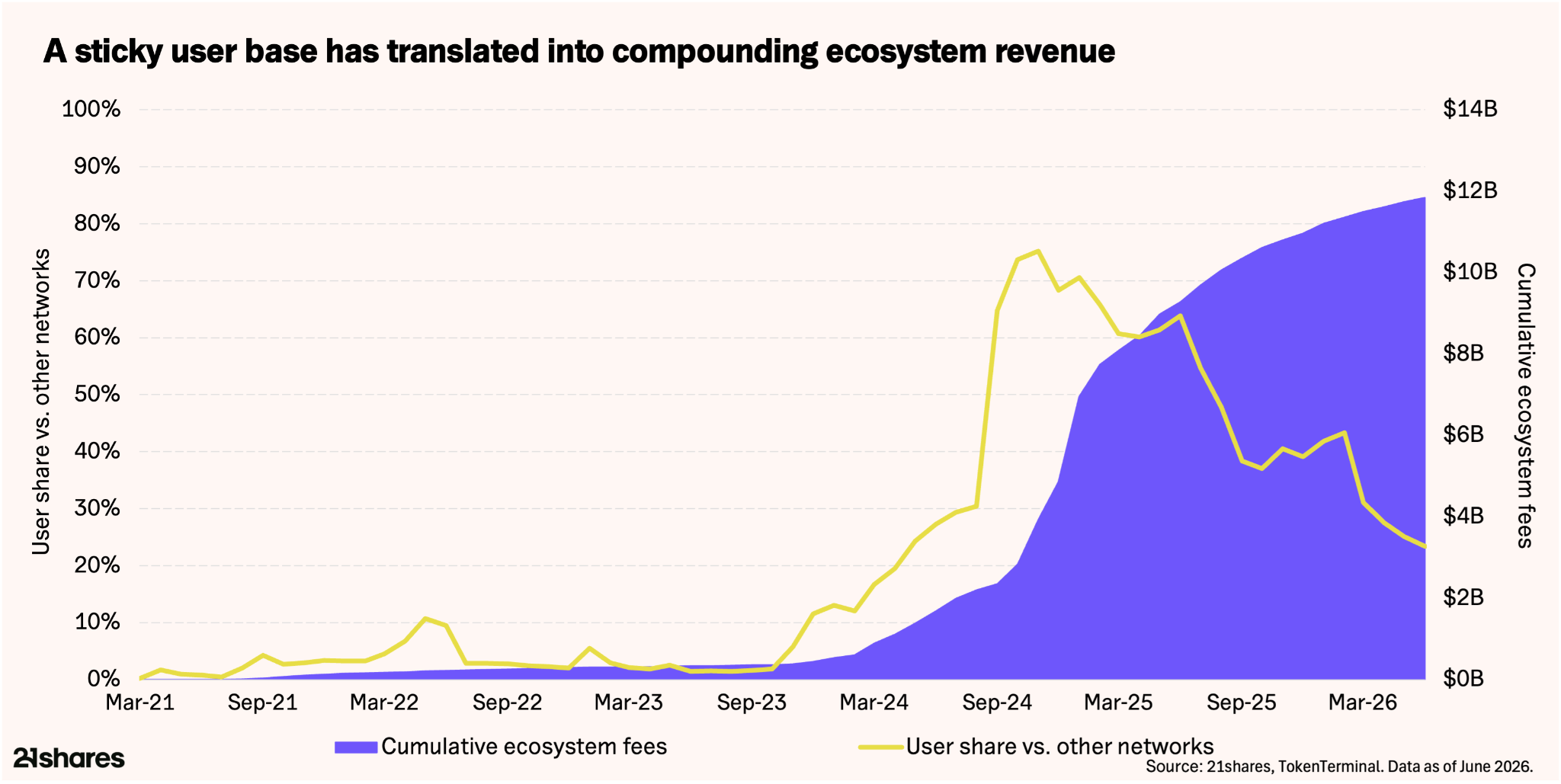

The memecoin boom that peaked in January 2025 drove app-layer fees to $2 billion in a single month and the network's user share to unsustainable heights - then both collapsed. What the washout revealed matters more than the washout itself: the economy that remained is roughly an order of magnitude larger than the pre-boom baseline. Applications on Solana earned approximately $148 million per month in the first half of 2026 - an annualized pace of $1.8 billion.

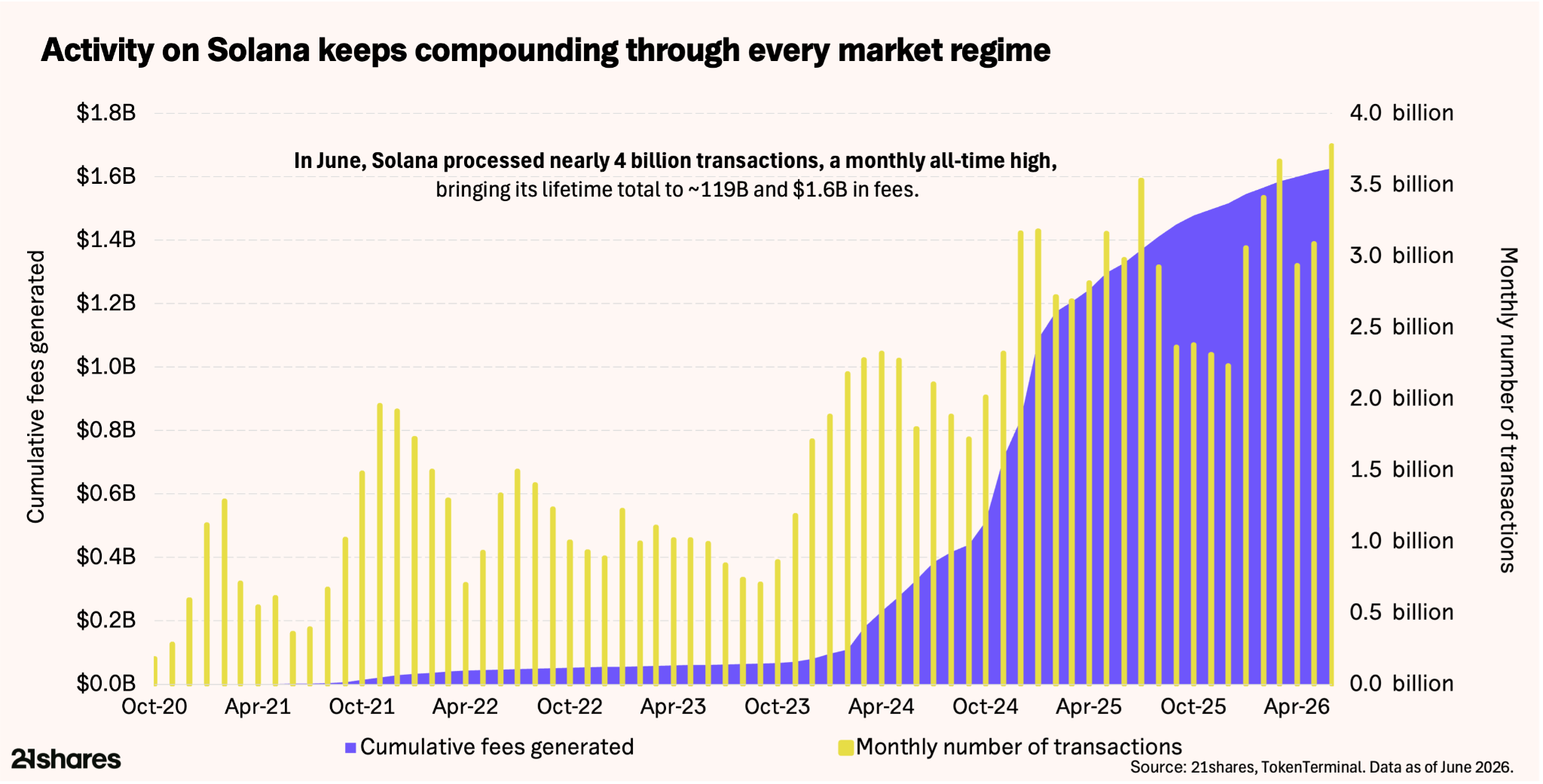

June was the busiest month in Solana's history: nearly 4 billion transactions processed, stablecoin supply at record levels, and tokenized real-world assets up roughly 230% year-on-year. Price is tracking sentiment. The network is tracking adoption. The two have decoupled - and the gap between them is the question worth examining.

4 reasons that make the case for Solana’s entry point

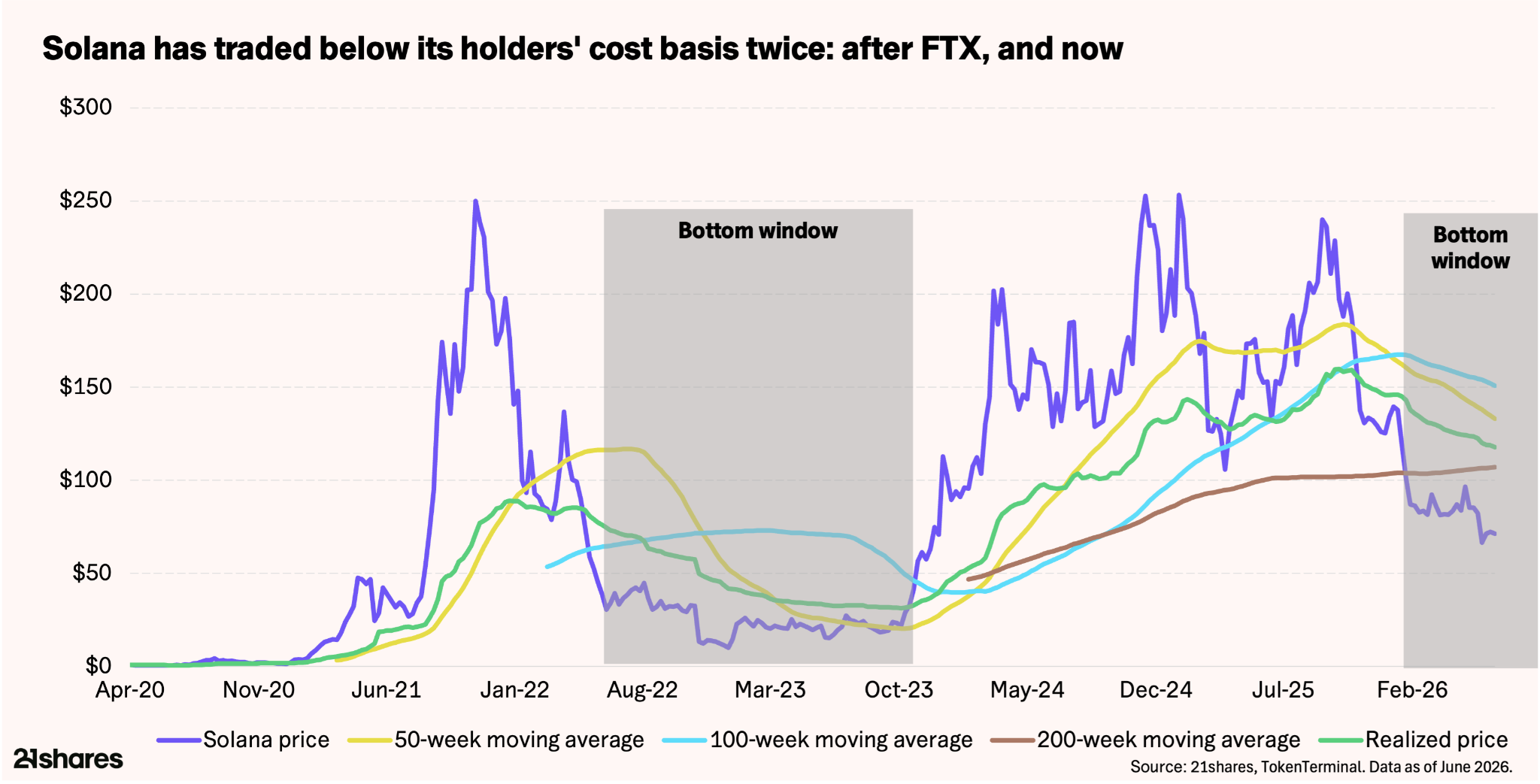

Solana trades near $80 in July 2026, down roughly two-thirds from its peak. This drawdown is structurally different from the last one. In 2022-23, the collapse of the FTX exchange drove the network's price 96% below its peak and hollowed out usage alongside it. This time there is no failure, no insolvency, and no contagion - and where the previous bear market emptied the network, this one has coincided with record activity.

1. The Solana network just posted its busiest month in history

Usage and price have never been this far apart. In June, with the price at its lowest point in the cycle, Solana processed nearly 4 billion transactions - a monthly all-time high, bringing its lifetime total to roughly 119 billion and over $1.6 billion in cumulative fees. In 2025 alone, the network settled roughly $3 trillion in stablecoin volume, placing it alongside major payment platforms at a fraction of their age. Solana also commands almost 50% of global onchain spot decentralized exchange volume, roughly $425 billion per month. The demand is organic: users settling payments and moving stablecoins through a bear market because they need the blockspace.

2. Solana’s economy survived its stress test and rebased higher

The memecoin washout was a test of whether Solana's users and revenue were real; a 90%+ fee reset would have hollowed out a speculative network. Instead, roughly one in four active users across every major chain and L2 remains on Solana, about seven times its share before the boom, and applications built on the network have generated nearly $12 billion in total. A user base and revenue floor that survive a washout of that magnitude are proof of a serious moat.

3. Institutions are building big on Solana’s rails

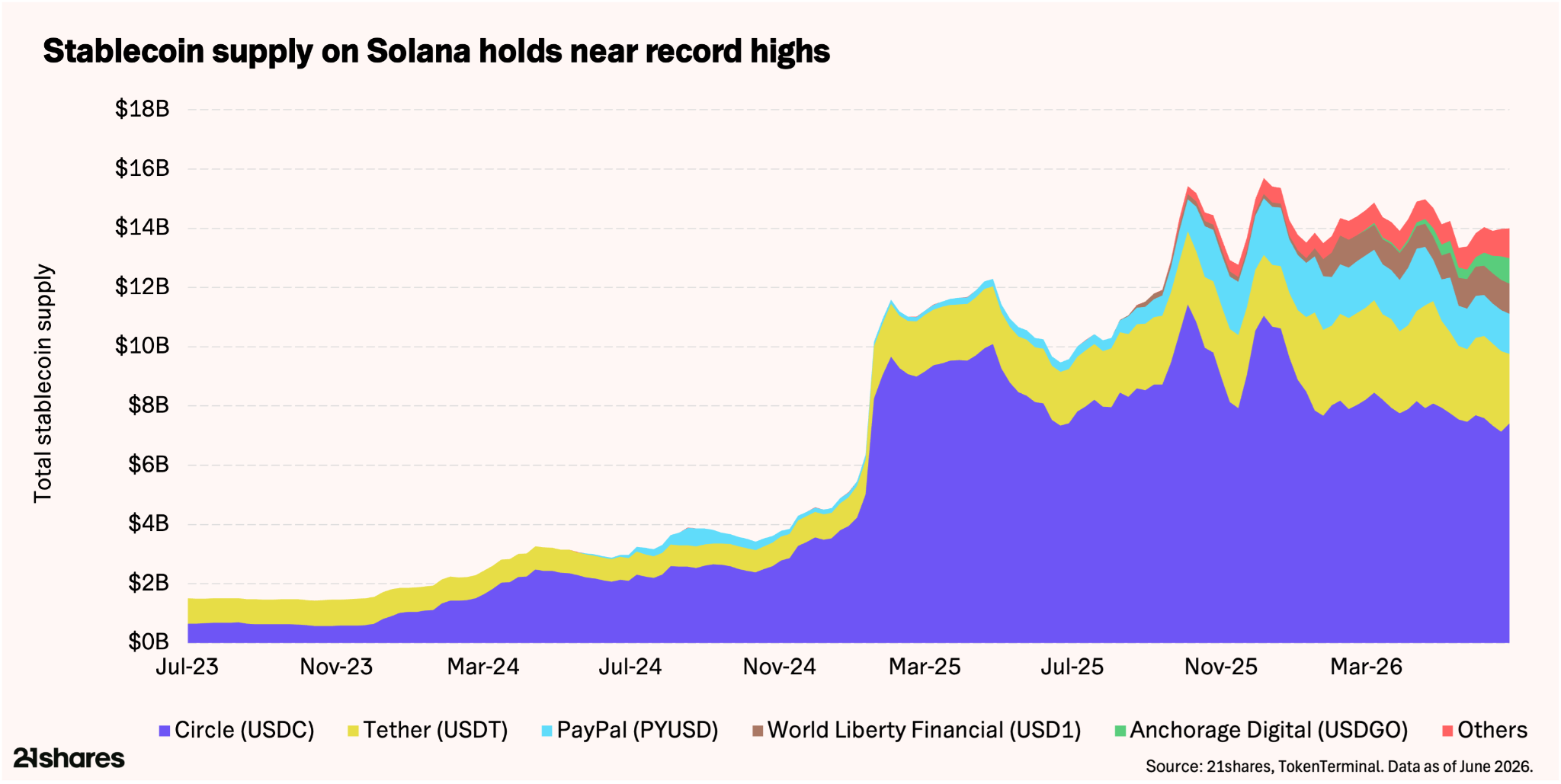

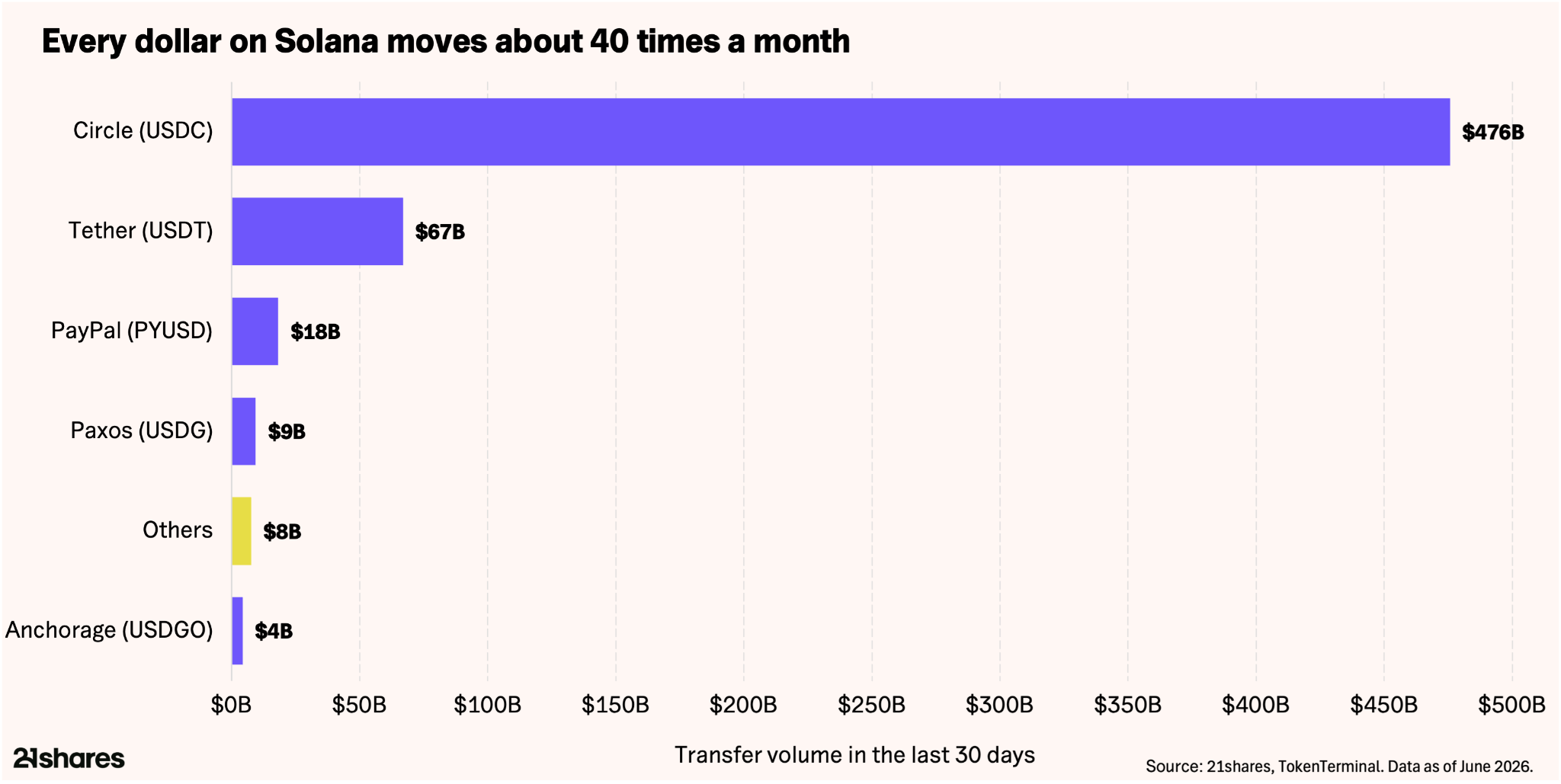

Stablecoin supply on Solana sits at record levels, roughly $16 billion at its peak, and the issuer bench has widened from two names to a deep roster: Circle, Tether, PayPal's PYUSD via Paxos, the Global Dollar consortium backed by Robinhood, Kraken and Galaxy, World Liberty Financial, Anchorage Digital, and SoFi.

The capital moves, too: over half a trillion dollars in stablecoin transfer volume in the last 30 days alone, meaning every dollar on Solana turns over roughly 40 times a month.

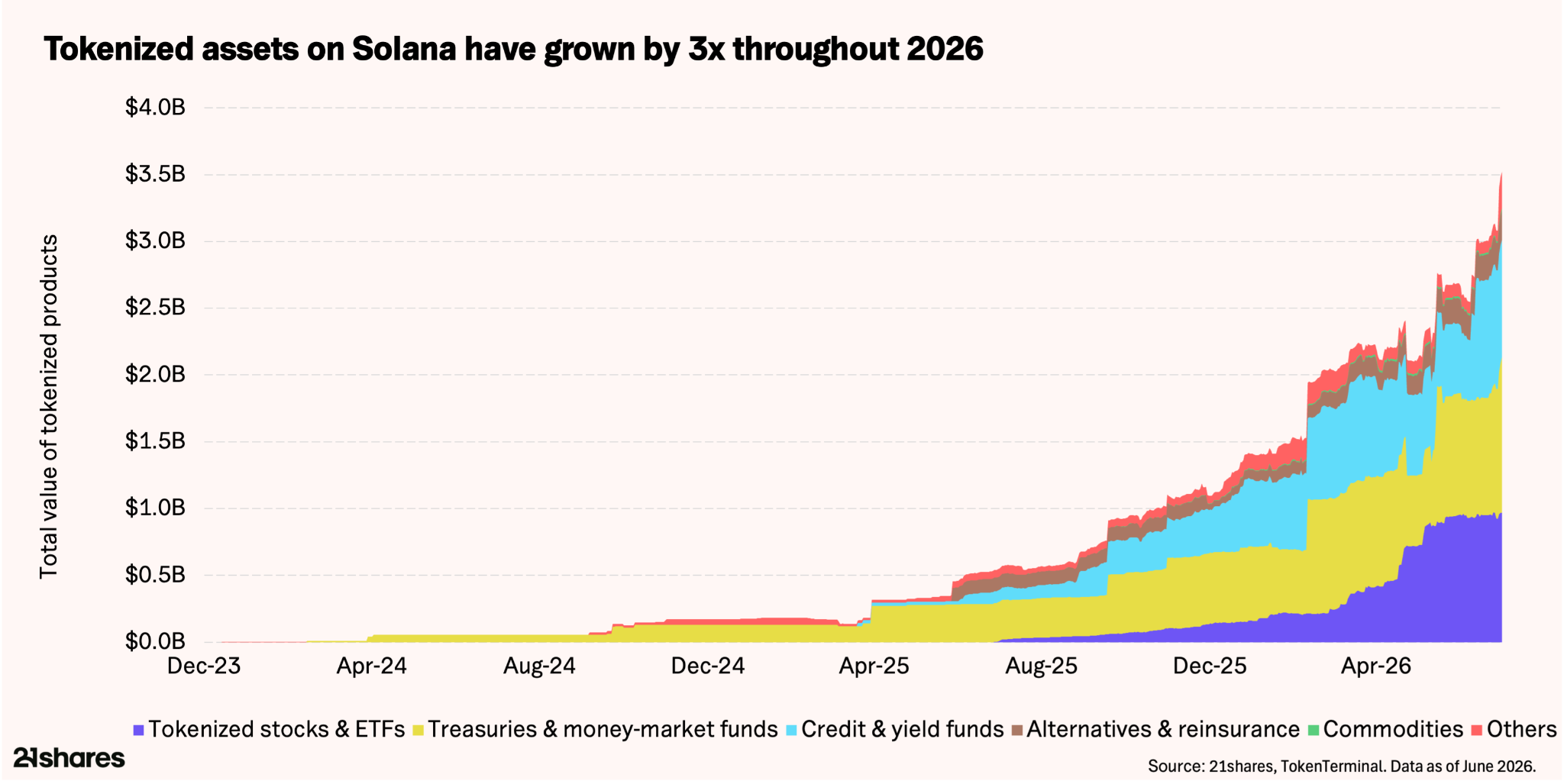

Tokenization is scaling too: real-world assets on the network have climbed to $3.4 billion, up roughly 230% year-on-year, spanning treasuries, private credit, tokenized equities, and gold, not memecoins. Solana just recorded its largest week ever for tokenized equities at $1.36 billion in volume, capturing roughly 97% of all onchain equity trading, and pre-IPO SpaceX exposure drove a record $1.49 billion single-day RWA transfer.

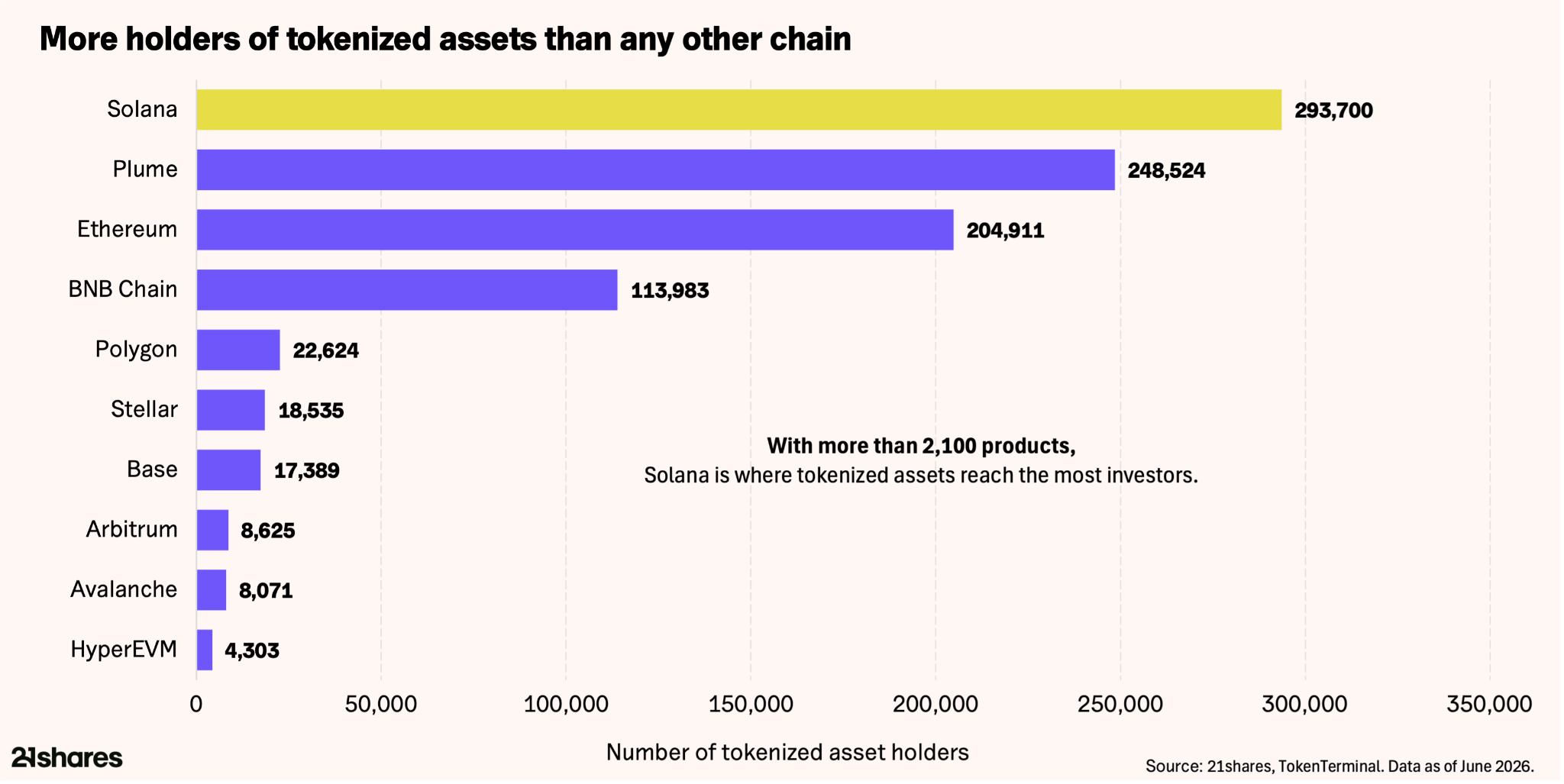

More than 290,000 investors hold tokenized assets on Solana, more than on any other chain. Strategic integrations now span Visa, Citi, Amundi-managed Spiko, MoneyGram, Western Union, Stripe, PayPal, and State Street.

4. Solana’s price has overshot every long-term anchor

Solana trades roughly 30 to 40% below each of its long-term anchors: its realized price and its 50-, 100-, and 200-week moving averages. Overshoots this deep reflect forced and fearful selling, not fair value, and they have historically resolved upward once sellers exhaust. The one precedent, the 2022-23 discount zone, marked the bottom before a roughly 20x recovery. Below the average holder's cost basis is where sellers run out, patient capital enters, and floors are built.

Bottom line:

Solana's network is compounding while price has reset

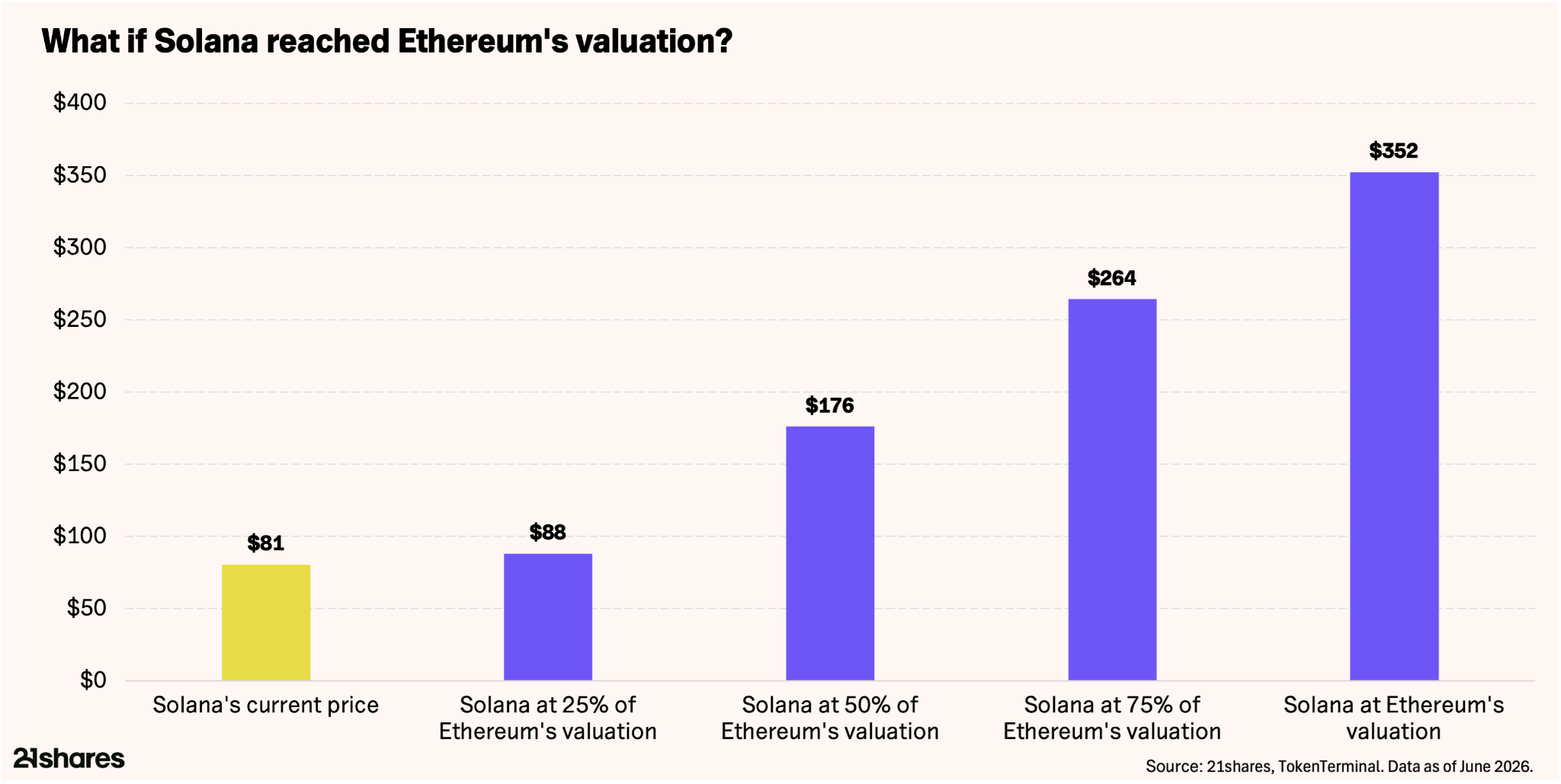

Solana already trades at roughly 23% of Ethereum's valuation, while on the adoption metrics that matter - activity, users, tokenized products, and holders - it reads as a peer. The fundamentals stopped being the gap; only the price is. That framing turns the much-debated "flippening" into simple arithmetic. Solana reaching half of Ethereum's valuation is roughly 2.2x from today's price; parity is roughly 4.3x.

Usage is decoupling upward from price - historically one of the strongest signals in crypto. Some investors view this gap as offering asymmetric upside; this view is contested, and digital assets remain highly volatile. Further volatility cannot be ruled out: a failure of the June lows near $62 would open a retest of the $50-$60 zone. The selling, however, has been market-wide and mechanical, not a verdict on the network.

The Alpenglow upgrade, targeting 100- to 150-millisecond finality and potentially landing in Q3, would move Solana into direct competitive range for onchain perpetual futures - the highest-fee vertical in crypto.

For investors considering exposure, the most defensible path through this zone is a gradual, sized approach rather than attempting to time the exact low. Past performance is not a reliable indicator of future results.

This report has been prepared and issued by 21Shares AG for publication globally. All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however we do not guarantee the accuracy or completeness of this report. Crypto asset trading involves a high degree of risk. The crypto asset market is new to many and unproven and may have the potential to not grow as expected.

Currently, there is relatively small use of crypto assets in the retail and commercial marketplace in comparison to relatively large use by speculators, thus contributing to price volatility that could adversely affect an investment in crypto assets. In order to participate in the trading of crypto assets, you should be capable of evaluating the merits and risks of the investment and be able to bear the economic risk of losing your entire investment.

Nothing in this email does or should be considered as an offer by 21Shares AG and/or its affiliates to sell or solicitation by 21Shares AG or its parent of any offer to buy bitcoin or other crypto assets or derivatives. This report is provided for information and research purposes only and should not be construed or presented as an offer or solicitation for any investment. The information provided does not constitute a prospectus or any offering and does not contain or constitute an offer to sell or solicit an offer to invest in any jurisdiction.

Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties, and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax, or other advice and users are cautioned against basing investment decisions or other decisions solely on the content hereof.