Will Bitcoin ride the “debasement trade” wave into year-end?

A good old narrative is echoing louder across markets: the so-called “debasement trade.” It reflects a growing concern that governments have lost the will or ability to rein in spending and debt, leading investors to seek shelter in assets that policy changes cannot easily dilute. Gold and Bitcoin have been the primary beneficiaries of this move, with both seen as “hard assets” that offer insulation from fiat currency debasement.

The timing is critical. With central banks expected to cut rates even as inflation remains above target, investors are increasingly questioning whether policymakers are prioritizing growth over price stability. This perceived shift toward looser monetary policy in an already inflationary environment has reignited fears of long-term currency debasement and fueled renewed interest in alternative stores of value.

The logic is simple: when the value of money itself comes into question, capital migrates toward assets that can’t be created out of nothing. That’s what has driven gold to repeated record highs this year, and it’s increasingly what investors expect from Bitcoin heading into the final months of 2025.

Why is the “debasement trade” getting more prominence now?

Across major economies, fiscal deficits remain wide, political dysfunction is on the rise, and central banks are cutting rates despite inflation remaining above target. This combination has revived fears of structural inflation and long-term dollar weakness. The so-called “hard asset” rally spanning gold, commodities, and Bitcoin is a direct response to those fears.

Gold, the traditional hedge against monetary debasement, has surged more than 50% this year, hitting all-time highs above $4,000 per ounce. Bitcoin has gained just 20% year-to-date. This performance gap between the two suggests Bitcoin still has room to run, particularly as macro conditions remain supportive.

What makes Bitcoin a “debasement trade”?

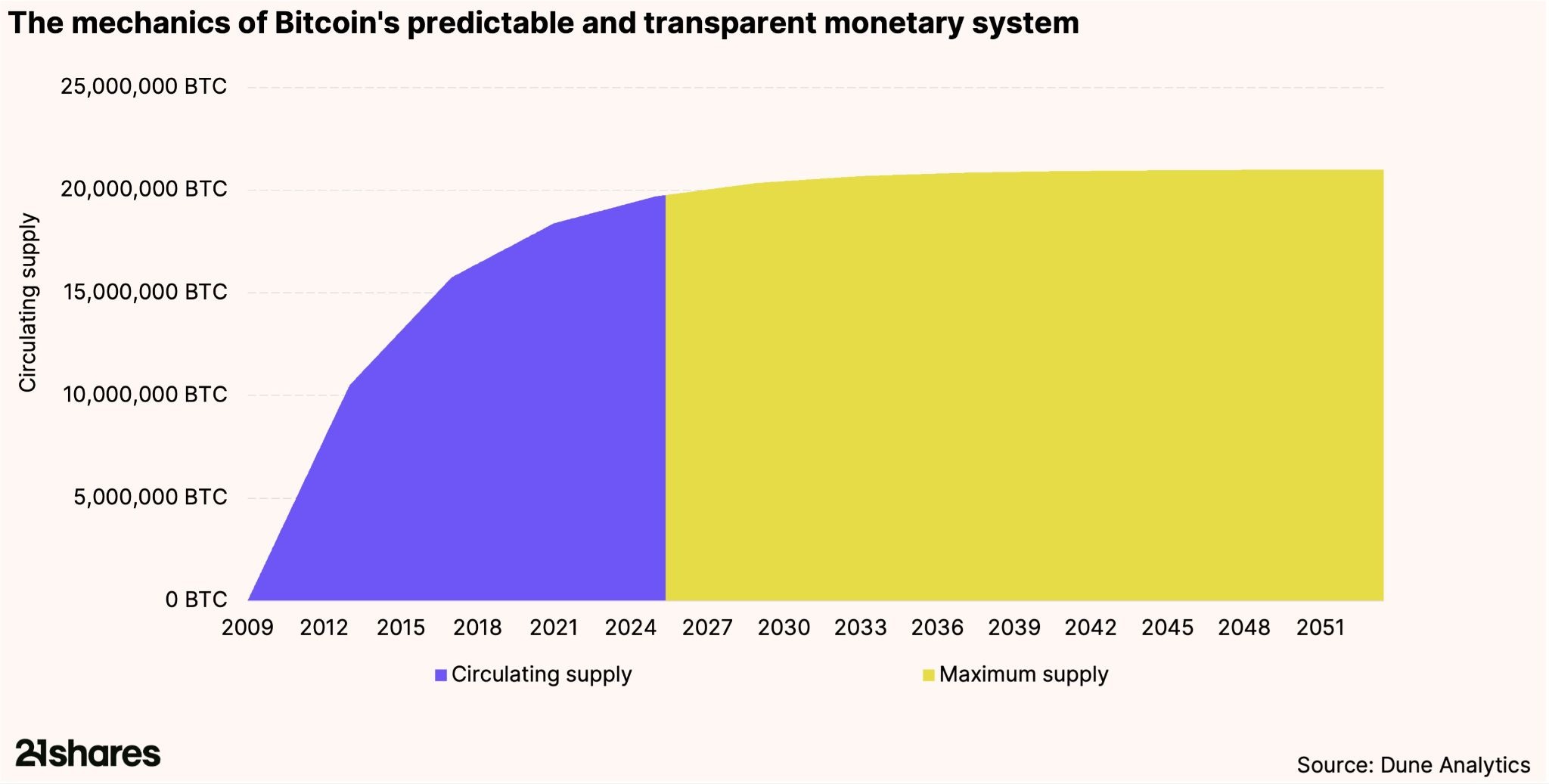

One reason Bitcoin continues to attract attention in this environment is its unique monetary design. Unlike fiat currencies or even gold, Bitcoin’s supply is mathematically capped at 21 million coins.

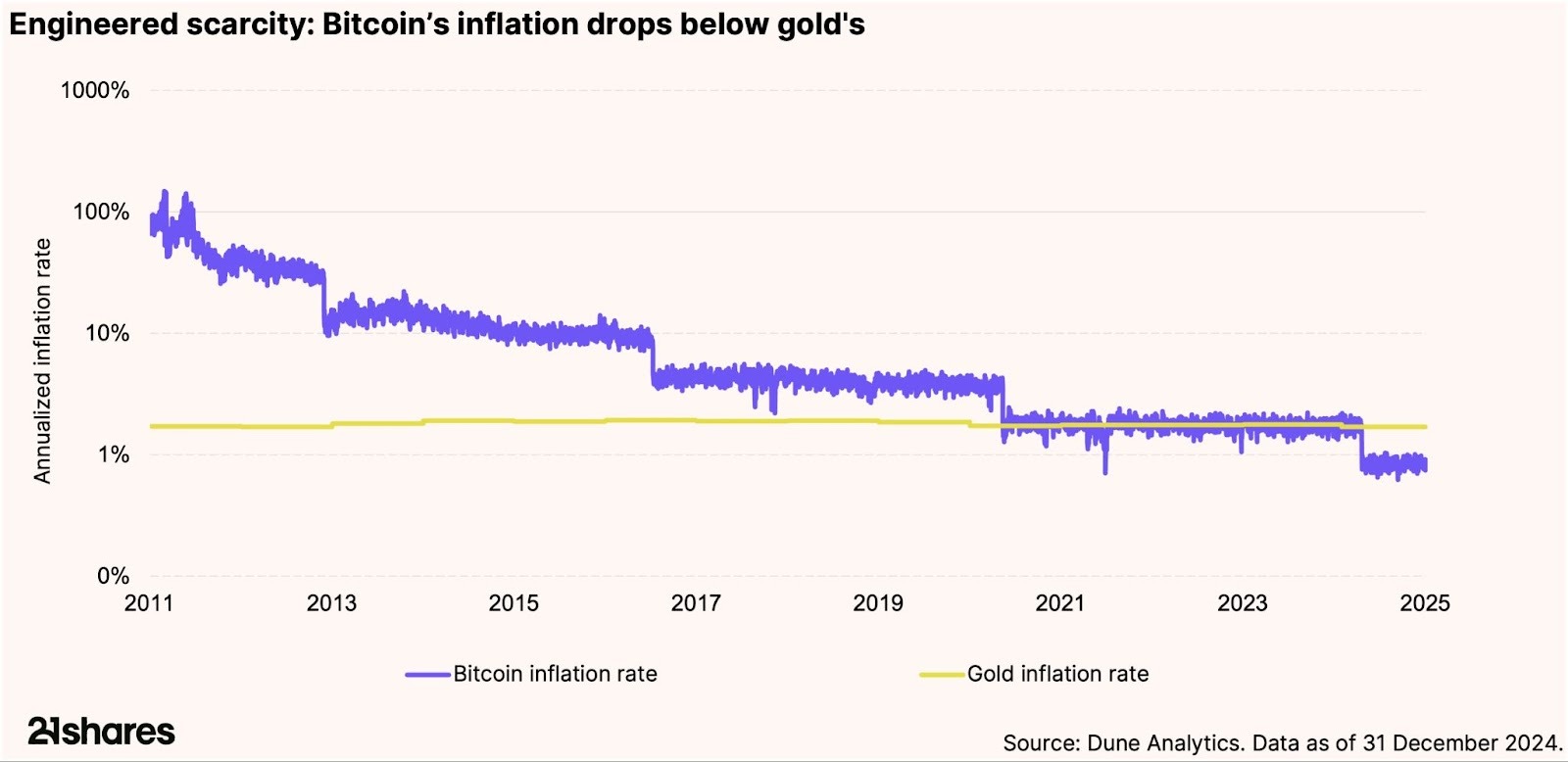

This hard limit makes its long-term inflation rate predictable and structurally lower than gold’s. As investors increasingly seek protection from currency debasement, Bitcoin’s transparent, programmatic supply schedule stands in sharp contrast to the flexibility of central banks and governments. It effectively positions Bitcoin as a modern, digital version of “hard money”, one immune to excessively expansive fiscal policy.

The story in the numbers: Institutional flows and the Bitcoin to gold ratio

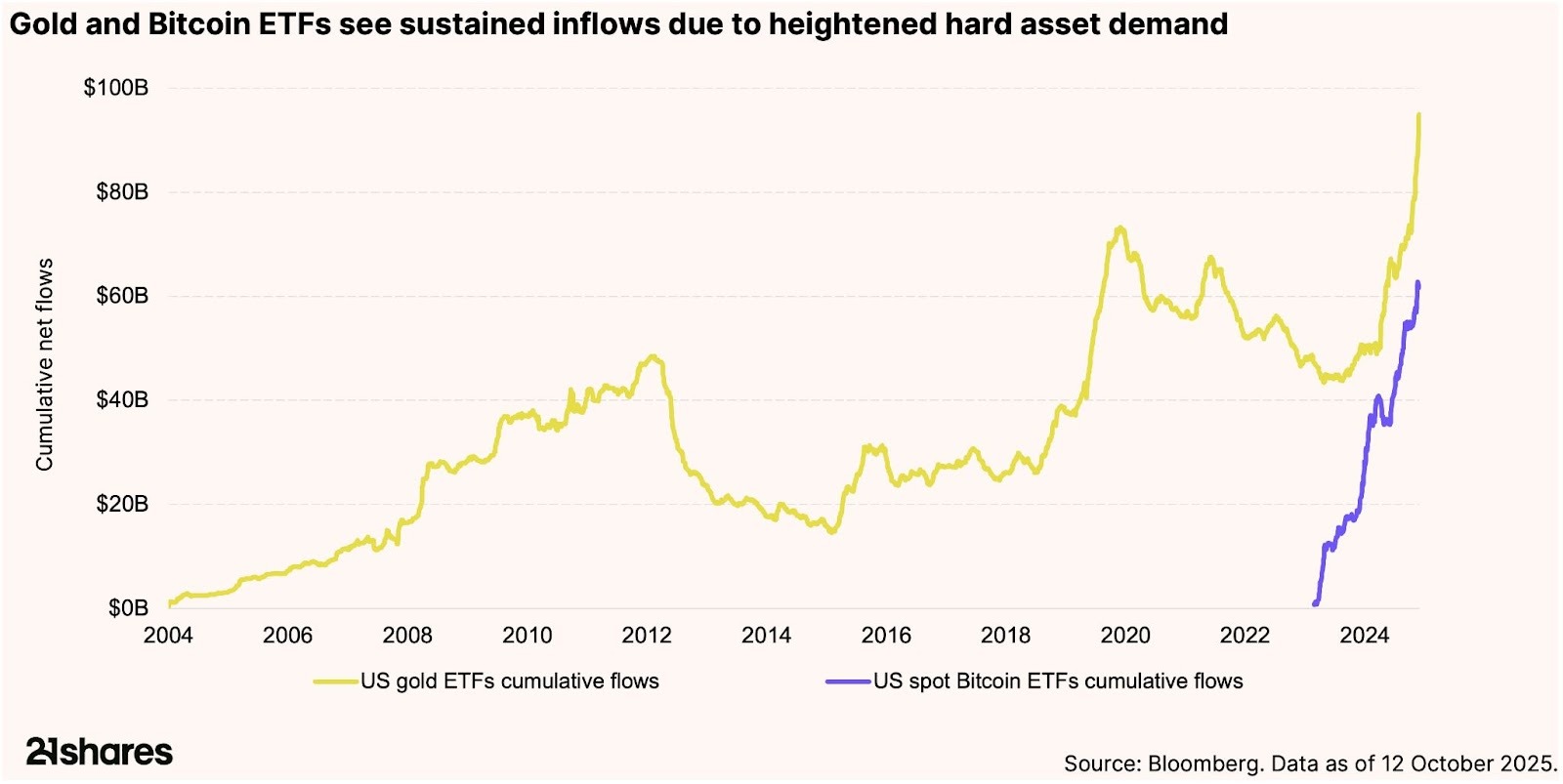

Global demand for gold ETFs has surged this year, with $64 billion in inflows year-to-date and a record $17.3 billion in September alone1. This marks a sharp turnaround from the $23 billion in outflows recorded over the previous four years, underscoring investor demand for tangible stores of value. By contrast, Bitcoin ETF flows have been more volatile but remain structurally positive, with $30 billion in inflows year-to-date and $3.9 billion in September (including Future ETFs in the US). The relative calm in Bitcoin inflows alongside its still-wide performance gap to gold suggests a potential “catch-up” trade as investors rebalance portfolios into year-end.

The Bitcoin-gold ratio highlights that relationship clearly. Since the start of 2024, gold has dramatically outperformed, but the ratio now sits at historically oversold levels. Historically, such extremes have preceded periods of Bitcoin outperformance, particularly during “risk-on” phases when liquidity conditions improve.

Is a Q4 reversal underway?

As global growth expectations stabilize and central banks maintain an easing bias, liquidity could once again become a key driver of asset performance. Historically, Bitcoin has tended to outperform gold in such environments, aligning with its role as a higher-beta expression of the same macro theme.

We’ve seen this dynamic play out before. Once the worst of the tariff-driven market jitters subsided in Q2, the Bitcoin-to-gold ratio sharply reversed higher, reflecting Bitcoin’s dual identity as both a risk-off hedge and a risk-on liquidity play. When fear dominates, gold tends to lead—but as sentiment improves and liquidity returns, Bitcoin often reclaims the spotlight.

In essence, the debasement trade is not just about hedging inflation; it’s about hedging dysfunction. Both gold and Bitcoin serve that purpose, but with gold already leading the charge, Bitcoin may now be set to play catch-up. If the year-end proves as liquidity-friendly as it appears, Bitcoin could once again emerge as the late-cycle beneficiary of a trade that began in fear and may end with digital gold taking center stage.

Footnotes:

World Gold Council. Gold ETFs, Holdings and Flows. GoldHub, 13 Oct. 2025. Available at: https://www.gold.org/goldhub/data/gold-etfs-holdings-and-flows.

This report has been prepared and issued by 21Shares AG for publication globally. All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however, we do not guarantee the accuracy or completeness of this report. Crypto asset trading involves a high degree of risk. The crypto asset market is new to many and unproven and may have the potential not to grow as expected.Currently, there is relatively small use of crypto assets in the retail and commercial marketplace in comparison to relatively large use by speculators, thus contributing to price volatility that could adversely affect an investment in crypto assets. In order to participate in the trading of crypto assets, you should be capable of evaluating the merits and risks of the investment and be able to bear the economic risk of losing your entire investment.Nothing herein does or should be considered as an offer to buy or sell or solicitation to buy or invest in crypto assets or derivatives. This report is provided for information and research purposes only and should not be construed or presented as an offer or solicitation for any investment. The information provided does not constitute a prospectus or any offering and does not contain or constitute an offer to sell or solicit an offer to invest in any jurisdiction. The crypto assets or derivatives and/or any services contained or referred to herein may not be suitable for you and it is recommended that you consult an independent advisor. Nothing herein constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to your individual circumstances or otherwise constitutes a personal recommendation. Neither 21Shares AG nor any of its affiliates accept liability for loss arising from the use of the material presented or discussed herein.Readers are cautioned that any forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors.This report may contain or refer to material that is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject 21Shares AG or any of its affiliates to any registration, affiliation, approval or licensing requirement within such jurisdiction.

.svg)