Why Canton solves DeFi’s institutional privacy gap

Privacy and consumer protection are issues which frequently arise for financial institutions considering blockchain technology. We believe the Canton Network, which was purpose-built to overcome the key barriers preventing traditional finance from moving on-chain, solves this privacy gap and provides a regulatory-compliant environment. This article explains the difference between permissionless and permissioned blockchains, as well as public versus private data.

Who can participate in blockchains and view their data

There is no universal privacy setting for blockchains. And blockchain privacy is not a switch that can be turned on and off. It is better visualised as a gradient dependent on two key components: who is allowed to join a specific blockchain and who is allowed to view the transaction data.

- Blockchain participation can be either open to everyone (permissionless) or restricted (permissioned). Ethereum and Solana, like the Internet, are examples of permissionless networks: they maximize openness and liquidity but expose all transaction data. In contrast, permissioned networks function more like an "intranet": participation is restricted to authorised institutions and individuals. While many institutions already operate on permissionless chains, a permissioned model offers built-in access controls and the ability to keep sensitive data private, making it easier for them to meet regulatory standards.

- Data visibility is also crucial to blockchain privacy. Public chains make all data visible, while private chains limit visibility to network participants. As financial institutions move increasingly on-chain, most require a balance between these two extremes, seeking selective privacy, auditability, and the ability to coordinate with partners without revealing sensitive information.

Meeting institutional demands around on-chain privacy

For over a decade, blockchains sat primarily on the sidelines of traditional finance due to concerns around privacy and regulatory compliance. This is because traditional firms cannot simply migrate assets or client data onto fully transparent public blockchains, and earlier iterations of privacy-focused blockchains were underwhelming in their ability to interact with the broader ecosystem.

However, financial institutions can no longer afford to ignore the tangible gains made by blockchain technology in settlement speed, cost efficiency, and asset mobility. The past year in particular has seen a subtle but important industry shift, with an increasing number of major banks, asset managers, and infrastructure providers actively moving on-chain.

Privacy is a key factor of consideration in this institutional shift, with advancements in blockchain privacy creating new on-chain environments that meet the needs of regulated financial institutions. For many years, traditional financial institutions could not find the privacy sweet spot they needed, but new blockchains like the Canton Network are changing this.

How Canton can bridge the privacy gap

The Canton Network was purpose-built by former Goldman Sachs and DRW engineers to overcome key barriers preventing traditional finance from moving on-chain. It is effectively a privacy-preserving layer which no longer forces institutions to choose between transparency and isolation.

It does this by operating as a network of networks. Importantly for traditional financial institutions, each Canton participant runs its own network with customizable governance, access controls, and privacy. Think of a bank accessing customer information in a protected network against external cyber threats, with data only visible to the bank’s IT department. Though insular, and therefore private, each intranet remains interoperable through Canton’s Global Synchronizer, allowing the exchange of value and data across partners without exposing confidential information.

Having only recently launched, Canton already sees over $100 billion in daily repo flows1 – a clear indicator of the institutional thirst for such a solution. Among the big name firms supporting the Canton Network are Goldman Sachs, BNP Paribas, Microsoft, Deutsche Bank, Circle, and Polychain2,3,4, with many of these institutions serving as investors as well as network validators and governance participants.

Canton Coins are designed to boost network security

The Canton Network is built so that its native token, Canton Coin (CC), underpins both economic activity and network security. Instead of paying traditional subscription fees in dollars, as they would for enterprise services like Slack, institutions “subscribe” to Canton by paying usage fees in CC. In return, they gain permissioned access to Canton's infrastructure and settlement rails.

Network operators, primarily regulated financial institutions, run the Global Synchronizer and application domains. They order and validate transactions, enforce data-permission rules, and ensure uptime. Rather than using an open proof-of-stake system, Canton uses a permissioned, utility-based incentive model: operators earn newly minted CC for delivering reliability and capacity, similar to how credit card reward programs incentivize usage rather than speculation. Misconduct or downtime results in loss of rewards and removal from the validator set, creating strong alignment between performance, compliance, and economic incentives.

This directly links institutional activity to token value. When usage increases, operators earn higher CC rewards, while a portion of every CC fee is permanently burned. Over $110 million in CC has already been burned, reducing supply as network traffic grows. The result is a token model where CC both secures the network and aligns incentives among validators, users, and the broader ecosystem.

The case for Canton

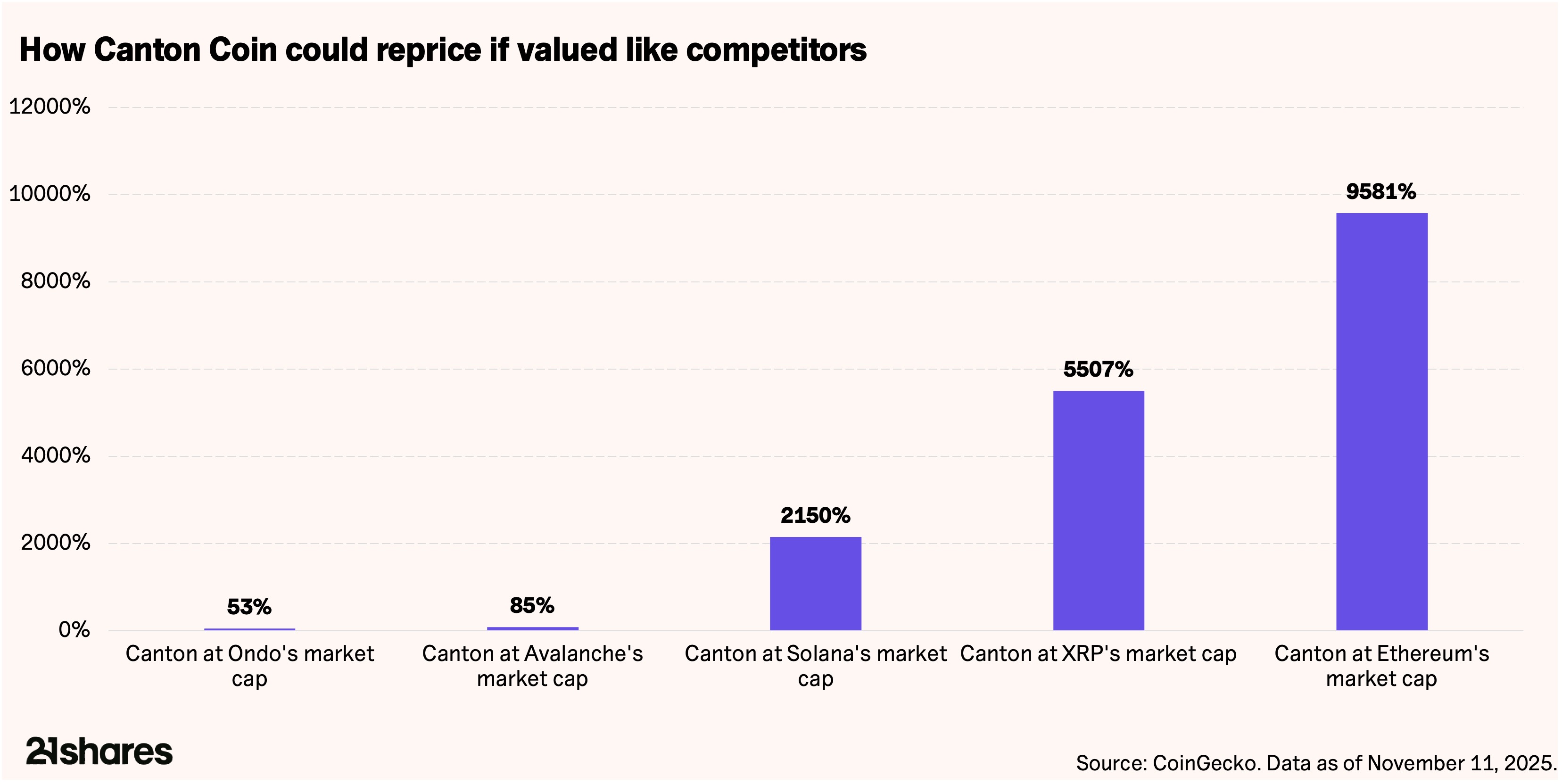

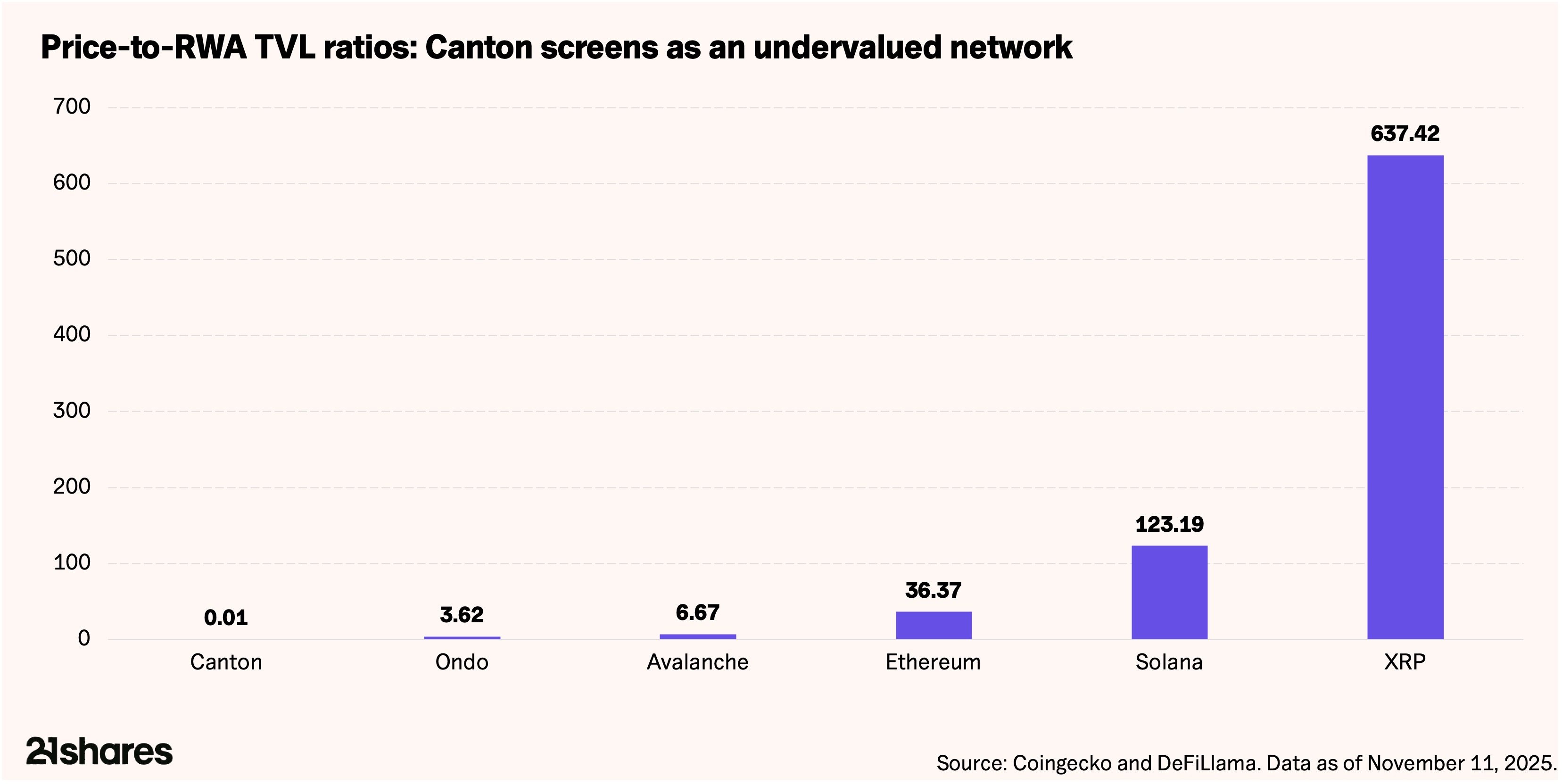

Canton is targeting one of the largest long-term opportunities in crypto: the tokenization of traditional financial assets. Analysts estimate that $10–$30 trillion in assets may be brought on-chain over the next decade. Canton already processes more than $4 trillion in annual tokenized volume, putting it ahead of nearly all public blockchains by real economic activity, yet its token trades at a fraction of their valuation.

One way to illustrate this is through a valuation multiple similar to those used in traditional finance. In equities, investors often compare a company’s valuation to its revenue or assets under management. In crypto, the closest equivalent is comparing a network’s market value to the value of assets issued or settled on it, known as Total Value Locked (TVL).

Based on this measure, Canton currently trades at a price-to-TVL ratio of roughly 0.01x, meaning investors pay only one cent for every dollar of real-world assets the network supports. In comparison, networks such as Ethereum and XRP trade at significantly higher multiples. Put simply, investors are paying far more for each dollar of activity on those chains than on Canton.

This valuation gap exists despite strong institutional momentum. The institutions adopting Canton are doing so because it solves the biggest barriers they face when using public blockchains: privacy, regulatory compliance, and deterministic settlement. As tokenization accelerates and more financial institutions move core workflows on-chain, networks that meet these requirements are positioned to capture the majority of market share.

Footnotes:

- Canton Network. “How Canton Network Delivers Institutional-Grade Privacy.” Canton Network Blog, https://www.canton.network/blog/how-canton-network-delivers-institutional-grade-privacy

- Canton Network. “Goldman Sachs, Microsoft and Deutsche Bank Are Testing Canton Network.” https://www.canton.network/news/goldman-sachs-microsoft-and-deutsche-bank-are-testing-canton-network

- Canton Network. “How Canton Network Delivers Institutional-Grade Privacy.” Canton Network Blog, https://www.canton.network/blog/how-canton-network-delivers-institutional-grade-privacy

- CryptoRank. “Digital Asset ICO Overview.” CryptoRank.io, https://cryptorank.io/ico/digital-asseton

This report has been prepared and issued by 21Shares AG for publication globally. All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however, we do not guarantee the accuracy or completeness of this report. Crypto asset trading involves a high degree of risk. The crypto asset market is new to many and unproven and may have the potential not to grow as expected.Currently, there is relatively small use of crypto assets in the retail and commercial marketplace in comparison to relatively large use by speculators, thus contributing to price volatility that could adversely affect an investment in crypto assets. In order to participate in the trading of crypto assets, you should be capable of evaluating the merits and risks of the investment and be able to bear the economic risk of losing your entire investment.Nothing herein does or should be considered as an offer to buy or sell or solicitation to buy or invest in crypto assets or derivatives. This report is provided for information and research purposes only and should not be construed or presented as an offer or solicitation for any investment. The information provided does not constitute a prospectus or any offering and does not contain or constitute an offer to sell or solicit an offer to invest in any jurisdiction. The crypto assets or derivatives and/or any services contained or referred to herein may not be suitable for you and it is recommended that you consult an independent advisor. Nothing herein constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to your individual circumstances or otherwise constitutes a personal recommendation. Neither 21Shares AG nor any of its affiliates accept liability for loss arising from the use of the material presented or discussed herein.Readers are cautioned that any forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors.This report may contain or refer to material that is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject 21Shares AG or any of its affiliates to any registration, affiliation, approval or licensing requirement within such jurisdiction.