The 21.co On-Chain Standard

A Framework for Blockchain (On-Chain) Metrics

Blockchain technology offers unimaginable possibilities for systematically evaluating both fundamentals and the market sentiment of cryptoassets, including Bitcoin and Ethereum, 24/7, 365 days a year, unlike any other asset classes. Dissecting blockchain data is crucial to help the community stay in the know and remain ahead of the curve. Blockchain transparency is undoubtedly an edge to remaining informed in real-time. For example, the early indications of the collapse of Terra's LUNA/UST could be traced back to a single trade on Curve, a decentralized exchange. However, one of the current hurdles for the community is the required expertise of many blockchains and dedicated time to make sense of the underlying data to build metrics, form cutting-edge insights, and make informed decisions. As such, we are thrilled to release this primer on blockchain (on-chain) metrics and introduce the 21.co On-Chain Standard (OS), proposing a novel framework for tactical investors and long-term asset allocators alike to leverage on-chain signals and indicators. Anyone interested in this burgeoning asset class can leverage our real-time dashboards serving as financial statements for Bitcoin and Ethereum and various other blockchain analytics tools here.

Coverage

(1) Introduction to the 21.co On-Chain Standard (OS)

(2) Fundamental Metrics

Protocol Health

- Bitcoin: Block Reward over Time

- Ethereum: Net Issuance

- Bitcoin: Hash Rate and Block Time

- Ethereum: Amount of Staked ETH Financial Statements

- Bitcoin: Active Addresses

(3) Momentum Metrics

PnL Indicators

- Bitcoin: Realized Cap

- Ethereum: Supply in Profit

(4) Relative Valuation

- Bitcoin: MVRV

- Ethereum: Price-to-Fees Ratio

(6) Conclusion

(7) Disclaimer

Introduction to the 21.co On-Chain Standard (OS)

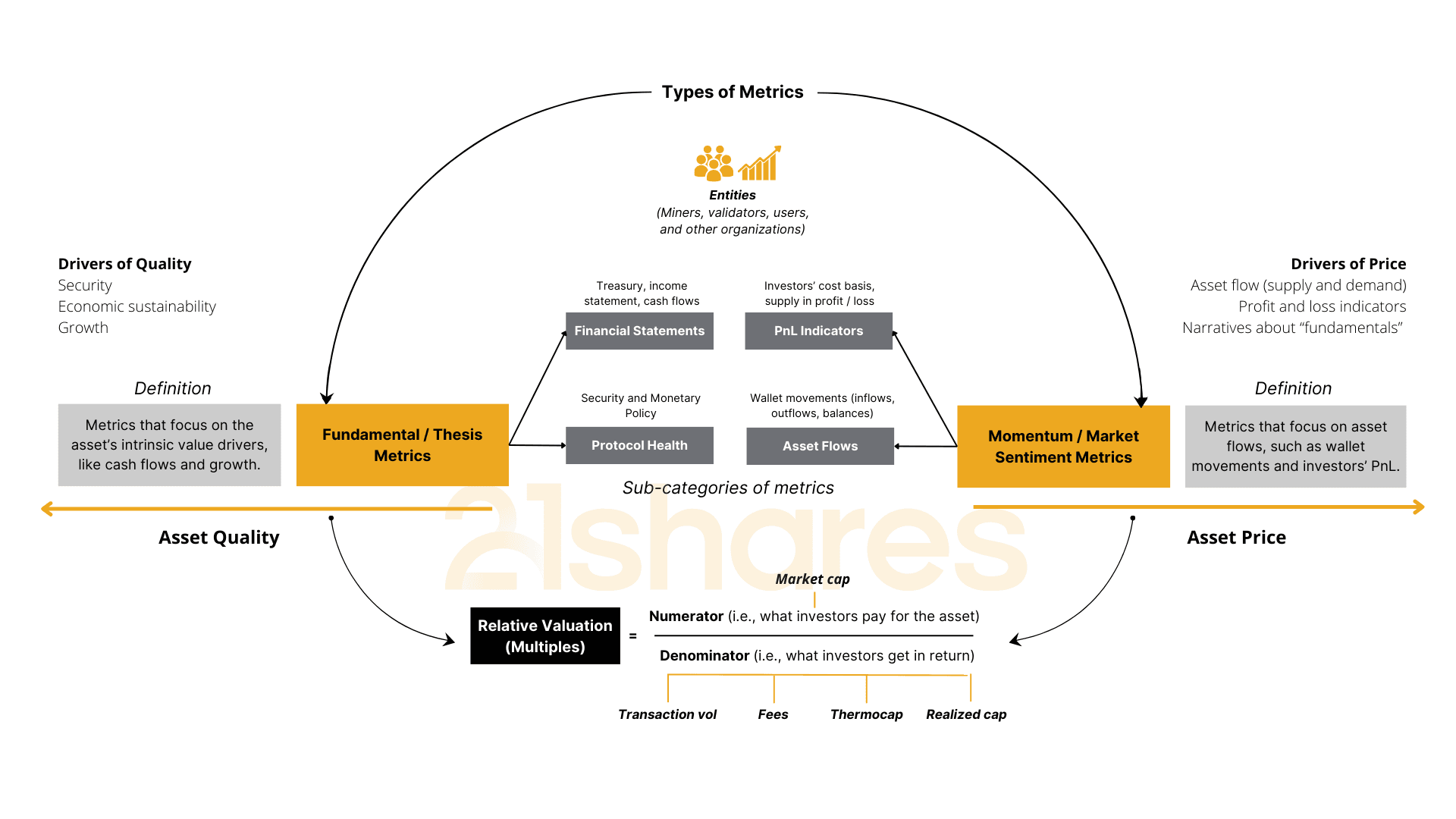

We are pleased to introduce you to the 21.co On-Chain Standard (OS) that organizes blockchain metrics in two buckets: fundamental or thesis-driven metrics and momentum or market sentiment metrics. Market participants can leverage on-chain signals and metrics in real-time to analyze Bitcoin and Ethereum in more depth than is possible with any other traditional asset. The On-Chain Standard enables anyone to have our framework in mind as they navigate this burgeoning asset class.

Figure 1: The 21.co On-Chain Standard (OS)

Source: 21Shares

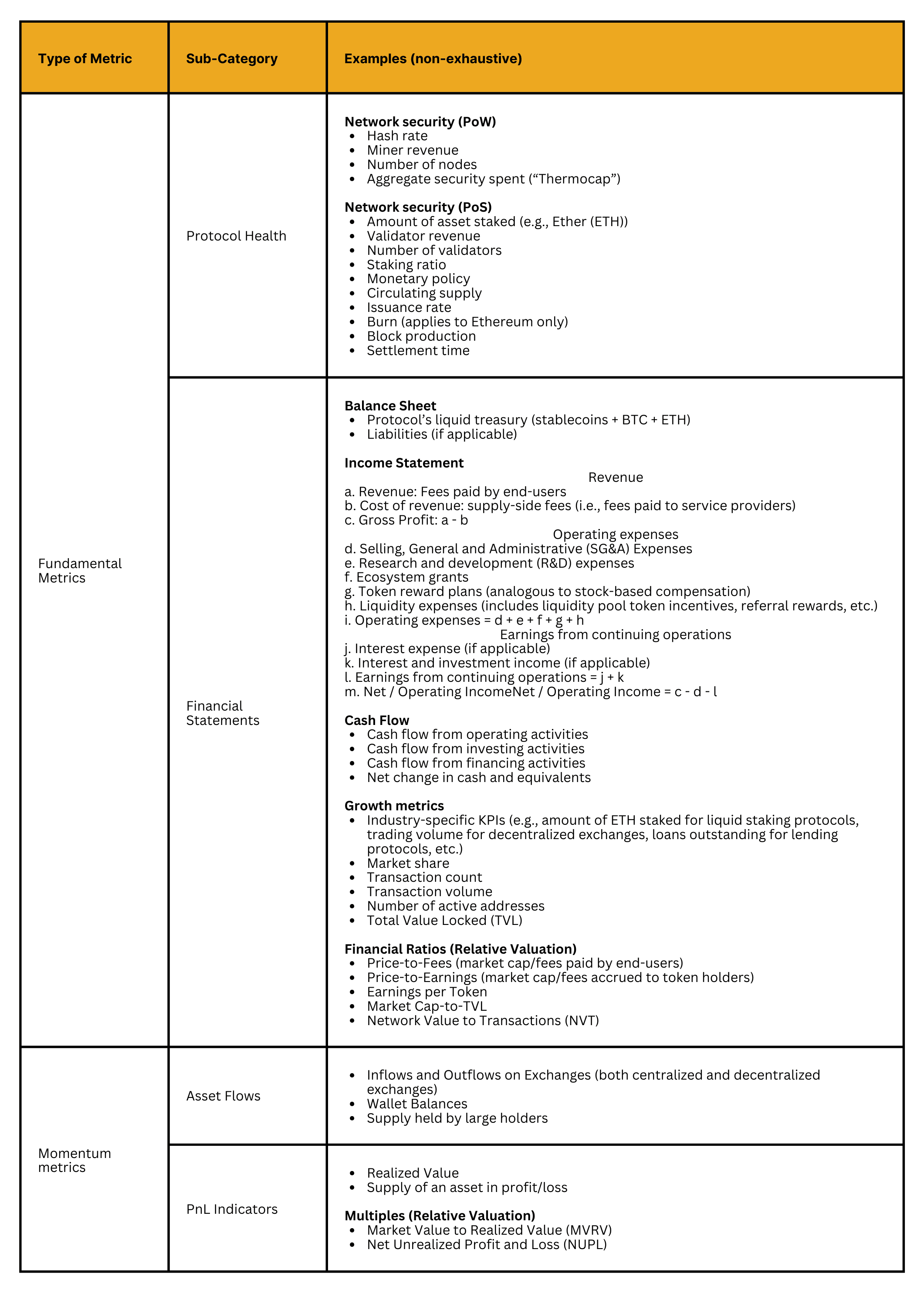

Table 1: On-chain Metrics

Source: 21Shares

While there’s a natural tendency to frame fundamental and momentum metrics as being opposed, both are backward-looking tools that can complement each other, especially for actively managed portfolios. Accessed by any block explorer like Etherscan (akin to a search engine), either in its raw form or through blockchain data services like 21.co real-time dashboards, investors can construct relative valuation ratios to identify short to midterm price inefficiencies.

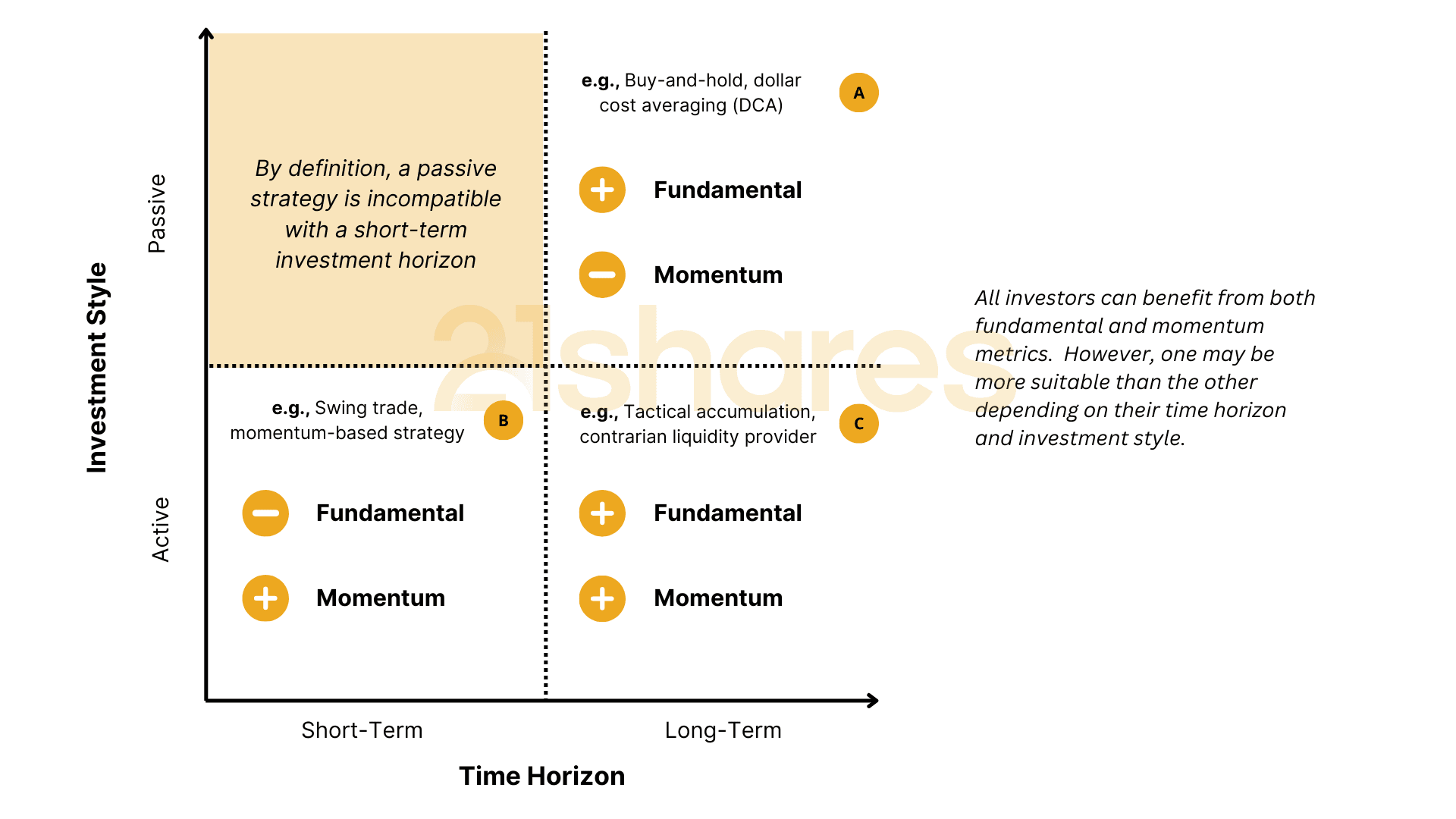

One type of on-chain metrics may be more suitable depending on the investment style and time horizon. Figure 2 represents the On-Chain Matrix (OM) for active and passive investors. The vertical axis refers to the investment style, either active or passive. The horizontal axis describes the time horizon, either short- or long-term oriented.

Figure 2: The On-Chain Matrix (OM) for active and passive investors

Source: 21Shares

First, it’s necessary to note that, by definition, a passive strategy is incompatible with a short-term investment horizon. As such, the On-Chain Matrix includes three quadrants. Let’s explore each in more detail:

- A. Long-term oriented, passive investor: Investors in this quadrant are mostly unbothered by momentum metrics like buyer and seller behavior. They are firm believers in the asset’s fundamentals and future growth prospects, so they tend to focus on fundamentals, including the network’s security and financial statements. The strategies employed include “buy-and-hold” and dollar cost averaging (DCA), meaning investing a fixed dollar amount regularly, regardless of the asset’s price.

- B. Short-term oriented, active investor: Investors in this quadrant constantly monitor momentum metrics to gauge market sentiment and identify short-term price inefficiencies. Although not preoccupied with the long-term prospects of an asset, they often trade based on narratives. This type of investor combines on-chain behavior analysis with market data, including options, futures, and spot data. The strategies employed rely upon mean reversion theory, which assumes that asset prices and historical returns eventually revert to their long-term mean.

- C. Long-term, active investor: Investors in this quadrant are a hybrid between the above extremes. Like investors in quadrant “A,” they are bullish on the asset’s long-term fundamentals. Conversely, like investors in quadrant “B,” they attempt to identify short- and medium-term price inefficiencies that can serve as an opportunity to accumulate more units of the underlying asset. As a result, they must monitor fundamentals and momentum metrics equally. This type of investor often goes against consensus, acting as a long-term but tactical asset allocator (i.e., buy when everyone is selling, sell or take profit when everyone is buying).

Now that we’ve outlined a framework that enables investors to leverage on-chain metrics based on their investment style and time horizon, we’ll explore some examples of each category for Bitcoin (BTC) and Ether (ETH).

Fundamental Metrics

Protocol Health

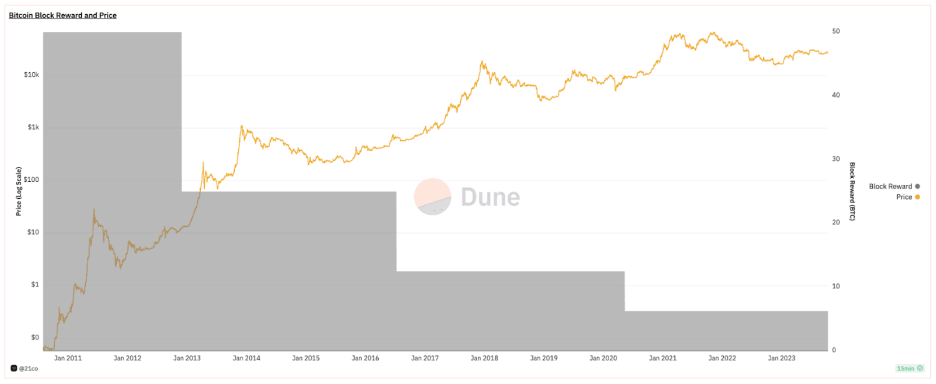

Bitcoin: Block Reward over Time

The Bitcoin protocol has ensured monetary integrity by allowing analysts and investors to track BTC’s total circulating supply and daily issuance, as shown in Figure 3. From Bitcoin’s inception, monetary policy has been pre-determined and encoded in its protocol, making it predictable and verifiable. The rate at which new Bitcoin is created decreases by half for every 210,000 blocks mined — roughly every four years. As per Bitcoin's halving dates history, the last three halvings occurred in 2012, 2016, and 2020, with a current reward of 6.25 BTC per block.

Figure 3: Bitcoin Block Reward and Price

Source: 21Shares Dune dashboard powered by 21.co (parent company)

Ethereum: Net Issuance

Over 3.5 million ETH worth over $10 billion has been burned (removed from circulation) since EIP-1559 went live in August 2021, helping Ether become a deflationary asset in 2023. Since Ethereum transitioned to a Proof-of-Stake consensus mechanism in September 2022, the network’s energy consumption has been reduced by >99%, and ETH’s new issuance has dropped by over 80%. Despite the current period of relatively dampened activity, ~$1.45 billion worth of ETH has been burned in 2023, increasing its prospects as a deflationary asset.

Figure 4: Ether’s prospects as a deflationary asset

Source: 21Shares Dune dashboard powered by 21.co (parent company)

Bitcoin: Hash Rate and Block Time

Bitcoin’s security is guaranteed by miners, who ensure transactions are valid and irreversible. The hash rate measures miners' processing power to secure the network from attacks. All else equal, rising hash rate levels increase the network's security and robustness.

Figure 5 shows the immediate effect of the May 2021 China ban on Bitcoin’s hash rate and block (or settlement) time. This geopolitical event impacted the short-term security of the network since the miners elsewhere in the world were taking longer to confirm transactions (50% increase from ~10 to ~15 minutes), increasing the likelihood of a transaction reversion.

Figure 5: Bitcoin Block Time and Hash Rate

Source: 21Shares Dune dashboard powered by 21.co (parent company)

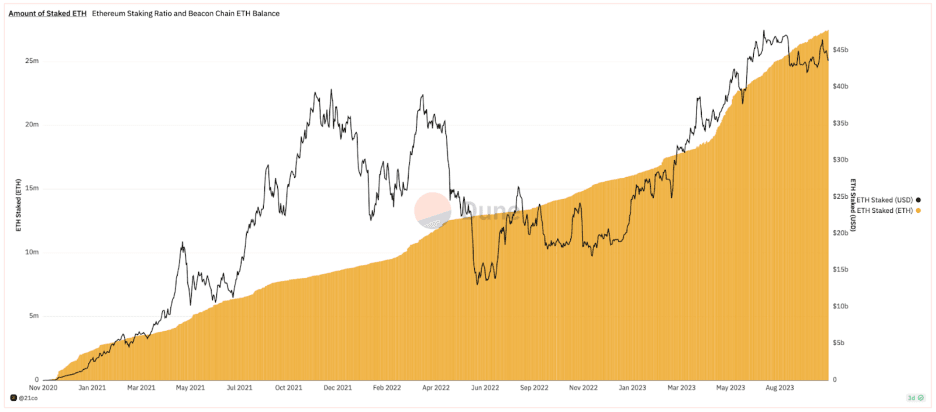

Ethereum: Amount of Staked ETH

In a Proof-of-Stake (PoS) blockchain, validators contribute to the security of the network by committing a portion of their capital (the “stake”) to attest that a block of transactions is valid. The most significant risk to staking is "slashing" or losing a portion of the principal staked balance due to being deemed a "bad actor" on the network. Slashing creates a negative incentive to prevent validators from behaving maliciously. PoS is much less computationally intensive and requires vastly less energy than Proof-of-Work (PoW) networks like Bitcoin. In return for securing the network, validators get a constant revenue stream from two sources: (1) transaction fees and (2) token issuance.

Validators have accrued over $350 million in transaction fees (net after burn) in the past year, showing that demand for Ethereum as a global computing platform for decentralized applications is unmatched. Moreover, validators have received $1.17 billion in new issuance in the past year, putting annualized flows (fees + issuance) at $1.52 billion. These economic incentives, combined with the de-risking of ETH staking by enabling withdrawals in April 2023, have contributed to Ethereum being the most secure smart contract platform, with over $45 billion staked ETH securing the network.

Figure 6: Amount of Staked ETH

Source: 21Shares Dune dashboard powered by 21.co (parent company)

Financial Statements

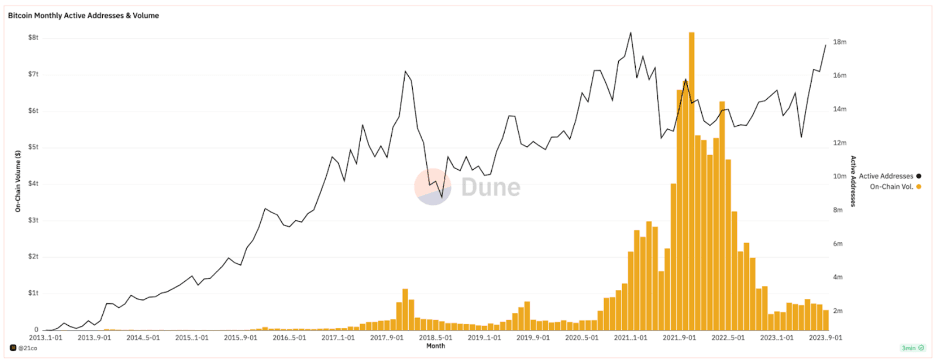

Bitcoin: Active Addresses

Bitcoin’s monthly active addresses surpassed 16.8 million in September 2023, the highest figure since March 2021, when BTC was trading close to its all-time high price. The surge results from new use cases on the network continuing to gain traction, such as Ordinals NFTs and smart contracts.

Figure 7: Bitcoin Monthly Active Addresses and Volume

Source: 21Shares Dune dashboard powered by 21.co (parent company), Data as of September 30, 2023

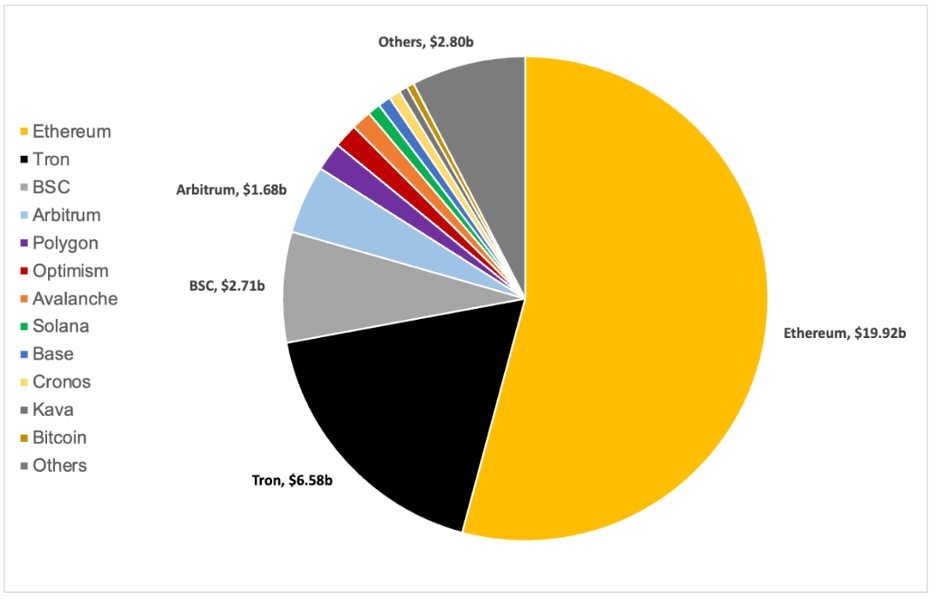

Ethereum: Total Value Locked (TVL)

Total value locked (TVL) is a measure of the total dollar-denominated value deposited in a platform or application, akin to assets under management (AuM). Ethereum remains crypto’s financial hub, with over 50% of all TVL, followed by Tron and Binance’s BSC.

Figure 8: Total Value Locked (TVL) across all networks

Source: DeFi Llama. Data as of October 16, 2023

Momentum Metrics

This section focuses on asset flows, assessing BTC and ETH holders’ positions and cost basis at any point in time. The relative value of a cryptoasset is a function of the supply and demand dynamic. Over long time horizons, the demand for BTC and ETH has trended upwards, but over shorter time periods, it has fluctuated dramatically. Based on on-chain data, investors can assess the variability of demand and its likely impact on price, by analyzing the behavior of buyers and sellers at any point in time.

PnL Indicators

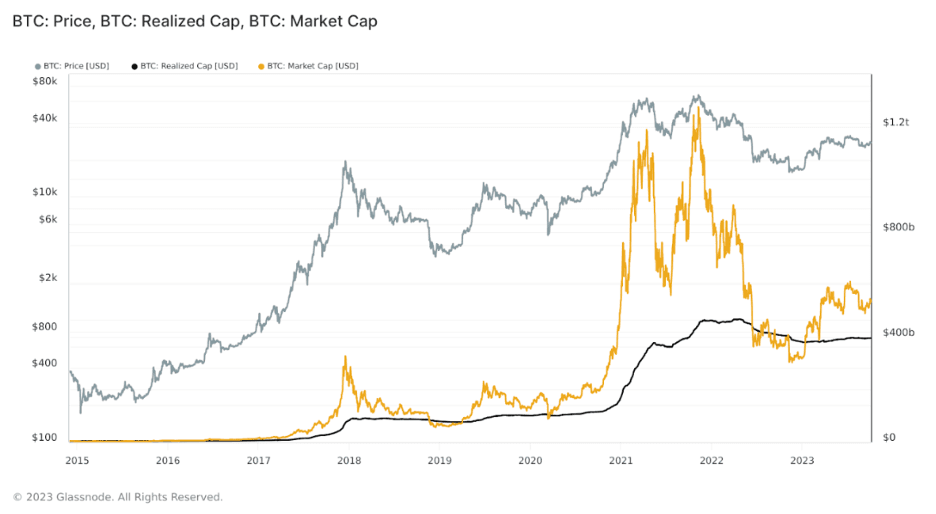

Bitcoin: Realized Cap

First conceptualized by Nic Carter and Antoine Le Calvez in 2018, realized capitalization (realized cap) is the average cost basis of all BTC in circulation, valuing each BTC at the price of its last movement. Whenever the market cap drops below the realized cap, the overall BTC market is selling at a loss, suggesting capitulation. Today, Bitcoin’s market cap is roughly $546 billion, about 1.38 times its approximately $396 billion realized cap, as shown in Figure 8.

Figure 9: BTC market cap and realized capitalization

Source: Glassnode, as of September 30, 2023

Ethereum: Supply in Profit

Supply in profit/loss measures the number of outstanding ETH with a profit or loss relative to their last transaction. Today, the percent supply of ETH at a profit is roughly 45%. Whenever the percentage of supply in profit goes below 50%, it has historically been near the bottoming process of the asset’s price.

Figure 10: Percent Supply in Profit

Source: Glassnode, As of September 30, 2023

Relative Valuation

A significant portion of equity valuations in traditional finance consists of relative valuations based upon market sizing and multiples, such as price-to-earnings (P/E ratio). Investors can use relative valuations to "price" or estimate how much to pay for an asset based on what others pay for similar or comparable assets. We can combine the on-chain metrics in the previous sections to identify short- and medium-term price inefficiencies.

Bitcoin: MVRV

The market-value-to-realized-value (MVRV) created by Murad Mahmudov & David Puell (Researcher at ARK) hot on the heels of the invention of Realized Cap by the Coinmetrics team of Nic Carter and Antoine Le Calvez — is a simple yet powerful on-chain multiple that leverages the transparency of the blockchain:

- "Market value" refers to the current value of supply (market cap);

- "Realized value" refers to the cost basis of supply (realized cap).

High MVRV values indicate a substantial degree of unrealized profits in the system. In contrast, values below "1" indicate that a significant portion of BTC's supply is near break-even or at a loss. Historically, high MRVR ratios have coincided with BTC market tops, while values below "1" have preceded past cycles' bottoms. BTC's MVRV ratio broke above the "1" mark in January this year. The last time this happened was in March 2020, marking the beginning of the previous cycle's meteoric bull run.

Figure 11: Bitcoin’s Market Value to Realized Value (MVRV)

Source: Glassnode

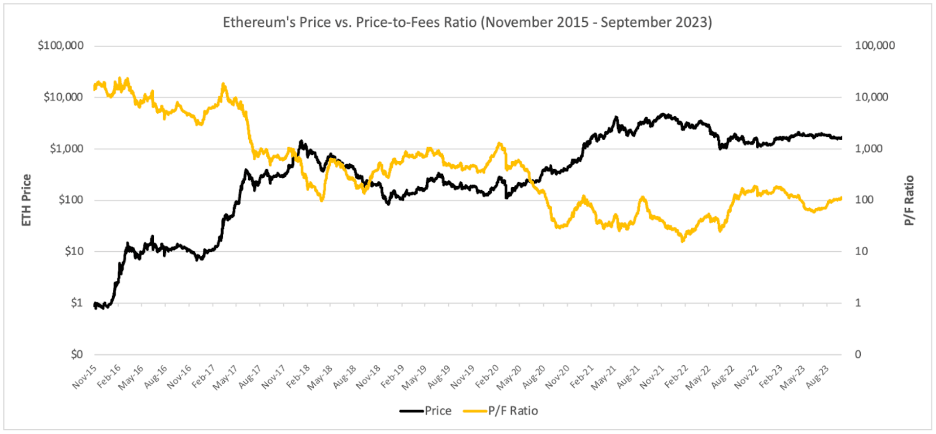

Ethereum: Price-to-Fees Ratio

Similar to traditional finance's Price-to-Sales (P/S) ratio, we can compute Ethereum's Price-to-Fees (P/F) ratio. In each cycle expansion, we see an inverse relationship between ETH's price and its price-to-fees ratio — a plausible interpretation is that, as ETH's price increases, it creates a virtuous cycle whereby new users come in, and with growing activity comes more significant protocol revenue. Crucially, ETH's price tends to bottom when the P/F ratio reaches its previous cycle bottom. If we follow this pattern, we could expect the P/F ratio to drop below 10 in the next expansion. For reference, Tesla and Apple have P/S ratios of roughly 9 and 7, respectively.

Figure 12: Ethereum’s Price-to-Fees (P/F) Ratio

Source: 21Shares. Data from Glassnode, as of September 30, 2023

Conclusion

Bitcoin and Ether do not resemble traditional assets, so many investors are grappling with ways to analyze them fundamentally. While conventional analytical frameworks may not be suitable, the Bitcoin and Ethereum blockchains offer a unique set of tools investors can leverage to assess its fundamentals and the behaviors and cost basis of investors. Similar to a public company publishing a quarterly earnings report with financial statements, Bitcoin and Ethereum provide a real-time, transparent ledger that publishes data about the network’s activity and inner economics. Without central control, Bitcoin and Ethereum’s blockchains provide open-source data verified by thousands of nodes worldwide. Investors increasingly will appreciate BTC and ETH investment merits through on-chain analysis.

Disclaimer

The information included herein is the express opinion and experience of 21Shares and is provided for discussion purposes only. Past performance is not indicative of future results. Investors should consult with their own advisors for legal, tax, regulatory, financial, accounting, and other aspects relevant to the investment's suitability and potential consequences.

This presentation is for informational and discussion purposes only and does not constitute an offer to sell or a solicitation of an offer to purchase any security. The information set forth herein does not claim to be complete and is subject to change. This presentation does not constitute a part of any document of any fund and should not be construed as an advertisement or marketing material for any fund.

Certain statements contained in this presentation are based on the expectations, estimates, projections, and opinions of 21Shares. Such statements involve known and unknown risks, uncertainties, and other factors, and reliance should not be placed thereon. This presentation contains “forward-looking statements,” the outcome of which may differ materially from those reflected or contemplated herein.

Certain economic, market, financial, and other information contained herein has been obtained from managers, service partners, and other parties besides 21Shares. While such sources are believed to be reliable, none of 21Shares or any of their respective affiliates or employees assumes any responsibility for the accuracy or completeness of the information contained in this presentation or to update any information contained herein.

Investing in crypto assets, including cryptocurrencies and crypto tokens, carries inherent risks. These assets are considered highly speculative due to their limited history and new technological nature. Future regulatory actions may impact the usability and tradability of crypto assets. The price of crypto assets can be influenced by a small number of holders and may decline in popularity or acceptance, affecting their value.

None of 21Shares nor any of its affiliates have made any representation or warranty, express or implied, with respect to the fairness, correctness, accuracy, reasonableness or completeness of any of the information contained herein (including but not limited to information obtained from third parties), and expressly disclaim any responsibility or liability relating thereto.

.svg)