Primer: Ethereum, The Global App Store for the Next Generation of Internet Services

Executive Summary

This research primer acts as a guide for investors to understand Ethereum fundamentally. You will learn how the technology works, discover the current and future state of Ethereum, the different ways to value the asset, and finally assess its various associated risks.

Ethereum represents the most significant single innovation within the cryptoasset and blockchain industry since the creation of Bitcoin in 2009. While Bitcoin was the world’s first decentralized, peer-to-peer digital currency and is considered the world’s first digital gold, Ethereum was the first global computing platform analogous to an App store in a smartphone, allowing developers and entrepreneurs to launch decentralized internet services. Ethereum’s key feature is smart contracts, computer programs on a blockchain that enable users to program financial assets and applications.

With around 6,000 monthly active developers as of October 2023, Ethereum is the world’s largest developer ecosystem. Moreover, various private and central banks explore and experiment with the platform, including the Monetary Authority of Singapore (MAS), Societe Generale, and the European Central Bank’s investment arm. Since its launch in 2015, Ethereum has driven the evolution of the blockchain space with innovations, ranging from decentralized finance (DeFi), non-fungible tokens (NFTs), digital identity solutions, and the tokenizations of real-world assets like equities. Some of the most important innovations that have come out of DeFi include ‘stablecoins,’ decentralized exchanges (DEXs), and automated lending protocols. Stablecoins maintain price parity with a target asset, such as the U.S. dollar. Decentralized exchanges (DEXs), such as Uniswap, allow users to trade assets without the need for an intermediary against an “automated market-maker” (AMM) algorithm, settling trillions of dollars of value since their inception. As a final example, overcollateralized lending protocols like MakerDAO, Aave, or Compound have taken traditional credit risk out of the equation, relying instead on smart contract automation and operators to liquidate loans when the collateralization ratio falls below a predetermined threshold. These and many other DeFi innovations reveal one of the core value propositions of Ethereum – the ability to act as a credibly neutral settlement layer where developers can automate away the need for centralized intermediaries and give power back to the individual.

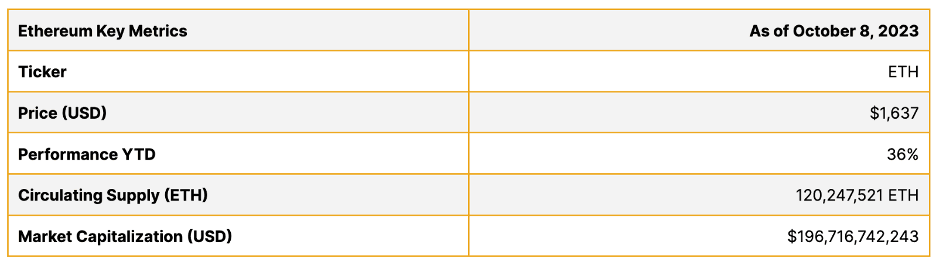

Table 1: ETH Key Metrics

Data Source: CoinMetrics

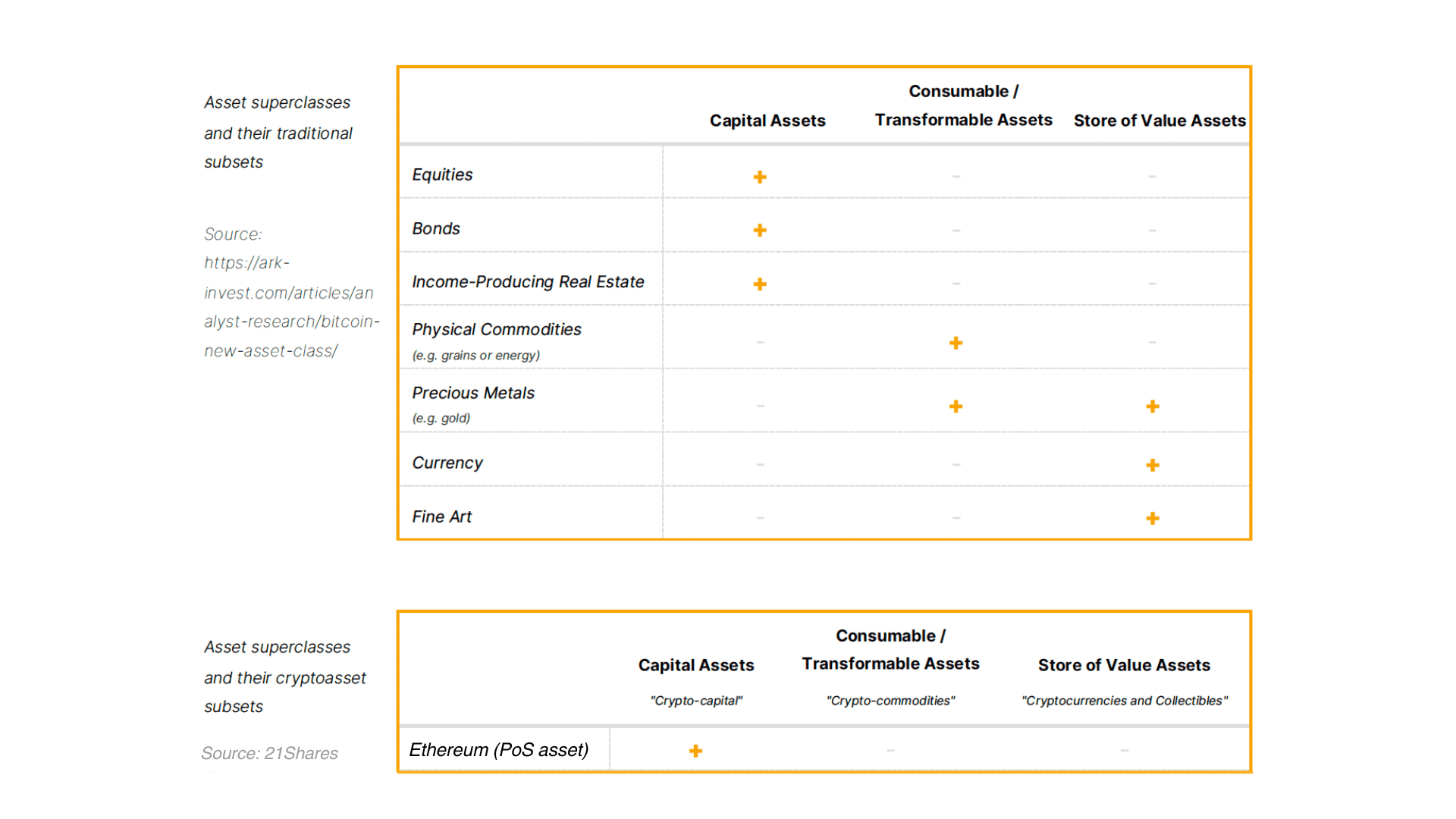

Figure 1: Asset Superclasses

Source: 21Shares

How Ethereum Works

Smart Contracts

As mentioned, the critical innovation behind Ethereum is its smart contracts. The latter are self-executing contracts between different users, representing an agreement over assets on the Ethereum blockchain. This contract is encoded into the Ethereum blockchain. Smart contracts are essential as they allow users to create complex financial instruments and self-enforcing contracts that exist on a decentralized blockchain. Because of this invention, users and engineers can easily make unique financial instruments in the form of tokens, fundraising agreements, lending, and market-making platforms, which all exist on the Ethereum blockchain in a public and transparent way. Therefore, the value of Ethereum in the long term is likely to be tightly coupled with the demand for smart contracts. Since Ethereum’s launch in 2015, the platform has seen a pronounced evolution of the smart contracts deployed. For example, in 2017, the cryptoasset bubble was primarily driven by the boom in the issuance of initial coin offerings (ICO) smart contracts. In contrast, since 2019, various decentralized finance applications, such as stablecoins, lending, and market-making apps, have been the primary growth area within smart contract development.

Ether

Integral to the cryptoasset’s success is Ether, the underlying currency that drives Ethereum’s functioning. In other words, Ether is the fuel of the Ethereum blockchain to function seamlessly. We use Ethereum (the network and blockchain) and Ether (the native currency) interchangeably. Still, Ether is the currency used to pay for transactions on the Ethereum blockchain and issue smart contracts. Users who wish to execute smart contracts and engage with financial contracts on Ethereum must pay for such transactions with Ether, so demand for smart contracts is closely tied to demand for Ether. In addition, several smart contracts require Ether to be deposited to fulfill their functions. For example, decentralized lending or stablecoin platforms on Ethereum often require investors to deposit Ether as collateral. Thus, the cryptoasset can be seen as analogous to the role oil plays within the global economy; increasing globalization and economic integration led to oil becoming a more demanded resource. As we will discuss later, the role of Ether has slightly changed after Ethereum transitioned from using Proof of Work mining to using Proof of Stake — where staking uses deposits of Ether rather than computing power with supercomputers and electricity.

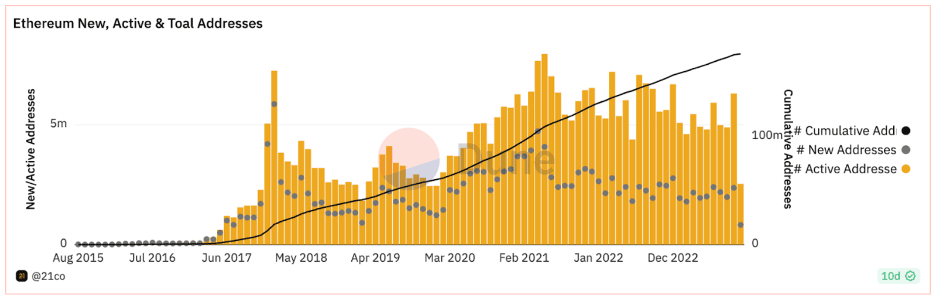

Figure 2: Ethereum New, Active and Total Addresses

Source: 21.co - Dune Analytics

The State of Ethereum

The closest analogy to investing in Ethereum is if Silicon Valley had a token representing the value of supporting the functioning of their ecosystem for startups to solve crucial problems. Potentially, Ethereum’s total addressable market (TAM) includes any industry that could build services and products on the Internet. While financial services (DeFi) is the most dominant sector on Ethereum, many more use cases are emerging, such as Non-Fungible Tokens (NFTs), blockchain-based games, and the tokenization of “real-world” assets. It’s important to note that these applications are non-custodial, meaning that the cryptoassets are stored on the Ethereum blockchain and controlled by users. Since the start of the DeFi ecosystem in the summer of 2020, the sector has experienced massive growth with more than 200 startups, billions of dollars worth of value transferred, and disrupting markets such as trading, lending, remittances, and more. This innovation provides 24/7 availability and transparency, and reduces censorship, costs, and certain counterparty risks. But, of course, none of this would be possible without Ethereum.

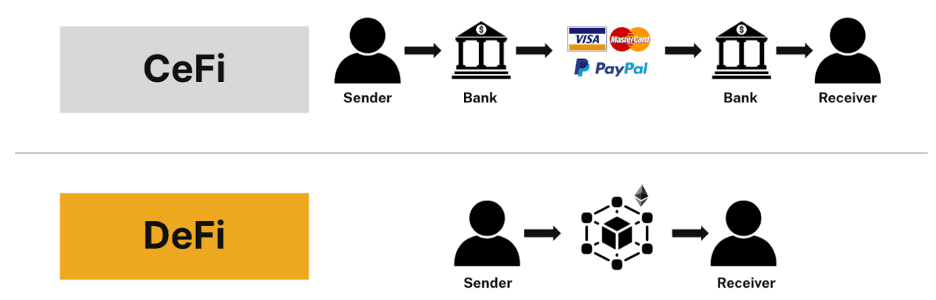

Figure 3: Centralized Finance vs. Decentralized Finance

Source: 21Shares

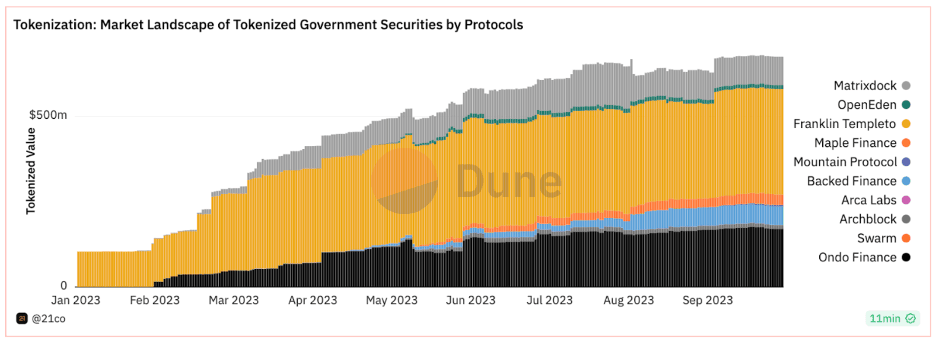

The tokenization of traditional financial products is another flourishing sector. Especially tokenized U.S. Treasuries have witnessed a remarkable growth of over 450% this year, with a total of $650 million in assets. The rise of on-chain U.S. treasuries can be attributed to the prevailing high-interest-rate environment. Issuers include crypto natives such as Ondo and Backed Finance, alongside well-established traditional finance players like Franklin Templeton. While these platforms harness the power of public blockchain technology, accessibility remains confined by the requisite onboarding process involving KYC/AML (Know Your Customer/Anti-Money Laundering) procedures or geographical limitations. Although this may appear counterintuitive to the ethos of crypto, given the current limited accessibility, this issue is likely to be resolved through technological and regulatory advancements. Moreover, it also aligns with our thesis that innovation primarily occurs in the backend infrastructure, exemplified by the utilization of a public blockchain for settlements and tokenization.

Figure 4: Market landscape of tokenized government securities by protocols

Source: 21.co – Dune Analytics

Ether is the second-largest cryptoasset globally, with a 30-day average trading volume of $52 billion, alongside over 1 million daily transactions processed on the Ethereum blockchain. On the institutional adoption front, Rothschild Investment Corporation invested over $4 million in Ether while the European Union’s investment arm, the European Investment Bank, issued bond tokens on Ethereum. T-Mobile Parent Deutsche Telekom reportedly launched an Ethereum validator and staking support, and many financial institutions, such as Deutsche Bank, started to offer crypto custody solutions. Fintech giant PayPal also issued a USD-pegged stablecoin on the Ethereum blockchain, citing a “shift toward digital currencies.” The total addressable market for Ethereum will expand over time as innovation keeps coming out. For example, UNICEF operates an innovation unit composed of initiatives for social good, including efforts to explore the possibility of DeFi to open access to financial services for the unbanked.

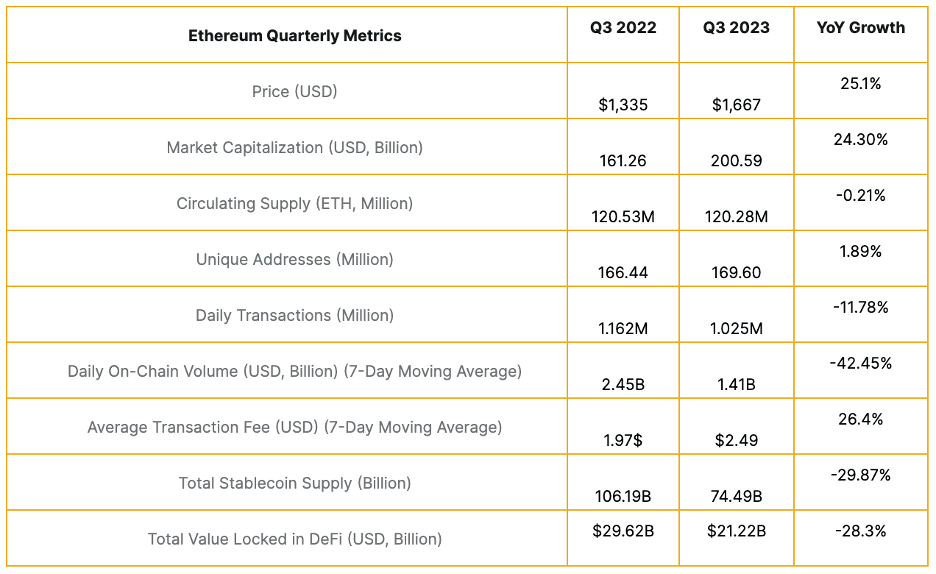

Table 2: Ethereum Quarterly Metrics (Source: Etherscan, CoinMetrics, DeFi Llama)

Source: Coinmetrics, Defillama, Tokenterminal, Dune Analytics

The Future of Ethereum

Ethereum stands out in the cryptoasset industry for having an incredibly ambitious roadmap. Several crucial upgrades have been successfully deployed, with others awaiting implementation. As technology advances, the Ethereum roadmap is subject to changes. However, its present focus centers on the following key components: cheaper transactions, extra security, and better user experience.

One of the most important milestones was “The Merge.” In September 2022, Ethereum transitioned from a Proof-of-Work (PoW) to a Proof-of-Stake (PoS) consensus mechanism. This pivotal moment set the foundation for improved scalability and efficiency, notably reducing Ethereum’s energy consumption by ~99.99%. In a PoS network, validators contribute to the network’s security by committing a portion of their capital (the “stake”) denominated in its native asset (ETH) to attest that a block of transactions is valid. With more than 860,000 validators securing the blockchain as of October 2023, Ethereum is the single most decentralized smart contract platform. As developers continue to integrate decentralized applications with existing financial software, merchants, consumers, and institutions worldwide will gradually adopt the network for payments, trading, identity solutions, digital provenance, and a variety of other applications. In conclusion, Ethereum is set to play its role as a global, neutral, and decentralized App store for the digital age.

We’ll now expand on the four critical elements of the future of Ethereum — Layer 2 scalability efforts, EIP-1559, and EIP-4844.

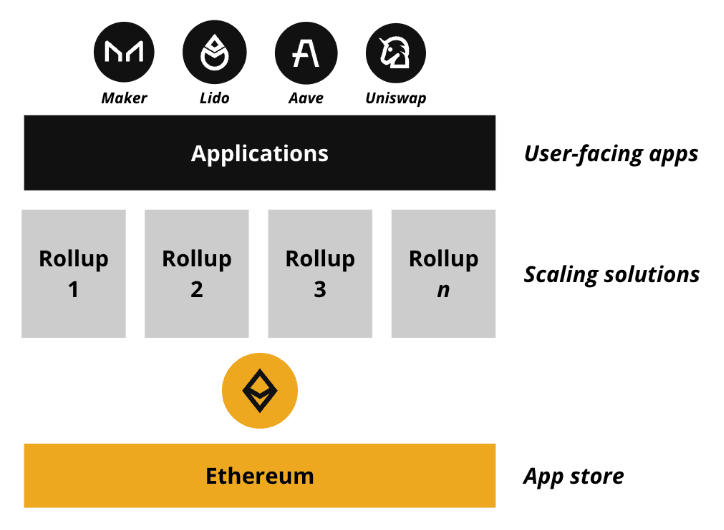

Scaling Solutions Also Called Layer 2

Figure 5: Ethereum’s scaling architecture

Source: 21Shares

One of Ethereum's limitations is the capacity to process thousands of transactions per second due to its decentralized architecture. Compared with the Visa network, processing over 2,000 transactions per second, Ethereum is limited to roughly 50 transactions per second. As such, scalability is one of the key elements on the Ethereum roadmap.

In Ethereum's initial roadmap, there was a concept known as "shard chains." Sharding involved partitioning the Ethereum blockchain, where individual subsets of validators would be accountable for specific portions of the overall data. While this was originally intended to help Ethereum to scale, so-called “Layer 2” solutions have developed much faster and better than expected and will improve even more after Proto-Danksharding is implemented. Layer 2 refers to technologies built on top of Ethereum’s base protocol, which allows for improved scalability of the Ethereum blockchain without reducing its economic security and sacrificing its decentralization nature. Consequently, sharding is no longer needed and has been dropped from the roadmap. Below, we list a few examples of Layer 2 technologies either already built on Ethereum or currently being built:

- Zero-Knowledge-based and Optimistic Rollups: Two different approaches that involve compressing (or “rolling-up”) several Ethereum transactions into a single transaction to improve scalability. Examples: Optimism, Arbitrum, Base, Starkware, zkSync, Polygon zkEVM, Scroll EVM and Linea.

- Plasma and Sidechains: Methods that aim to enable fast and cheap transactions by offloading Ethereum transactions to a blockchain (or “sidechain”) that connects to the main Ethereum blockchain. Examples: Polygon PoS, Gnosis Chain, and Skale.

- State and Payments Channels: Methods that enable faster transactions by allowing for bilateral interactions between two participants on the Ethereum blockchain, which are settled on the main blockchain at a later date. Examples: Raiden Network and Connext.

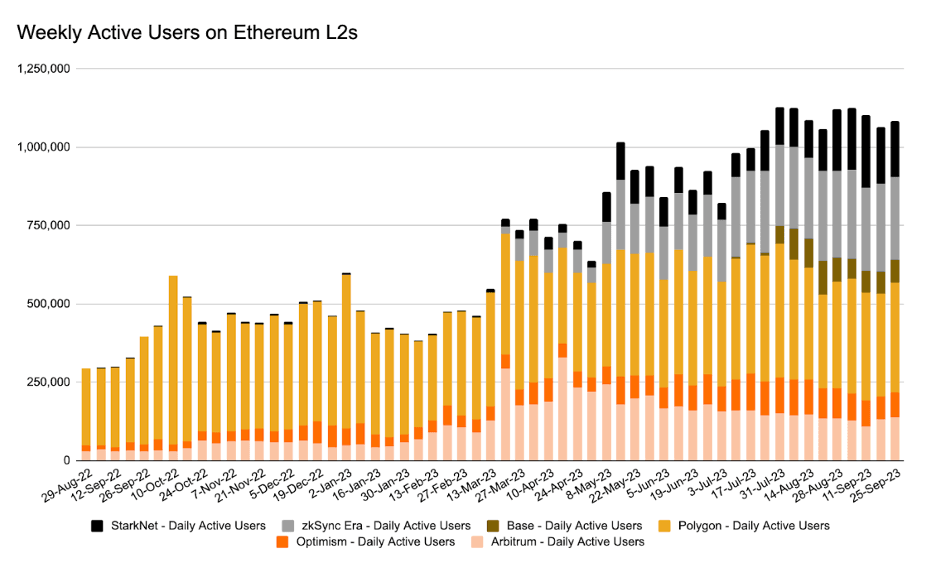

Layer 2s have been growing significantly over the last two years. Weekly active users on the leading Ethereum scaling platforms have more than doubled from ~450k in November 2022 to more than 1 million as of September 2023 (see Figure 4). Ethereum’s scaling thesis is becoming a reality as multiple L2 networks converge upon similar architectures and compete for the most network effects. While it’s still unclear which will win, the fierce competition between L2s is unequivocally positive for Ethereum, as they directly accrue value to Ethereum, acting as their settlement layer, as well as contributing towards bringing on an influx of new developers, applications, and users.

Figure 6: Ethereum Scaling Solutions

Source: Artemis, 21Shares

EIP-1559

EIP-1559 was a proposal to upgrade the economics of how users pay transaction fees on Ethereum and went live on August 5, 2021. Some have lauded it as “the final puzzle piece to Ethereum’s monetary policy.” In short, the protocol upgrade is intended to make the flow of transaction fees on the Ethereum network more predictable and to more closely tie the value of Ether to the demand for transactions on its blockchain.

The changes entailed a so-called burning mechanism that burns a certain amount of Ether per transaction while adjusting the burnt amount to allow users to more accurately predict how much they will pay in transaction fees over time. The fee burn would respond dynamically to demand on the Ethereum network. In addition, this change creates deflationary pressure on Ethereum’s supply, which further increases when the demand for transactions and smart contracts increases, and then decreases when the demand for the network decreases. This deflationary pressure positively impacts Ether’s valuation, assuming the need for the cryptoasset remains the same.

Figure 7: EIP-1559 Mechanism

Source: ConsenSys

EIP 4844

Ethereum’s next major upgrade, slated for Q1 2024, is expected to address the issue of reducing transaction fees for Ethereum’s scalability solutions, known as rollups. The upgrade, otherwise known as Proto-DankSharding, does so by introducing a new type of transaction called Blob, which is cheaper to store and process, enabling the efficient handling of large chunks of data. EIP 4844 also aims to offer a solution that introduces the transaction format of sharding, which should make the transition into the scaling solution smoother in case sharding is fully implemented later in Ethereum’s roadmap. The primary beneficiaries of this upgrade are Layer 2 protocols, which will offer cheaper transaction fees for users by factor of ~100x.

Valuing Ethereum

In this section we will present two ways to value Ethereum: 1) intrinsic valuation and 2) relative valuation.

Ethereum's Intrinsic Valuation

From the standpoint of a validator, PoS assets like ETH are akin to a stock paying a dividend yield, which means we can conduct a DCF valuation following four simple steps:

(1) Estimate the cash flows during the life of the cryptoasset

- a. Transaction fees within the network accrue to validators. Just so, fees are a proxy for revenue. Ethereum validators received $355.01 million in transaction fees (net after the burn mechanism) from September 30, 2022, to September 30, 2023.

- b. Token issuance doesn’t dilute the value of validators. On the contrary, they have the right to new issuance, similar to how shareholders may receive stock-based compensation. ETH Issuance from September 30, 2022, to September 30, 2023, amounted to $1.17 billion.

- c. Total Cash Flows: a + b = $1.52 billion in the first year.

(2) Estimate expected future cash flows and the lifespan of the cryptoasset

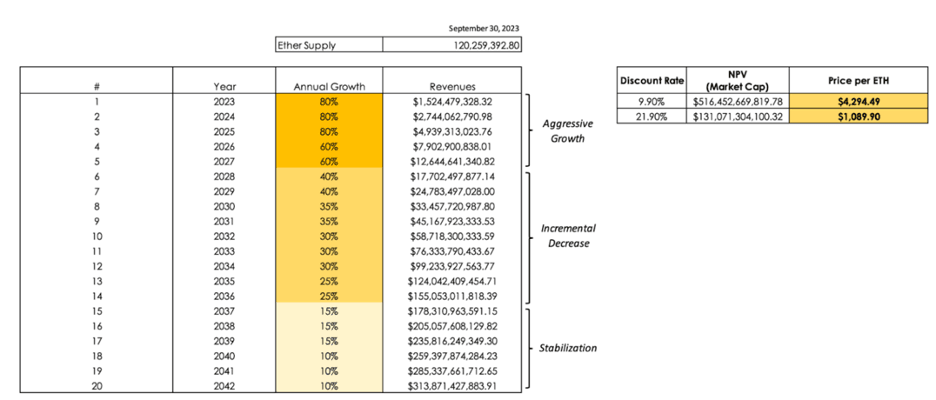

- a. Future cash flows: We propose a slight variation of the three-stage growth model to project Ethereum’s future cash flows. Specifically, we forecast an initial period of aggressive growth, followed by an incremental decrease that eventually stabilizes at a more moderate growth rate.

- b. Lifespan of the asset: With public companies that at least in theory can last forever, equity analysts generally assume that cash flows beyond a specific point in time continue in perpetuity. Investors may apply the same logic to PoS cryptoassets, but for simplicity’s sake, we assume ETH’s life will be 20 years.

(3) Estimate the discount rate to apply to these cash flows

- a. Lower-bound discount rate (9.90%): In the past 10 years, the Invesco QQQ Trust ETF obtained a 9.90% compound annual return.

- b. Higher-bound discount rate (21.90%): Obtained using the Fama and French Three-Factor Model (market premium, size premium, and value premium).

(4) Estimate the net present value (NPV) of cash flows using the above parameters

Assuming a discount rate of 9.09%, the implied price per one ETH today would be ~$4,293, a ~157% increase from ETH’s price ($1,668) as of September 30, 2023. On the other hand, if we use a 21.90% discount rate, the implied price per one ETH would be ~$1,090, a ~35% decrease from ETH’s price as of September 30, 2023. Investors should interpret the results of this DCF valuation with caution and run their own assumptions regarding projected cash flows and discount rates. The rationale behind our approach was to be conservative and capture the high volatility of ETH in the discount rate to accurately reflect the asset’s riskiness. Another implicit assumption of this approach is that the asset’s monetary premium (Store of Value) is embedded into the DCF.

Figure 8: ETH DCF Valuation

Source: 21Shares, as of September 30, 2023

Ethereum's Relative Valuation

A significant portion of equity valuations in traditional finance consists of relative valuations based upon market sizing and multiples, such as price-to-earnings (P/E ratio). This approach is more likely to reflect market perceptions and sentiment than a fundamental valuation. Moreover, investors can use relative valuations to "price" any asset, not just ones that generate cash flows.

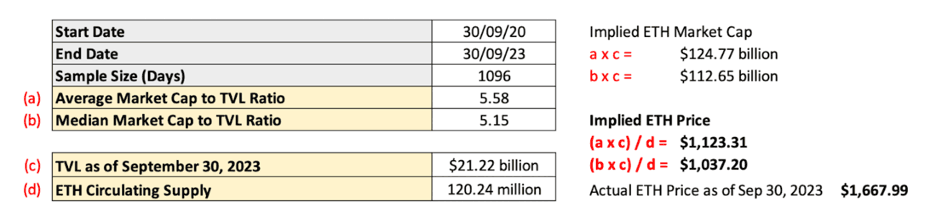

In decentralized finance (DeFi), total value locked (TVL) is a crypto-native metric that investors can use as a proxy for assets under management (AUM). Hence, an ingenious pricing approach is to represent the market value of a smart contract platform like Ethereum as a multiple of TVL. We should clarify that TVL in our exercise includes Ethereum’s base chain and scaling platforms (Layer 2s).

Figure 4 shows that investors are pricing ETH at a premium relative to historical levels. A plausible explanation is that activity has dropped relative to the period of euphoria we experienced during 2020 and 2021. However, a flaw of this metric is that TVL does not necessarily translate to higher profits. Thus, this multiple is only appropriate to the extent that TVL can effectively influence the protocol’s ongoing and future profits.

Figure 9: Ethereum’s Market Cap-to-TVL-based implied price

Source: 21Shares

Risks of Ethereum and DeFi

In this section, we zero in on one of the most quintessential elements to consider when investing in cryptoassets: the associated risks. This section is not exhaustive since, as the industry matures, some risks may be mitigated to some extent while others might come into the spotlight more sharply. We categorized the risks based on third-party involvement, their impact on market participants, and Ethereum as the settlement layer for financial applications. Finally, we describe three risks associated with DeFi and Ethereum – technological, regulatory, and financial risks.

Technology Risks

Bugs, hacks, or implementation failures not only present a major impediment to the mainstream adoption of DeFi but also slow down the potential value brought to Ether in the future. In this part, we cover the main technological risks associated with both Ethereum and DeFi applications.

Smart Contract Loopholes and Hacks

Hacks originating from smart contract loopholes are the Achilles’ heel for adoption, primarily when they permanently lose user funds. This fear can haunt risk-averse users and entrepreneurs alike, prevent them from using certain crypto services, or even drive them to capitulate. The DAO hack is a good example. In 2016, this popular project launched on Ethereum and built by the team behind the now-defunct startup Slock — was hacked. It raised over $100 million worth of Ether, which an unknown attacker stole 3.6 million Ether. As of August 2021, with the price of ETH trading at $3.2K, this hack would have represented over $11.5 billion of investors’ money lost. At the time of the theft, the price of ETH went down to $12 from a high of $20, a 40% drop. It’s worth noting that the hack didn’t relate to the Ethereum blockchain per se and, hence, didn’t affect users’ funds held on the blockchain. Instead, the problem emanated from the smart contract built by the DAO.

Network Congestion

The unprecedented growth of DeFi has led to excessive amounts paid by users in gas fees, surpassing what one would pay to make international payments with Western Union. Frontrunners also scan unconfirmed transactions on Ethereum to find transactions attempting to score arbitrage. Then, they pay miners a little more for the same transaction to pocket the arbitrage themselves, and this concept is called Maximal Extractable Value (MEV). As a reminder, gas fees make up the payment in ETH to use the Ethereum platform. As such, rising fees present the perfect opportunity for Ethereum competitors and off-chain solutions to flourish, driving a user and entrepreneur brain drain from Ethereum to other solutions.

Liquid Staking

In 2023, Ethereum faced a pivotal moment with the Shanghai upgrade, enabling users to unlock staked ETH that had been locked since late 2020. To address this liquidity gap, a new breed of staking protocols, known as liquid staking, emerged in 2021. These protocols enable users to convert their illiquid staked ETH into a liquid version or an IOU, tradable as any ERC20 token. This innovation allows users to earn staking rewards without relinquishing ownership of their ETH, while providing the flexibility to use the IOU as collateral in DeFi lending and borrowing.

Nevertheless, potential risks lurk, as these derivatives may not always closely match the market price and could trade at a discount during periods of selling pressure on secondary markets. Additionally, smart contract exploits could jeopardize the network's security if the underlying staked ETH is impacted. Centralization concerns have also surfaced, particularly with Lido, holding a dominant 71% market share and depending on 32 node operators. In response, Lido plans to bolster decentralization through measures like distributed validation technology (DVT) to further distribute staked ETH across a wider list of node operators, and adopting a permissionless validator onboarding approach, mirroring the operational practices of other service providers across this vertical like Rocket Pool, Frax.

Regulatory Risks

In the aftermath of the Ethereum Merge, concerns have arisen regarding the possibility that the shift to Proof of Stake (PoS) could classify ETH as a security under U.S. securities law. This classification typically hinges on the Howey Test, which examines whether there is an investment of money, a common enterprise, a reasonable expectation of profits, and profits derived from the efforts of others. SEC Chairman Gary Gensler has hinted that staking models might trigger tokens to qualify as investment contracts under the Howey Test, raising questions about whether the shift to staking in Ethereum could satisfy the "efforts of others" criterion. Gary Gensler also suggested that staking service providers pooling customer assets for staking might resemble a security offering.

The SEC's stance on digital assets has been increasingly stringent, but some have relied on previous statements (such as a statement from a speech by former SEC Director William Hinman in 2018) to argue that ETH is not a security due to its decentralized nature. If Ethereum is genuinely decentralized, it would be challenging to pinpoint a core team responsible for securities law disclosures. Some proposed legislation even classifies ETH as a commodity. The potential consequences of the SEC treating ETH as an unregistered security after the Merge are uncertain but far-reaching. This could require disclosures and filings for ETH transactions, affecting exchanges listing ETH. The impact would extend to other PoS blockchains and their protocols, introducing ambiguity about responsibilities and enforcement in decentralized systems.

Disclaimer

The information included herein is the express opinion and experience of 21Shares and is provided for discussion purposes only. Past performance is not indicative of future results. Investors should consult with their own advisors for legal, tax, regulatory, financial, accounting, and other aspects relevant to the investment's suitability and potential consequences.

This presentation is for informational and discussion purposes only and does not constitute an offer to sell or a solicitation of an offer to purchase any security. The information set forth herein does not claim to be complete and is subject to change. This presentation does not constitute a part of any document of any fund and should not be construed as an advertisement or marketing material for any fund.

Certain statements contained in this presentation are based on the expectations, estimates, projections, and opinions of 21Shares. Such statements involve known and unknown risks, uncertainties, and other factors, and reliance should not be placed thereon. This presentation contains “forward-looking statements,” the outcome of which may differ materially from those reflected or contemplated herein.

Certain economic, market, financial, and other information contained herein has been obtained from managers, service partners, and other parties besides 21Shares. While such sources are believed to be reliable, none of 21Shares or any of their respective affiliates or employees assumes any responsibility for the accuracy or completeness of the information contained in this presentation or to update any information contained herein.

Investing in crypto assets, including cryptocurrencies and crypto tokens, carries inherent risks. These assets are considered highly speculative due to their limited history and new technological nature. Future regulatory actions may impact the usability and tradability of crypto assets. The price of crypto assets can be influenced by a small number of holders and may decline in popularity or acceptance, affecting their value.

None of 21Shares nor any of its affiliates have made any representation or warranty, express or implied, with respect to the fairness, correctness, accuracy, reasonableness or completeness of any of the information contained herein (including but not limited to information obtained from third parties), and expressly disclaim any responsibility or liability relating thereto.

%20(1).webp)

.svg)