The two eras of Bitcoin valuation: pre- and post- ETFs

Key takeaways:

- While useful, onchain metrics alone are insufficient for Bitcoin valuation, as a large portion of trading and ownership changes now occur offchain.

- ETFs (holding 7% of supply), futures markets, and macro conditions now significantly drive Bitcoin's price discovery as derivatives activity expands sharply.

- Valuing Bitcoin now demands a combined approach: analyzing onchain indicators alongside offchain indicators such as ETF flows, futures positioning, and macro liquidity signals.

For the first decade of Bitcoin’s existence, onchain metrics provided a reliable view of investor behaviour and market cycles, as almost all trading and transfers occurred directly on the blockchain. This valuation era came to an end in early 2024, when the introduction of US spot Bitcoin exchange traded funds (ETFs) reshaped the market. Suddenly offchain market data became a crucial factor, as investors gained an alternative entry point into the Bitcoin market. Though ETFs triggered the need for a new era of Bitcoin valuation, futures markets and macro conditions also play a part. This shift raises an important question: Can onchain indicators still provide a clear picture of market conditions, or must they now be combined with offchain data to understand valuation?

How Bitcoin valuation worked before ETFs

Before ETFs existed, almost all economic activity was visible on Bitcoin’s blockchain. With nearly all of the market’s activity available in one place, the following were key indicators of Blockchain’s value:

- Market Value to Realized Value Ratio, which functions similarly to a Price-to-Book Ratio in traditional markets and is commonly known as MVRV. MVRV showed when the market traded far above or below its aggregate cost basis.

- Measures of unrealised profit and loss across the network, called Net Unrealized Profit or Loss or NUPL, also played an important role. NUPL captured periods of widespread optimism or stress.

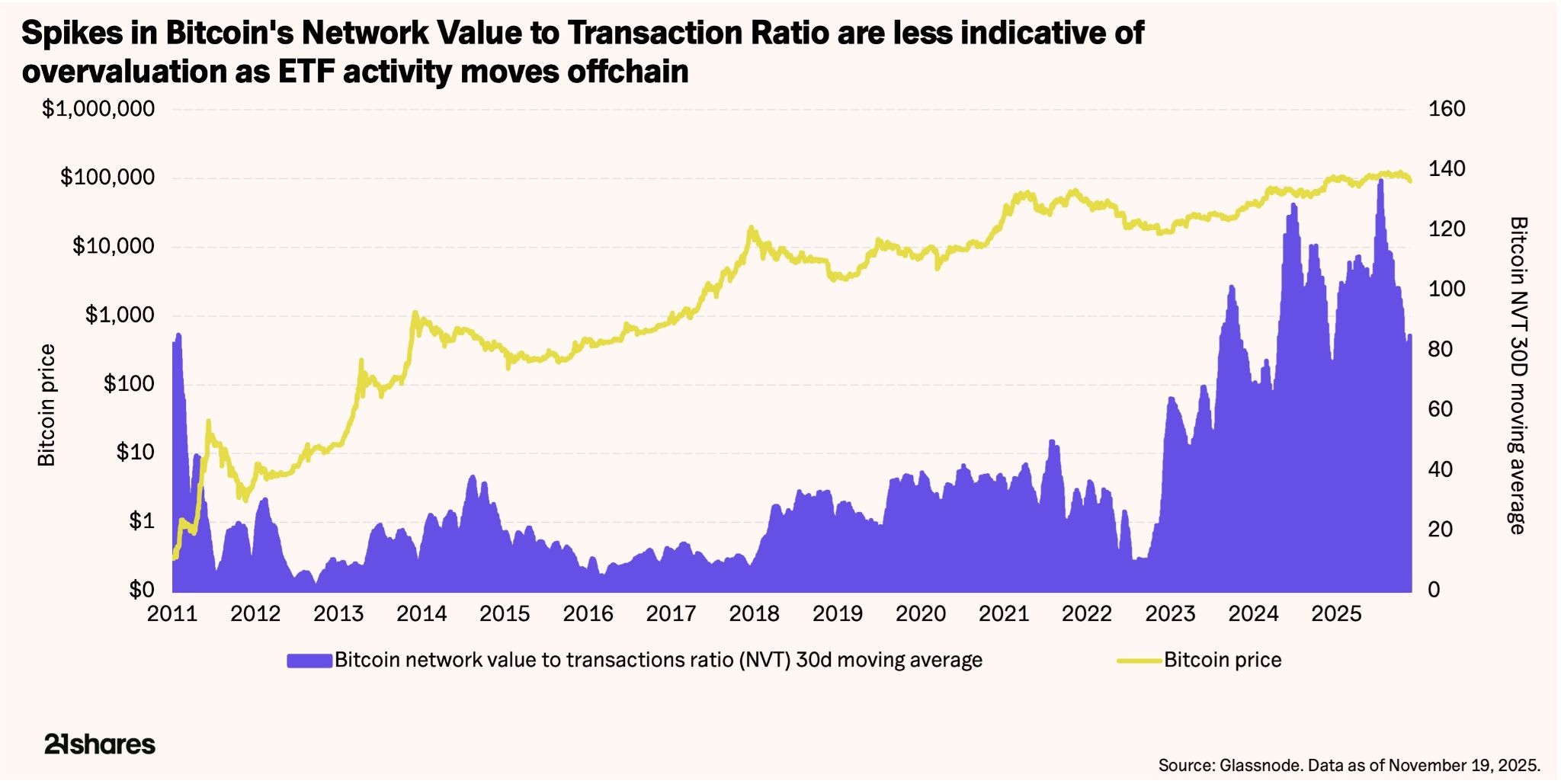

- The Network Value to Transactions Ratio, often shortened to NVT, acted like a Price-to-Earnings Ratio by comparing the value of the network with the value of transactions moving across it. NVT spikes aligned well with cycle peaks and troughs by comparing the value of the network with the value being transferred.

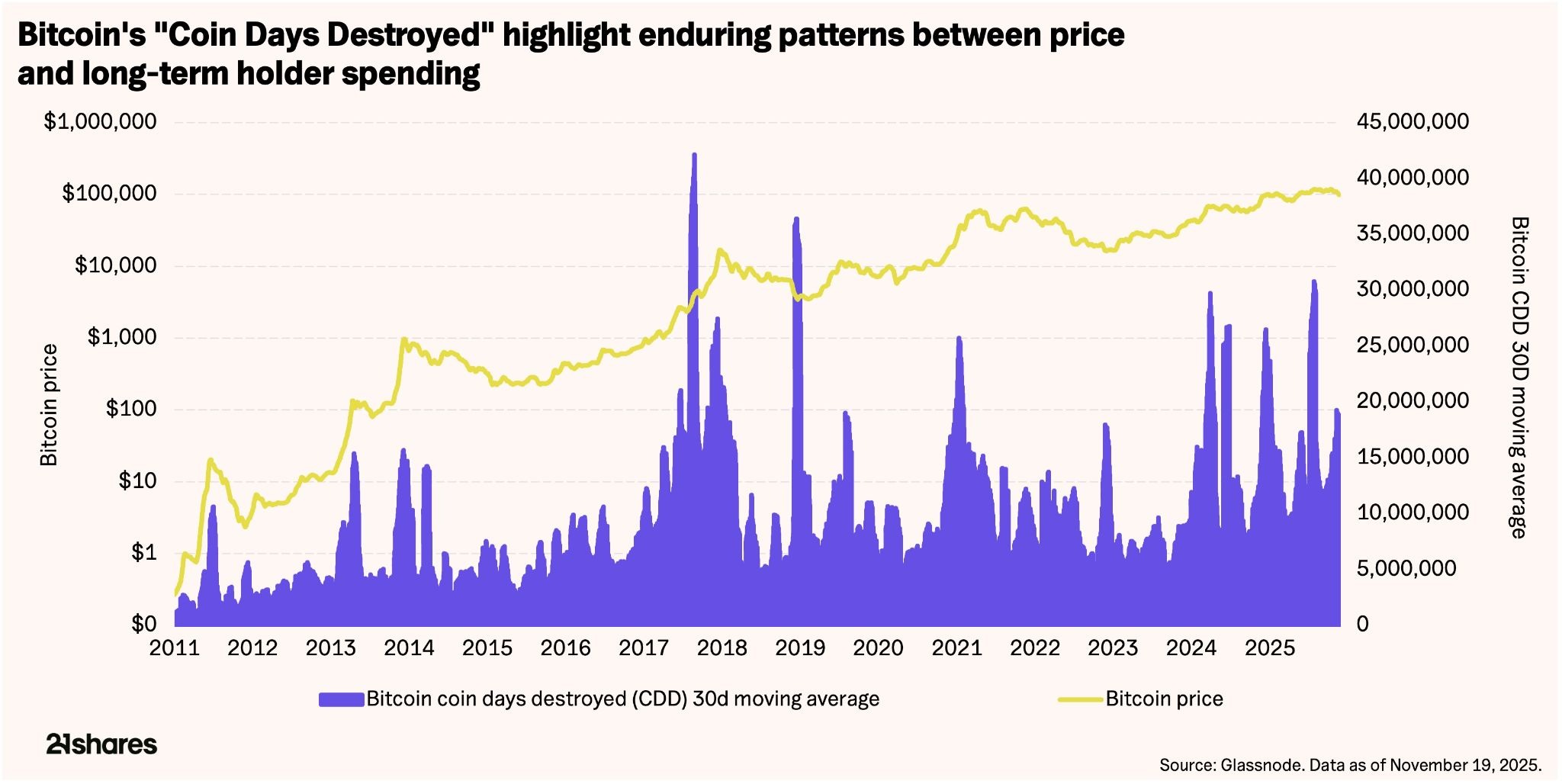

- Coin Days Destroyed, or CDD, which is similar to long-term shareholder turnover, highlighted when long-held coins were spent.

- Broader activity measures such as active addresses, transaction counts, and fee levels rounded out the picture, generally rising during expansions and softening ahead of downturns.

How ETFs changed the market

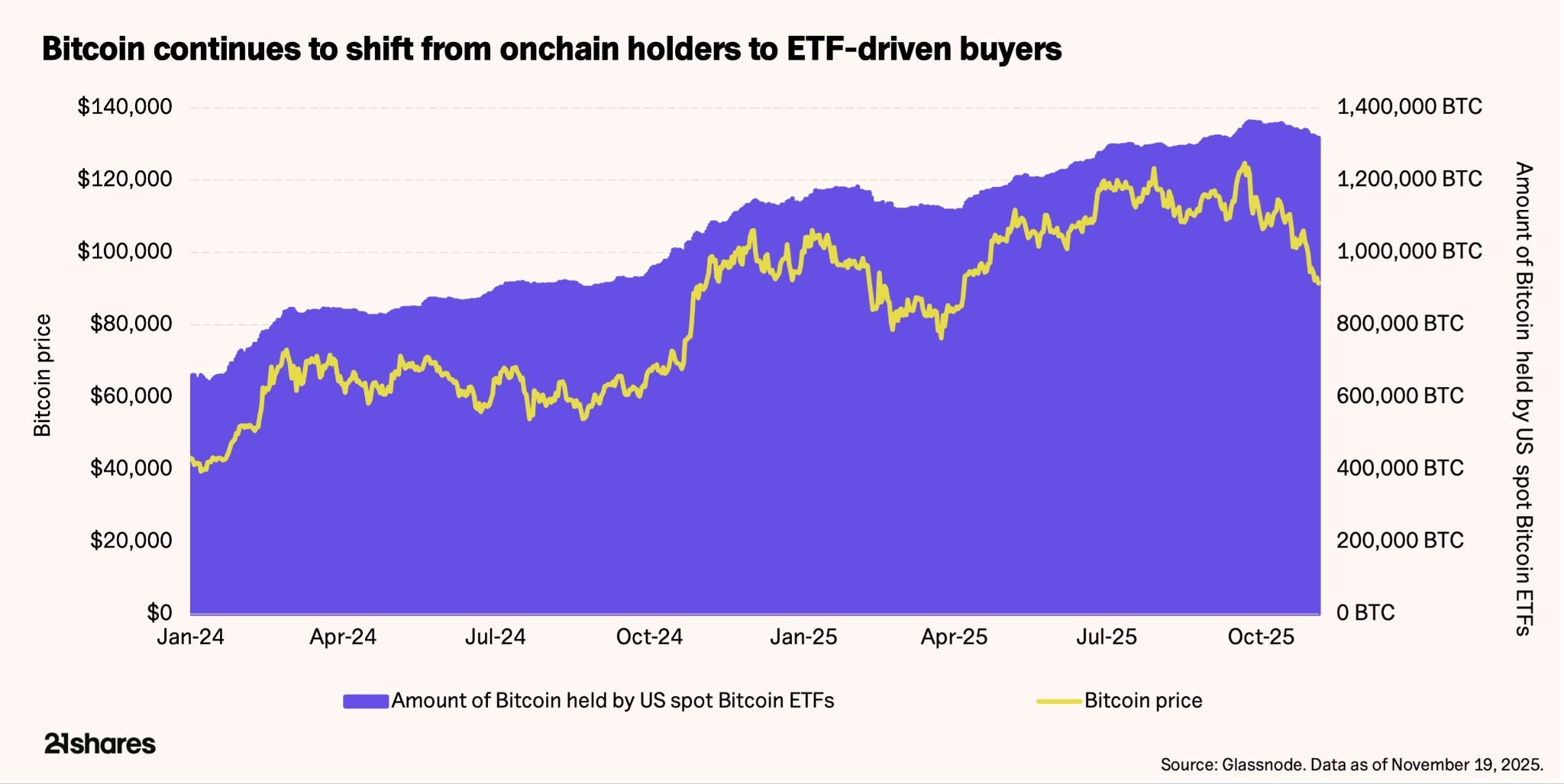

The launch of ETFs changed the Bitcoin valuation landscape: large investors can now enter or exit positions through regulated funds, futures markets, and custodial platforms that leave minimal onchain footprints. A substantial portion of supply and price discovery now takes place through offchain instruments, such as spot and futures funds.

- Since their launch in 2024, US spot Bitcoin funds have accumulated nearly 1.3M Bitcoin, or around 7% of total supply, held in custodial storage.

- At the same time, billions of dollars in Bitcoin exposure now trade on traditional exchanges without any blockchain activity, as shares of these products move between investors in the secondary market.

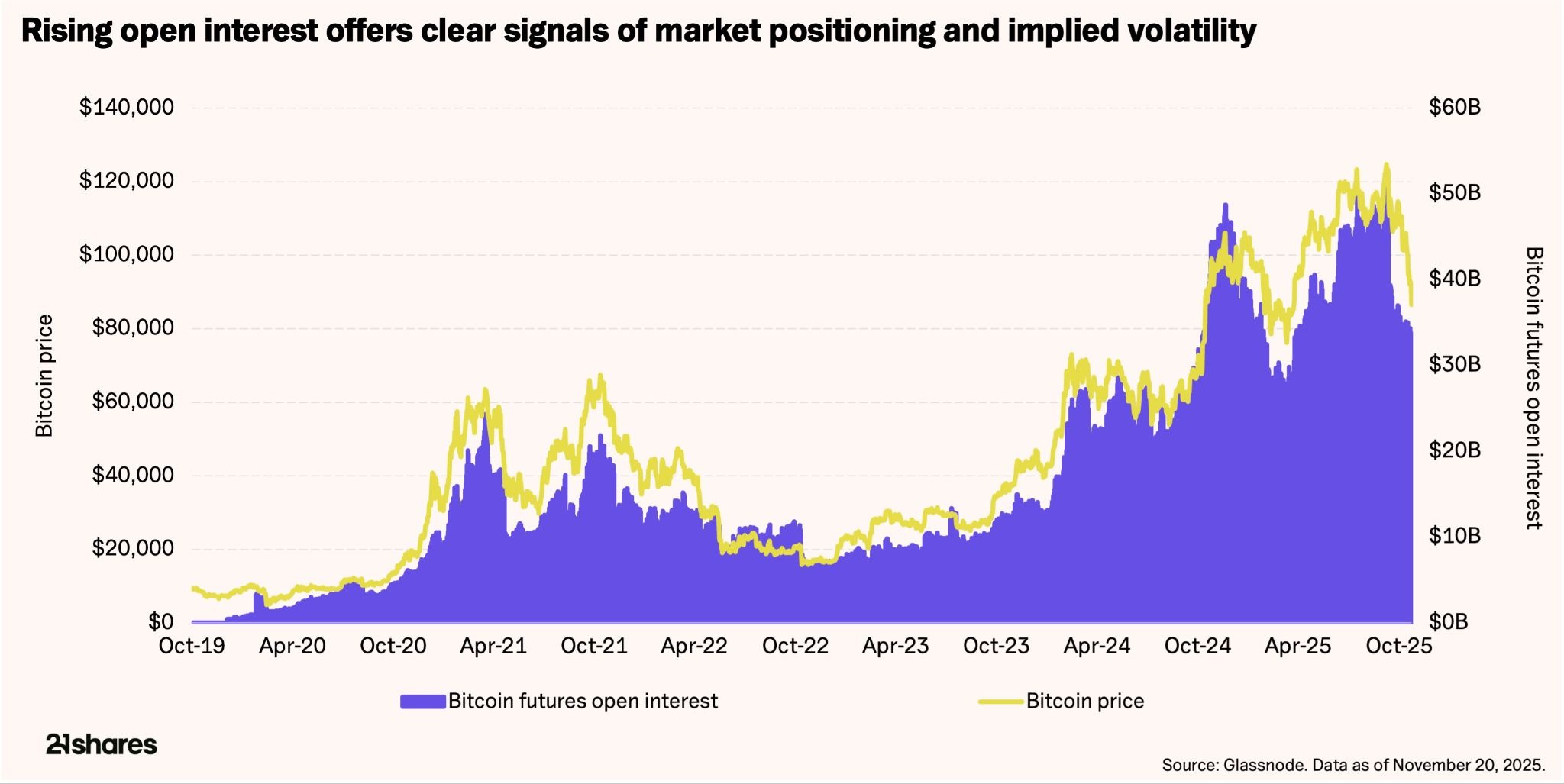

- Futures markets expanded as well. Open interest reached record levels in the beginning of October 20251, allowing market participants to take large positions without moving any coins. Broader macroeconomic forces, including global liquidity conditions and interest rate policy, also became more influential in shaping short-term price movements.

These developments mean that onchain data no longer reflects the entire scope of Bitcoin economic activity. This is because of the growing migration of trading activity to offchain ETF markets, where secondary-market transactions leave minimal onchain footprints. Consider that active addresses peaked at 959K in March 2025 as BTC reached $70K, yet ETF trading volume has jumped over 150% from roughly $2B at launch to exceed levels of $4.5B2. Network usage has declined accordingly: daily transactions have fallen from nearly 500K in December 2023 to about 250K today, and the 30-day average transaction fees have dropped from ~265 BTC prior to 2024 to just 4-7 BTC throughout 20253. This drop in onchain activity has occurred simultaneously to Bitcoin reaching new all-time highs, echoing the idea that some traditional metrics don’t move in step with market value as much anymore.

How traditional onchain metrics behave today

Many of the traditional onchain metrics outlined above, especially those focused on transaction counts, fee levels, or basic NVT ratios, fall short in fully capturing the network’s economic throughput. Though they still provide valuable context, they must be interpreted with the knowledge that a growing portion of Bitcoin’s usage is being intermediated through vehicles that do not settle directly onchain. Let’s look at three onchain metrics and how they fare today:

- The NVT ratio has become less reliable as so much activity now occurs offchain. Elevated readings do not always indicate overvaluation as they once did, and updating the measure to include ETF trading volumes and flows will make it more accurate.

- On the other hand, Coin Days Destroyed (CDD), Bitcoin’s closest equivalent to long-term shareholder turnover, has remained important because it highlights when long-dormant coins begin to move. This often reflects distribution from early investors to new holders. Spikes in this measure have continued to appear around market tops and bottoms, even after the launch of ETFs.

- Activity measures such as active addresses and transaction counts still help gauge network health, but they are not strongly connected to short-term price behavior anymore.

New forms of market data that matter

Gaining a complete view of valuation now requires incorporating both onchain and offchain signals together. The following three offchain indicators are key:

- Daily inflows and outflows offer a near-term view of shifting sentiment (similar to onchain value transfers previously), with steady inflows reflecting strong demand and large outflows often aligning with risk-off behavior.

- Futures market data adds important context, especially as the derivatives market’s open interest has grown by roughly 500% since early 2020 and now represents a much larger share of Bitcoin market structure. Rising open interest often signals upcoming volatility, while shifts in funding rates help show how the market is positioned. Most interestingly, open interest growth of 50-90% has preceded major volatility spikes (Oct 2020–Apr 2021, Oct 2024–Nov 2024, Apr 2025–Oct 2025).

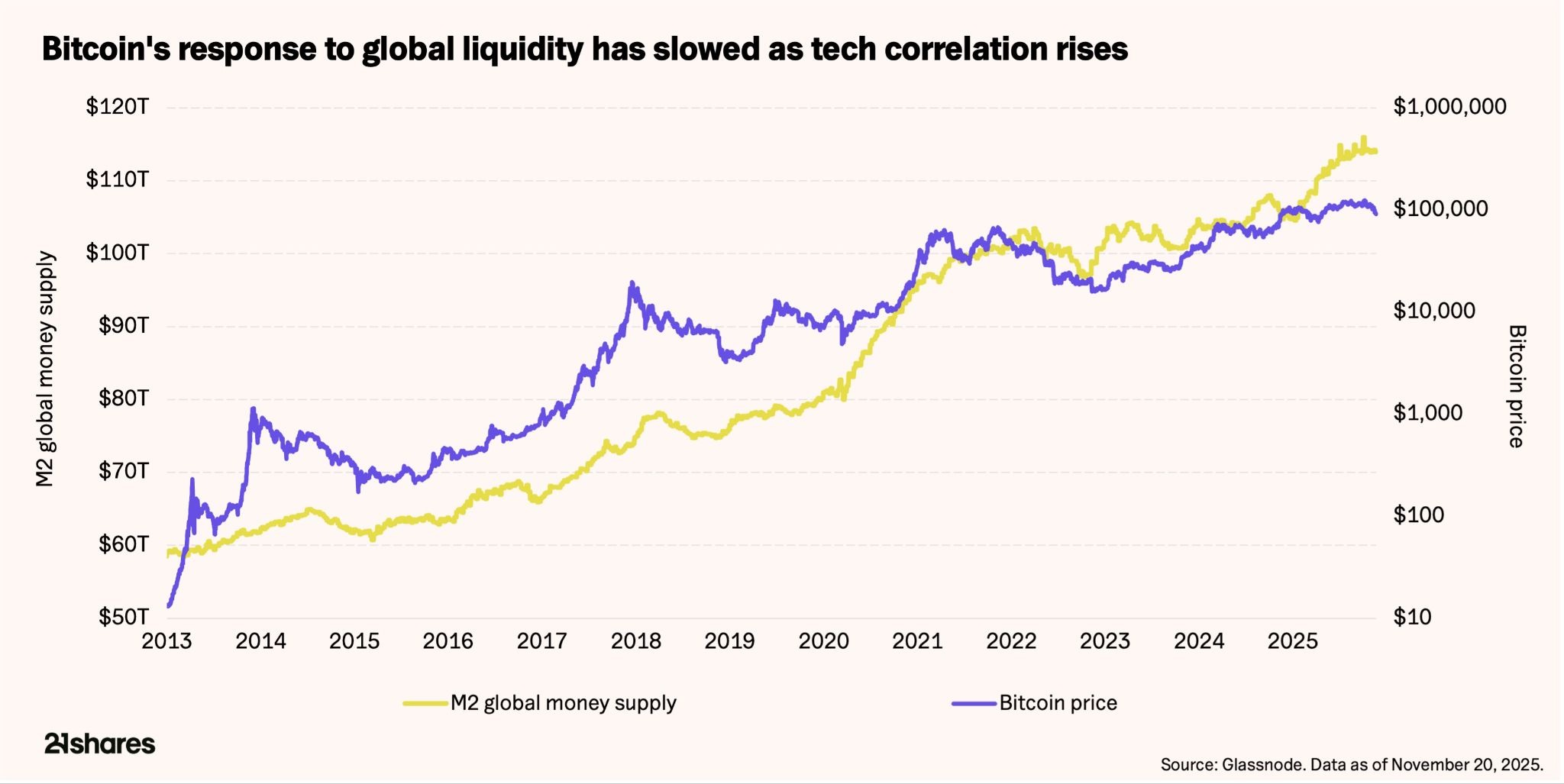

- Similarly, macro liquidity measures such as money supply growth and real interest rates have also gained importance as Bitcoin behaves more like a global risk asset. Its increasing correlation4 with major equity indexes has amplified volatility and made it more sensitive to valuation changes in artificial intelligence-related and broader technology markets, which some view as extended.

Where to from here?

All in all, onchain metrics still provide meaningful insight into cost basis, investor behavior, and long-term cycle trends, but they no longer give a complete view on their own. With more supply held in custodial storage and price discovery increasingly driven by ETFs and futures markets, a more integrated approach is required. Combining onchain fundamentals with fund flows, derivatives positioning, and macro conditions offers a clearer understanding of where Bitcoin stands in its evolving market cycle.

______

Footnotes:

- The Block. https://www.theblock.co/data/etfs/bitcoin-etf/bitcoin-spot-etf-volumes

- The Block. https://www.theblock.co/data/etfs/bitcoin-etf/bitcoin-spot-etf-volumes

- Glassnode. https://studio.glassnode.com/charts/addresses.ActiveCount?a=BTC and https://studio.glassnode.com/charts/fees.VolumeSum?a=BTC

- New Hedge. https://newhedge.io/bitcoin/bitcoin-correlations

This report has been prepared and issued by 21Shares AG for publication globally. All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however, we do not guarantee the accuracy or completeness of this report. Crypto asset trading involves a high degree of risk. The crypto asset market is new to many and unproven and may have the potential not to grow as expected.Currently, there is relatively small use of crypto assets in the retail and commercial marketplace in comparison to relatively large use by speculators, thus contributing to price volatility that could adversely affect an investment in crypto assets. In order to participate in the trading of crypto assets, you should be capable of evaluating the merits and risks of the investment and be able to bear the economic risk of losing your entire investment.Nothing herein does or should be considered as an offer to buy or sell or solicitation to buy or invest in crypto assets or derivatives. This report is provided for information and research purposes only and should not be construed or presented as an offer or solicitation for any investment. The information provided does not constitute a prospectus or any offering and does not contain or constitute an offer to sell or solicit an offer to invest in any jurisdiction. The crypto assets or derivatives and/or any services contained or referred to herein may not be suitable for you and it is recommended that you consult an independent advisor. Nothing herein constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to your individual circumstances or otherwise constitutes a personal recommendation. Neither 21Shares AG nor any of its affiliates accept liability for loss arising from the use of the material presented or discussed herein.Readers are cautioned that any forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors.This report may contain or refer to material that is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject 21Shares AG or any of its affiliates to any registration, affiliation, approval or licensing requirement within such jurisdiction.