Aave’s governance crisis: the vote is over, the ownership question isn’t…

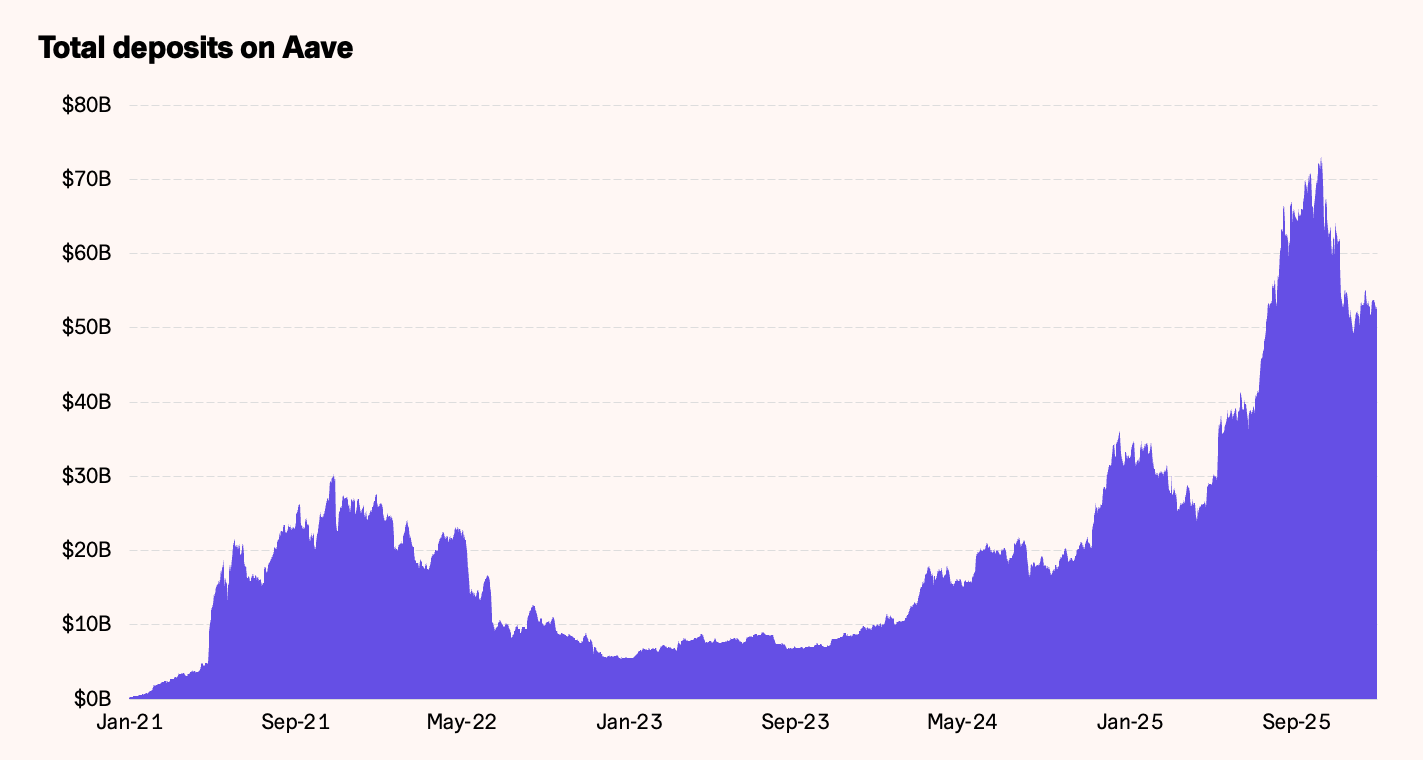

Aave, the largest lending protocol in decentralized finance (DeFi) with over $53 billion in net deposits, has faced a governance crisis that goes beyond a single vote. At its core is an unresolved question that many DeFi protocols have postponed: who actually owns the economic value of a decentralized protocol when governance is onchain, but brands, interfaces, and key monetization points are controlled by a private company? A recent Aave governance vote has brought this tension into the open, exposing fault lines between token-holder ownership, operational control, and value capture.

This note examines why that vote did not settle the issue, what it reveals about DAO governance at scale, and why the outcome matters not just for Aave, but for investors and DeFi protocols structured around a DAO and a for-profit organization split.

Two Aave organizations, one protocol

To understand why this escalated so quickly, you have to start with Aave’s structural split.

On one hand sits Aave DAO, governed by AAVE token holders. The DAO controls the core lending smart contracts, sets risk parameters, and accumulates protocol-level revenue into the treasury. Economically, it owns the onchain system, the engine.

On the other hand sits Aave Labs, a private company by Aave founder Stani Kulechov. It employs core builders and controls what most users perceive as “Aave”: the website and interface, infrastructure (including security), brand, domains, and much of the product development and branding. Economically, it controls the storefront, and in crypto, storefronts monetize.

For years, this split worked because early growth masked the ambiguity. But once meaningful revenue, estimated at circa $90 million annually, began appearing outside the DAO’s immediate perimeter, the arrangement stopped being just a theoretical debate.

The trigger: an interface change that looked like a value grab

The spark came in early December, when Aave Labs announced a partnership with the decentralized exchange CoW Swap, integrating the service on the official Aave interface. The public rationale was user-centric: better execution, MEV protection, and improved pricing. Few disagreed with the goal. The issue was not the integration itself, but what followed.

Onchain analysis showed that swap-related fees, previously routed to the DAO treasury, were now flowing to wallets controlled by Aave Labs. Delegates estimated the revenue impact at roughly $200k per week, or $10m+ per year. In isolation, that figure might appear modest. In context, it represents more than 10% of the DAO’s estimated ~$90m in annualized revenue, value generated at the interface layer of a protocol governed and economically underwritten by token holders.

That relative magnitude is what turned a philosophical question into an existential one. Once a protocol generates eight figures of annualized value at the interface layer, value inseparable from a DAO-owned system, unilateral redirection begins to look less like operational discretion and more like structural value leakage. At that point, the AAVE token’s economic claim starts to resemble an expectation rather than enforceable ownership.

Escalation: from fee routing to ownership

Once public, the debate escalated rapidly. What began as “why did the DAO lose revenue?” quickly turned into “what does token-holder ownership actually mean?” Proposals emerged that pushed far beyond fee flows. Some advocated a so-called “poison pill”: transferring Aave IP, brand, and domains into DAO control and forcing Labs into a subordinate structure. Others argued for immediate transfer of trademarks, domains, repositories, and social accounts to the DAO.

The logic was consistent: if the DAO funds development and governs risk, it should not be structurally dependent on a private company that controls the protocol’s monetization choke points.

Aave Labs pushed back just as forcefully. Their position was that the DAO governs contracts, not websites, and that frontend monetization reflects the real costs of running infrastructure, maintaining security, and paying engineers. In this framing, the interface is not a public good, but a product built on permissionless rails. This is the unresolved fault line in DeFi governance:

- The DAO claims economic legitimacy because it governs the protocol.

- The Labs claims operational legitimacy because it ships the product.

Both are true. And when money appears at the boundary, alignment gets stress-tested.

The snapshot that collapsed trust

On December 23, a Snapshot vote went live asking whether Aave-related brand assets should be brought under DAO control. But the vote itself immediately became a controversy.

The proposal’s author publicly stated they did not approve its submission, criticized the rushed timing, and urged the community to abstain, arguing that voting either way would legitimize a procedurally flawed process. Major delegates echoed these concerns, citing holiday timing, compressed discussion, and sudden shifts in delegated voting power.

When a proposal’s own author disowns the vote, substance becomes secondary. Governance is not just about outcomes, it is about process credibility. And at that moment, the Snapshot became less a vote on ownership and more a test of whether Aave governance could still function as a legitimate coordination and alignment mechanism.

The result: rejection by design, not indifference

The vote closed exactly where momentum had pointed: a decisive no (NAY) plus abstain supermajority. But interpreting that outcome as a simple rejection misses the signal. This was not a clean “no.” A large portion of token holders and delegates explicitly declined to validate a rushed, binary decision on a complex legal and economic issue. Abstention was not disengagement, it was intent. In fact, nearly 45% of voting power either abstained or supported the proposal.

Two observations stand out. First, participation broke records despite every factor that normally suppresses turnout, namely 1.8 million AAVE voting power expressed this despite short timelines, a holiday window, and a rapidly evolving debate. Second, delegation diversity diverged sharply: no votes were concentrated in a small cluster of large holders, while abstain reflected the most broadly distributed set of voters. The message was layered but clear, the community rejected the process. A narrow Snapshot result cannot be framed as broad endorsement of the status quo and the concerns that triggered the debate remain unresolved.

The unspoken power dynamic: concentrated governance

This episode also surfaced a reality token governance often avoids discussing until it matters: concentration. Stani Kulechov is estimated to control roughly ~33% of AAVE supply, and during the drawdown he acquired approximately $12–15M worth of AAVE. Whatever the motivation, the implication is structural: large holders can materially shape outcomes.

That does not mean governance is broken. But it does puncture the myth that DAOs are inherently democratic. They are better described as hierarchical coordinated systems based on token holdings, whose legitimacy depends on norms, credible process, and alignment between large stakeholders and the broader community. When those norms fracture, confidence erodes quickly.

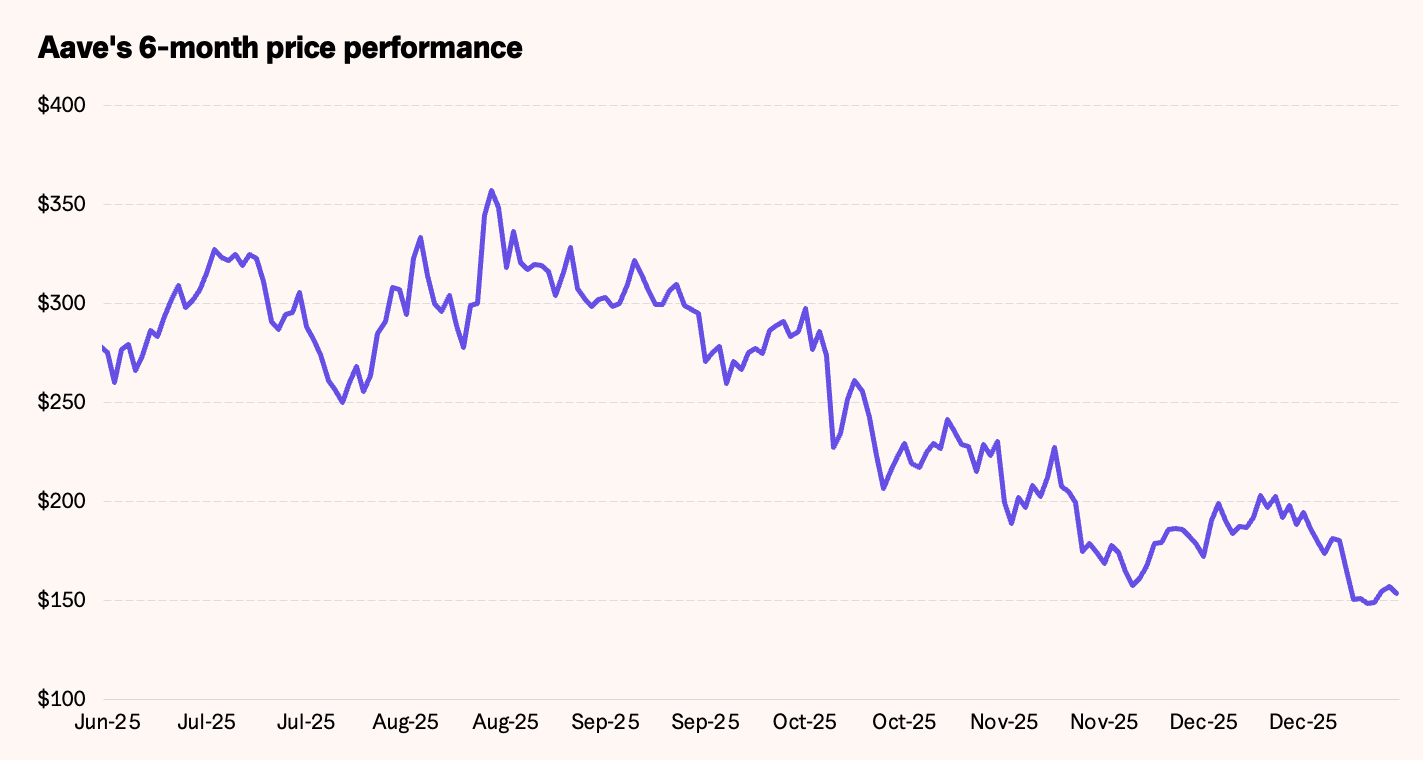

Market reaction: governance risk gets priced

Markets reacted accordingly. AAVE declined around 22% during the dispute, even as broader crypto markets remained flat. The drawdown reflected not protocol weakness, but governance uncertainty, a risk premium applied when long-term value capture becomes unclear. At the same time, fundamentals continued to tell a different story.

Aave remains the largest lending protocol in DeFi, with nearly $53 billion in net deposits, having more than tripled over the past year. Usage, institutional relevance, and product expansion have not stalled. The protocol’s engine is stronger than ever which is precisely why the ownership debate matters now.

Where this leaves Aave and what investors should consider

Despite the turmoil, Aave remains one of the most important projects in crypto. Heading into 2026, it has credible catalysts: Aave V4 as a modular liquidity and risk engine, Horizon as an institutional credit market, and a consumer-facing Aave App aimed at mainstream onboarding. In effect, Aave is evolving into a full-stack onchain credit system.

That scale changes the stakes. Ownership and value capture can no longer remain ambiguous. Long-term valuation will depend not only on adoption and usage, but on whether economic value generated across protocol, frontend, and brand accrues in ways token holders can credibly defend.

For investors, this distinction matters. In the short term, governance uncertainty justifies a discount and markets have already applied it. But importantly, this is governance risk, not operational decay. The protocol’s fundamentals remain strong: deposits are growing, institutional relevance is increasing, and product expansion continues uninterrupted.

In the medium term, that same discount can turn into opportunity. Aave’s deep liquidity, engaged community, and economic gravity make a negotiated resolution far more likely than a prolonged governance standoff. Put differently: governance issues are solvable, while network effects at Aave’s scale are not easily replicated.

This creates a familiar asymmetry for long-term investors. If governance uncertainty resolves, most likely through clearer ownership definitions and a follow-up vote, valuation can normalize while fundamentals remain intact. If it does not, the protocol still operates as the dominant onchain lending market, albeit with a persistent risk premium.

Now Aave has to do what much of DeFi has avoided: explicitly define what “ownership” means when code is decentralized, but brands are not. If it succeeds, this episode may ultimately be remembered not as a governance failure, but as a watershed moment DeFi began taking token-holder rights and investor protections seriously.

This report has been prepared and issued by 21Shares AG for publication globally. All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however, we do not guarantee the accuracy or completeness of this report. Crypto asset trading involves a high degree of risk. The crypto asset market is new to many and unproven and may have the potential not to grow as expected.Currently, there is relatively small use of crypto assets in the retail and commercial marketplace in comparison to relatively large use by speculators, thus contributing to price volatility that could adversely affect an investment in crypto assets. In order to participate in the trading of crypto assets, you should be capable of evaluating the merits and risks of the investment and be able to bear the economic risk of losing your entire investment.Nothing herein does or should be considered as an offer to buy or sell or solicitation to buy or invest in crypto assets or derivatives. This report is provided for information and research purposes only and should not be construed or presented as an offer or solicitation for any investment. The information provided does not constitute a prospectus or any offering and does not contain or constitute an offer to sell or solicit an offer to invest in any jurisdiction. The crypto assets or derivatives and/or any services contained or referred to herein may not be suitable for you and it is recommended that you consult an independent advisor. Nothing herein constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to your individual circumstances or otherwise constitutes a personal recommendation. Neither 21Shares AG nor any of its affiliates accept liability for loss arising from the use of the material presented or discussed herein.Readers are cautioned that any forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors.This report may contain or refer to material that is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject 21Shares AG or any of its affiliates to any registration, affiliation, approval or licensing requirement within such jurisdiction.

.svg)